SECONDARY ADJUSTMENT – SECTION 92CE

The Finance Act, 2017 has inserted the provision of “Secondary adjustment” to reflect that the actual allocation of profits between the assessee and its AE are consistence with the transfer price determined as a result of primary adjustment, thereby removing imbalance between cash account and actual profit of the assessee. The provision of secondary adjustment are applicable from the AY 2018-19.

MEANING OF SECONDARY ADJUSTMENT – SECTION 92CE(3)(V)

“Secondary adjustment” means an adjustment

in the books of accounts of

the assessee and its AE to reflect that the

actual allocation of profits between the assessee and its AE

are consistent with the transfer price determined

as a result of primary adjustment,

thereby removing the imbalance between

cash account and actual profit of the assessee.

FORMS OF SECONDARY ADJUSTMENT

As per the OECD’s Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations, secondary adjustment may be in the form of

- Constructive dividends,

- Constructive equity contributions, or

- Constructive loans.

The provisions of secondary adjustment seek to align the economic benefit of the transaction with the arm’s length position.

CASES WHERE SECONDARY ADJUSTMENT TO BE MADE

Section 92CE(i) provides that the assessee shall make secondary adjustment where the primary adjustment to transfer price has been : –

- made suo motu by the assessee in his return of income; or

- made by the Assessing Officer and has been accepted by the assessee; or

- determined by an advance pricing agreement entered into by the assessee u/s 92CC; or

- made as per the safe harbour rules framed u/s 92CB; or

- arising as a result of resolution of an assessment by way of the mutual agreement procedure.

NOTES : –

- As per Section 92CE(3)(iv) “Primary adjustment” to a transfer price means

-

- determination of transfer price

- in accordance with the arm’s length principle

- resulting in an increase in the total income or reduction in the loss, of the assessee.

- Secondary adjustment shall be made only when transfer pricing adjustment (i.e., primary adjustment) is accepted by assessee in aforesaid circumstances. Thus, secondary adjustment shall not be made when primary adjustment is challenged by assessee before income-tax authorities.

EXAMPLE : –

Analyse the following situations and determine whether secondary adjustment could be made ?

- ICO (Indian company) has imported certain goods from foreign AE for Rs 20 crores, for which it offered the ALP of 18 crores.

- ICO has filed ITR and TP report. AO made additions of Rs 5 crores on basis of ALP determined by TPO. Assessee challenged the order before Commissioner (Appeals).

- ICO has made additions of Rs 10 crore on basis of APA and filed the modified return.

- ICO filed the income-tax return on basis of MAP and made additions of Rs 4 crores.

SOLUTION : –

- Secondary adjustment shall be made only when transfer pricing adjustment (i.e., primary adjustment) is accepted by assessee. In this case suo-motu addition made by assessee in its income-tax return will be considered as primary adjustment. Accordingly secondary adjustment can be made subject to non satisfaction of repatriation condition.

- Secondary adjustment shall be made only when transfer pricing adjustment (i.e., primary adjustment) is accepted by assessee. In this case assessee has not accepted the primary adjustment made by Assessing Officer and therefore secondary adjustment cannot be made.

- Where the primary adjustment to transfer price has been determined by an APA, secondary adjustment can be made subject to non satisfaction of repatriation condition.

- Where the primary adjustment to transfer price has been arrived as a result of resolution of an assessment by way of the MAP, Secondary adjustment can be made.

NON-REPATRIATION OF EXCESS MONEY BY THE AE DEEMED TO BE AN ADVANCE

Where, as a result of primary adjustment to the transfer price,

there is an increase in the total income or

reduction in the loss of the assessee,

the excess money which is available with its AE,

if not repatriated to India within the specified time,

shall be deemed to be an advance made by the assessee to such AE and

the interest on such advance,

shall be computed as the income of the assessee, at the prescribed rates.

EXAMPLE : –

ICO sold goods to its foreign AE located in UK at Rs 10 crores during F.Y. 2017-18. TPO determined the ALP of such sale at Rs 13 crores. The AO made transfer pricing adjustment of Rs 3 crores. Calculate following items:

- Primary adjustment ?

- Excess money available with foreign AE ?

- Additions to be made due to Secondary adjustment ?

SOLUTION : –

- The transfer pricing adjustment of Rs 3 crores made by Assessing Officer will be the Primary Adjustment.

- Foreign AE would have paid Rs 13 crores to ICO instead of Rs 10 crores if transaction was carried out at Arm’s length price. Thus, excess money of Rs 3 crores (13-10) available with foreign AE should be repatriated to India within specified time.

- In case excess money is not repatriated to India within prescribed time-limit, such excess money of Rs 3 crores would be deemed as advance made by ICO to foreign AE and interest on such excess money shall be added to the income of the assessee due to secondary adjustment.

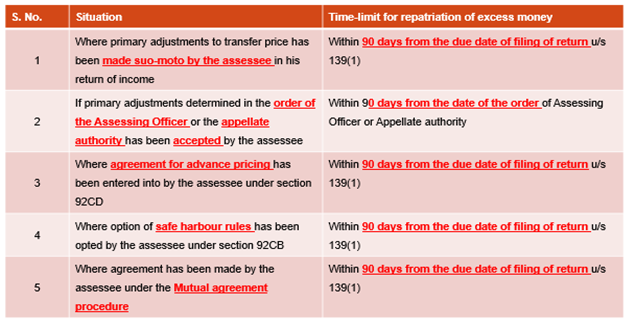

TIME-LIMIT FOR REPATRIATION OF EXCESS MONEY TO INDIA – RULE 10CB

EXAMPLE 1 : –

ICO (Indian Company) has imported certain goods from its foreign AE at Rs 20 crores. It determined arm’s length price of such transaction at Rs 15 crores. It made transfer pricing addition of Rs 5 crores in its income-tax return filed on November 30, 2018 for PY 2017-18. Determine the time-limit for repatriation of excess money to India ?

SOLUTION : –

Excess money available with foreign AE would be Rs 5 crores [i.e., the difference between actual transaction price (Rs 20 crores) and arm’s length price of Rs 15 crores]. In case primary adjustment has been made by assessee in its income tax return, excess money should be repatriated to India within 90 days from the due date of filing return of income.

Thus, excess money of Rs 5 crores should be repatriated to India till February 28, 2019.

EXAMPLE 2 : –

In the above example assume that assessee has opted for safe harbour rules. Other facts remain unchanged. Determine the time-limit for repatriation of excess money in such case.

SOLUTION : –

In this case also the excess money shall be repatriated to India within 90 days from the due date of filing of return. Thus, the time-limit for repatriation of excess money to India would be same (i.e., February 28, 2019).

SECONDARY ADJUSTMENT – TIME-LIMIT FOR REPATRIATION OF EXCESS MONEY TO INDIA – RULE 10CB

EXAMPLE 3 : –

ICO (Indian Company) has sold goods to its foreign subsidiary at Rs 10 crores during the FY 2017-18. The TPO determined the arm’s length price of such transaction at Rs 12 crores. Accordingly, the Assessing Officer made additions of Rs 2 crores in its order dated August 1, 2021. The ICO accepts the order of Assessing Officer. Determine the time-limit for repatriation of excess money to India ?

SOLUTION : –

Excess money available with foreign AE would be Rs 2 crores [i.e., the difference between actual transaction price (Rs 10 crores) and arm’s length price of Rs 12 crores]. In case this case, excess money should be repatriated to India within 90 days from the date of order of assessing officer.

Thus, excess money of Rs 2 crores should be repatriated to India till October 30, 2021.

EXAMPLE 4 : –

ICO (Indian Company) entered into an APA on September 1, 2018 for PY 2017-18. It filed its income tax return on November 30, 2018 as per the arm’s length price determined under APA. Determine the time-period for repatriation of excess money ?

SOLUTION : –

Excess money should be repatriated to India within 90 days from the due date of filing of income tax return. Thus, excess money should be repatriated to India till February 28, 2019.

EXAMPLE 5 : –

In the previous example assume that Indian company has filed its income tax return on November 15, 2018. Other facts remain unchanged. Determine the time-period for repatriation of excess money ?

SOLUTION : –

Excess money should be repatriated to India within 90 days from the due date of filing of income tax return. In this case period of 90 days should be counted with reference to November 30, 2018 even if income tax return has been filed before the due date of filing of return. Thus, excess money should be repatriated to India till February 28, 2019.

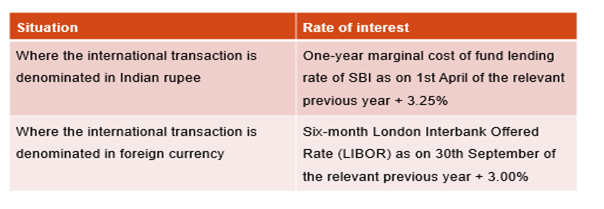

RATE AT WHICH INTEREST INCOME SHALL BE COMPUTED UNDER SECONDARY ADJUSTMENT – RULE 10CB

The excess money which is available with its AE, if not repatriated to India within the aforesaid time-limit, shall be deemed to be an advance made by the assessee to such AE. The interest income on such advance, shall be computed as per the following rate of interest :

EXEMPTION FROM SECONDARY ADJUSTMENT

Secondary adjustment shall not be carried out if, the

amount of primary adjustment in any previous year

does not exceed Rs 1 crore and

the primary adjustment is made in respect of A.Y.2016-

17 or an earlier assessment year.