What is Transfer Pricing ?

To understand what is transfer pricing, let us look at an example : –

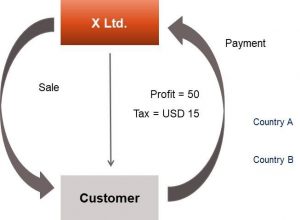

X Ltd. operates in Country A, wherein the tax rates are 30%. It intends to sell goods costing USD 100 to a customer in Country B for USD 150.

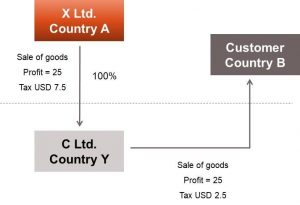

X limited also has a subsidiary C Ltd. in Country Y ?

CASE I – IF X Ltd. sells GOODS DIRECTLY TO A CUSTOMER IN COUNTRY B

In such a case, its profit would be: –

= (Sale Price – Cost)

= USD 150 – USD 100

= USD 50

Tax = 30% of profit = 30% of USD 50 or USD 15

However by changing the mechanics of the transaction, X Ltd. can reduce its taxes. This is discussed as under : –

To save taxes, X Ltd. incorporated a subsidiary in Country Y, namely Subsidiary C, where tax rate is 10% and sold the goods to C for USD 125. C Ltd. then which in turn, sold the goods to buyer in Country B for USD 150.

In such a case, tax is computed as under: –

Tax = (Tax in Country A) + (Tax in Country Y)

= (125 – 100) *30 + (150 – 125) *10%

= 7.5 + 2.5 = USD 10

X Ltd. saved USD 5 in taxes (USD 15 in CASE I Vs. USD 10 in CASE II) by selling goods via subsidiary C ltd. located in Country Y

Different countries have different rules on taxation, in terms of tax rates, tax exemptions etc

For example, X Ltd. , a foreign operates in Country A, wherein the tax rates are 30% while Country Y, where its Subsidiary C is incorporated has a tax rate is 10%.

Further many countries do not tax income arising on account of capital gains or in other words exempt them, where as other countries may tax such income.

While in case of unrelated entities, transactions are normally carried out at prices which are driven by commercial considerations, in case of Multi National Enterprises, which have several group companies across various tax jurisidiction, due to common control, transaction between group companies, may be structured in a manner, whereby the maximum profits accrue in jurisdiction with low/ Nil rates of taxes (in the above example, profits were artificially shifted to Country Y, where tax rate is 10%), thereby reducing the taxable income of country A.

This is achieved through contracts and prices, which may not have any commercial reasons, but are entered into to take benefit of lower tax rates .

In order to curb these practices and ensure that taxes paid in the jurisdiction where the economic activity takes place , the concept of transfer pricing was introduced. It is therefore important to understand what is transfer pricing ? This has been discussed in the subsequent blogs and write ups that we have on this topic.