In case of a transaction between two related Enterprises, both the enterprise maybe earning certain profits or losses. Under the profit split method, the total operating profit earned by the parties involved in the transaction is first ascertained. There after it is splitted, amongst the parties, based on the respective contributions.

PSM evaluates, if, the profits or loss, allocated to a particular entity, out of combined operating profit, of controlled transaction, is at arm’s length, considering their individual contribution in the overall profit or loss.

Note : –

PSM is typically applicable in international transactions or Specified Domestic Transactions, involving transfer of unique intangibles or in multiple international transactions which are so interrelated that they cannot be evaluated separately for determining the ALP of any one transaction.

Steps involved in PSM

STEP 1 : – DETERMINE COMBINED NET PROFIT

Determine combined total net profit of the AEs, arising from the controlled international transaction.

STEP 2 : –

Evaluate the relative contribution made by each AE through their activities, to the earning of such combined net profit.

Note : –

- Such evaluation of the contribution made by each AE is based on functions performed, assets employed and risks assumed by each enterprise.

- Reliable external market data , on evaluating such contribution should be obtained, by considering cases where unrelated enterprises perform comparable functions in similar circumstances, and comparied with AEs functions.

STEP 3 : –

The combined net profit is then splitted amongst the Associated Enterprises in proportion to their relative contributions.

STEP 4 : –

The profit so apportioned to the tested party, is considered to arrive at an arm’s length price of the international transaction.

Allocation Methods under PSM

The allocation of profit or loss under the PSM must be made in accordance with one of the following allocation methods : –

- Comparable Profit split; or

- Residual Profit split.

(a) COMPARABLE PROFIT SPLIT METHOD

A comparable profit split is derived, from the combined operating profit of independent uncontrolled taxpayers whose transactions and activities are similar to those of the associated related controlled taxpayers. Under this method, independent uncontrolled taxpayer’s percentage of the combined operating profit or loss, is used to allocate the combined operating profit or loss in the controlled transaction.

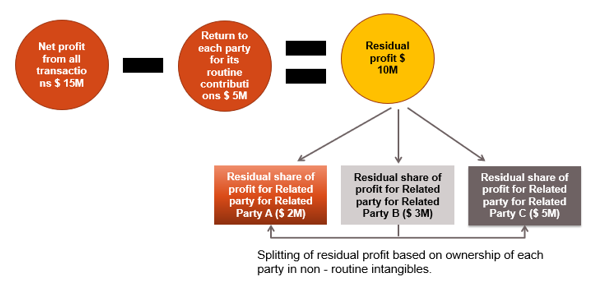

(b) RESIDUAL PROFIT SPLIT METHOD

The combined operating profit or loss from the relevant business activity is allocated between the controlled taxpayers following the two-step process : –

- Allocate operating income to each party to the controlled transactions to provide a market return for its routine contributions to the relevant business activity.

- Allocate residual profit among the controlled taxpayers, based upon the relative value of their contributions of intangible property to the relevant business activity that was not accounted for as a routine contribution.

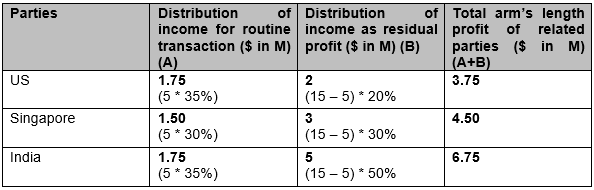

EXAMPLE : –

MNC US entered into a contract for manufacturing of Dam on a river, for which its subsidiaries in US, Singapore and India worked together. The total contract price of deal was $100M. Net profit earned by MNC US from the entire deal transactions was $15M, of which the routine contribution is $5M, wherein the relative efforts put in by group companies are 35%, 30% and 35% respectively.

Non routine profit are to be splitted amongst the group companies on the basis of ownership of non-routine intangibles i.e. 20%, 30% and 50%.

Compute the Arm’s length profit of related party in US, Singapore and India in accordance with Profit Split Method ?

SOLUTION : –

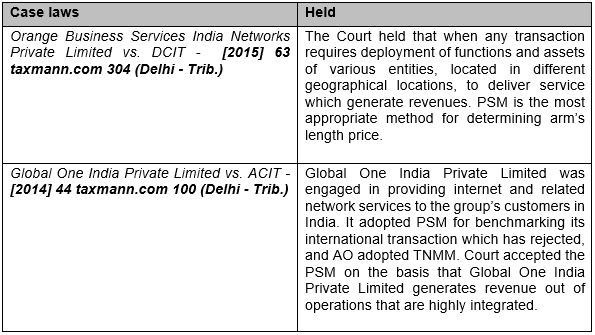

Judicial Rulings on the selection of Profit Split Method