SAFE HARBOUR RULES FOR INTERNATIONAL TRANSACTION

![]()

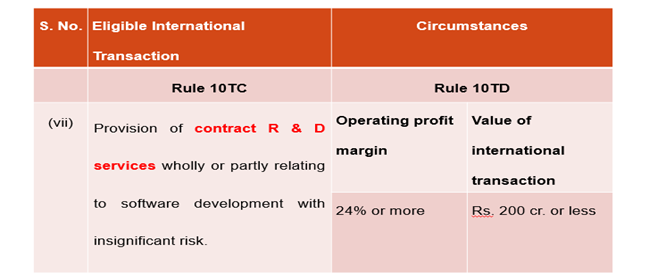

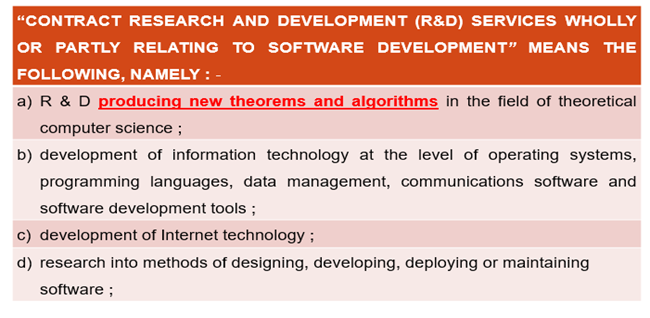

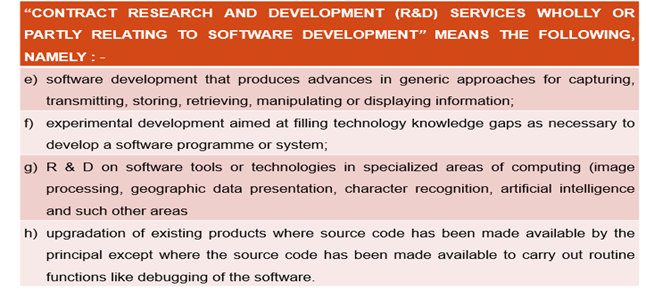

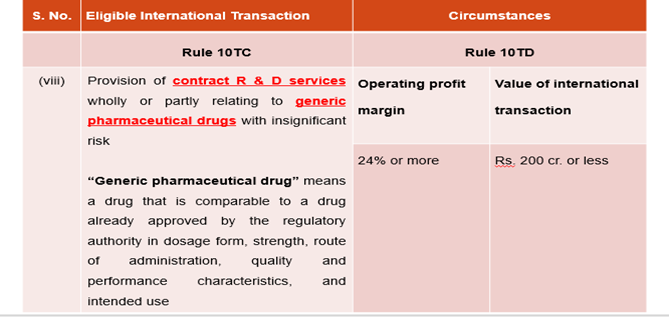

SAFE HARBOUR RULES – CONTRACT R & D SERVICES

SAFE HARBOUR RULES FOR INTERNATIONAL TRANSACTION

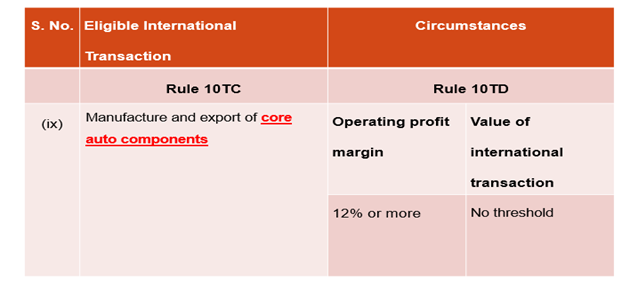

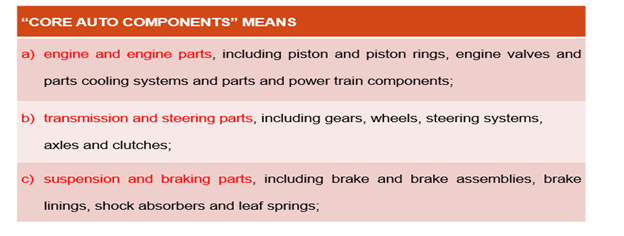

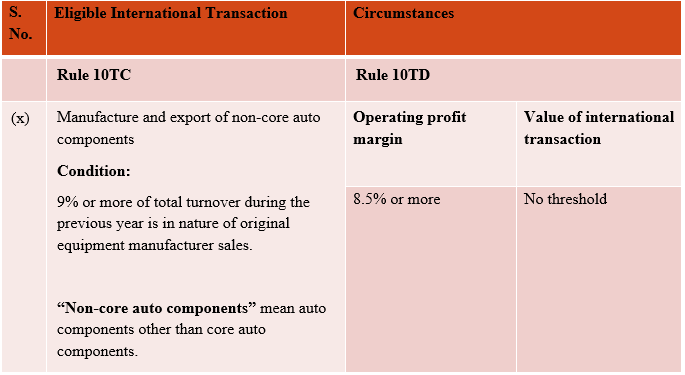

SAFE HARBOUR RULES – CORE AUTO COMPONENTS

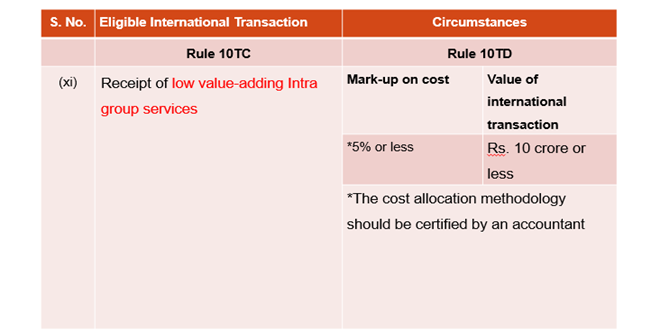

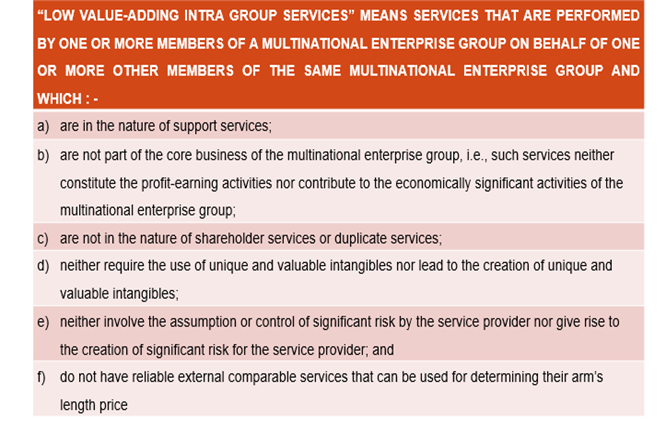

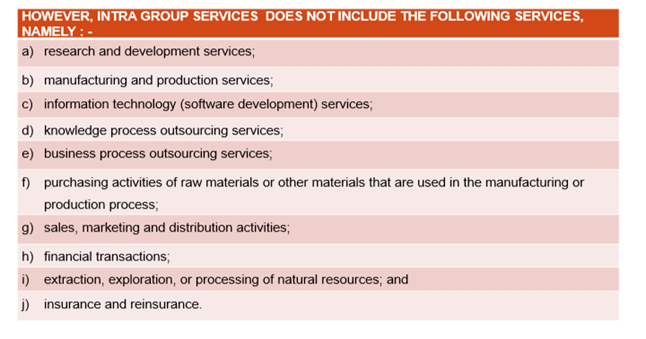

SAFE HARBOUR RULES – LOW VALUE-ADDING INTRA GROUP SERVICES

SAFE HARBOUR RULES FOR INTERNATIONAL TRANSACTION

MEANING OF ACCOUNTANT

An accountant referred to in the Explanation below section 288(2) of the Act and includes any person recognised for undertaking cost certification by the Government of the country where the associated enterprise is registered or incorporated or any of its agencies, who fulfils the following conditions, namely : –

- if he is a member or partner in any entity engaged in rendering accountancy or valuation services then, –

- the entity or its affiliates have presence in more than two countries; and

- the annual receipt of the entity in the year preceding the year in which cost certification is undertaken exceeds Rs. 10 crore;

- if he is pursuing the profession of accountancy individually or is a valuer then, –

- his annual receipt in the year preceding the year in which cost certification is undertaken, from the exercise of profession, exceeds Rs. 1 crore; and

- he has professional experience of not less than 10 years.

MEANING OF OPERATING EXPENSE – INCLUSION

The costs incurred in the previous year by the assessee in relation to the international transaction during the course of its normal operations including : –

-

- costs relating to Employee Stock Option Plan or similar stock-based compensation provided for by the AE of the assessee to the employees of the assessee,

- reimbursement to associated enterprises of expenses incurred by the AE on behalf of the assessee,

- amounts recovered from AE on account of expenses incurred by the assessee on behalf of those AE and which relate to normal operations of the assessee ; and

- depreciation and amortisation expenses relating to the assets used by the assessee,

MEANING OF OPERATING EXPENSE – EXCLUSIONS

However, the costs incurred in the previous year by the assessee in relation to the international transaction during the course of its normal operations does not include the following, namely : –

(i) interest expense;

(ii) provision for unascertained liabilities;

(iii) pre–operating expenses;

(iv) loss arising on account of foreign currency fluctuations;

(v) extraordinary expenses;

(vi) loss on transfer of assets or investments;

(vii) expense on account of income–tax; and

(viii) other expenses not relating to normal operations of the assessee

MEANING OF OPERATING REVENUE

The revenue earned by the assessee in the previous year in relation to the international transaction during the course of its normal operations including costs relating to Employee Stock Option Plan or similar stock-based compensation provided for by the associated enterprises of the assessee to the employees of the assessee but not including the following, namely : –

(i) interest income;

(ii) income arising on account of foreign currency fluctuations;

(iii) income on transfer of assets or investments;

(iv) refunds relating to income-tax;

(v) provisions written back;

(vi) extraordinary incomes; and

(vii) other incomes not relating to normal operations of the assessee.

MEANING OF OPERATING PRORIT MARGIN

In relation to operating expense, “operating profit margin” means the ratio of operating profit, being the operating revenue in excess of operating expense, to the operating expense expressed in terms of percentage.

MEANING OF EMPLOYEE COST

It includes, –

- salaries and wages;

- gratuities;

- contribution to Provident Fund and other funds;

- the value of perquisites as specified in clause (2) of section 17;

- employment related allowances, like medical allowance, dearness allowance, travel allowance and any other allowance;

- bonus or commission by whatever name called;

- lump sum payments received at the time of termination of service or superannuation or voluntary retirement, such as gratuity, severance pay, leave encashment, voluntary retrenchment benefits, commutation of pension and similar payments;

- expenses incurred on contractual employment of persons performing tasks similar to those performed by the regular employees;

(ix) outsourcing expenses, to the extent of employee cost, wherever ascertainable, embedded in the total outsourcing expenses. However, where the extent of employee cost embedded in the total outsourcing expenses is not ascertainable, eighty per cent of the total outsourcing expenses shall be deemed to be the employee cost embedded in the total outsourcing expenses;

(x) recruitment expenses;

(xi) relocation expenses;

(xii) training expenses;

(xiii) staff welfare expenses; and

(xiv) any other expenses related to employees or the employment.

MEANING OF RELEVANT PREVIOUS YEAR

The previous year relevant to the assessment year in which the option for safe harbour is validly exercised.

SAFE HARBOUR RULES FOR INTERNATIONAL TRANSACTION

NOTES :

- The above provisions shall apply for A.Y. 2017-18, A.Y.2018-19 and A.Y.2019-20.

- No comparability adjustment shall be made to the transfer price declared by assessee and accepted under the Safe Harbour Rules given.

- Safe harbour rules shall not be applicable in respect of eligible international transaction entered into with an AE located notified Jurisdiction Area under section 94A or in a no tax or low tax country.

- Provisions of the IT Act, requiring maintenance of information and documents and furnishing of report in Form No 3CEB, shall apply irrespective of the fact that the assessee exercises his option for safe harbour Rules in respect of such transaction.

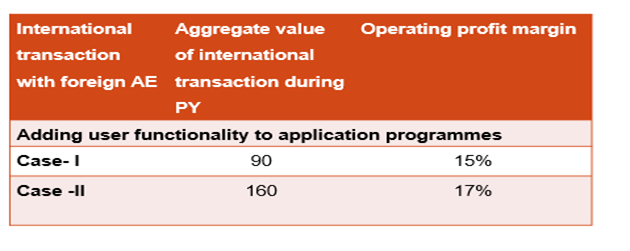

EXAMPLE 1: –

In following situations examine and discuss whether transfer price declared by assessee would be accepted when it had exercised a valid option of safe harbour rules:

SOLUTION : –

Providing user functionality to application programmes of foreign AE would be covered in the definition of ‘software development services’ under Safe Harbour Rules. Transfer price declared by assessee would be accepted –

- When the operating profit margin of assessee is 17% or more and value of international transaction is Rs 100 crore or less or

- When the operating profit margin of assessee is 18% or more and value of international transaction is Rs 200 crore or less.

CASE – I : –

Since the value of international transaction is less than Rs 100 crores the safe harbour margin should be 17% or more. In this case the safe harbour margin is 15%. Thus, income-tax authorities are not bound to accept the transfer price declared by assessee .

CASE – II : –

Since the value of international transaction is above Rs 100 crores but less than Rs 200 crores the safe harbour margin should be 18% or more. However, in this case the safe harbour margin is 17%. Thus, income-tax authorities are not bound to accept the transfer price declared by assessee.

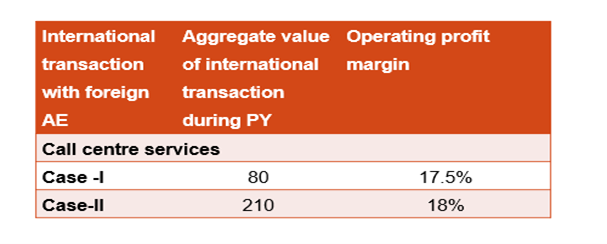

EXAMPLE 2: –

In following situations examine and discuss whether transfer price declared by assessee would be accepted when it had exercised a valid option of safe harbour rules:

SOLUTION : –

Call centre services provided to foreign AE would be covered in the definition of ‘Information Technology Enabled Services’ under Safe Harbour Rules. Transfer price declared by assessee would be accepted –

a. When the operating profit margin of assessee is 17% or more and value of international transaction is Rs 100 crore or less or

b. When the operating profit margin of assessee is 18% or more and value of international transaction is Rs 200 crore or less.

CASE – I : –

Since the value of international transaction is less than Rs 100 crores the safe harbour margin should be 17% or more. In this case the safe harbour margin is 17.5%. Thus, income-tax authorities are bound to accept the transfer price declared by assessee .

Case – II : –

In case of call centre services, the value of international transaction should not exceed Rs 200 crores. However, in this case the value of international transaction is Rs 210 crores. Thus, income-tax authorities are not bound to accept the transfer price declared by assessee.