DEEMED ASSOCIATED ENTERPRISES – SECTION 92A (2)

READERS INFORMATION: –

The general application of definition of AE , discussed in Section 92A(1) may not be sufficient to cover all cases of tax manipulation by various Enterprise, and may leave scope for manipulation in such a manner, that the issue whether two enterprise are AE’s is debatable.

For example, if an enterprise (A) participates to the extent of 2% in the capital of another enterprise (B), it may not result in exercising control on transactions of B, and may therefore not qualify as an AE of B. However, if A is the only purchaser of goods produced sold by B, it may still be able to exercise control prices /certain policies of B.

In order to address this situation, the concept of deemed AE, is introduced in Section 92A (2).

Section 92A (2) provides that two enterprises shall be deemed to be Associated Enterprises if, at any time during the previous year they satisfy any one or more of following 13 conditions . For identification of Associated enterprise, any of the aforesaid relationship should exist at any time during the previous year. It is not necessary that such relationship should exist throughout the year or atleast for some duration of time, before the relationship of Associated enterprise shall be deemed to exist.

Example : –

The following is the list of transaction between A Limited and its UK parent, Sigma UK. You are required to comment which transaction shall be covered under Transfer Pricing ?

Solution

Section 92A (2) provides that two enterprises shall be deemed to be Associated Enterprises if, at any time during the previous year they satisfy any one or more of conditions for being deemed associated enterprise. In the present case, on 31.12.2019, Sigma UK owns 45% stake in A Limited, and hence both the companies would be AE. Once two enterprise are AE during the year, all their transaction during the year are covered under TP irrespective of whether they were entered into before such date or after such date during that year. Hence all transaction between Sigma UK and A Limited for FY 2019-20 would be covered under TP.

Two entities fall under any of the following clauses, they shall be treated as AE’s , even though they may not be covered u/s Section 92A (1) : –

DIRECT OR INDIRECT VOTING POWER OF 26% OR MORE

One enterprise (FCO) holds, directly or indirectly, shares carrying 26% or more of the voting power in the other enterprise (ICO).

Note : –

In this case, the entity which owns the voting power, namely, FCO and the investee company (ICO), would be treated as Associated Enterprises.

Since only Equity share carry voting rights, the participation is generally based on ownership of such equity shares. Generally preference shares do not carry any voting rights, and therefore even if an enterprise owns more than 26% preference shares (which are non-voting) in another Enterprise, the two enterprise will not be treated as Associated Enterprises under this clause.

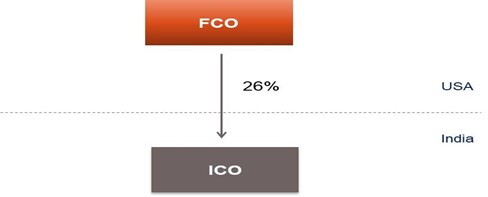

Example 1 : – DIAGRAM 1.19

Diagram 1.19

Facts :

- FCO holds 26% Equity Shares in ICO (all equity shares carry equal voting rights) .

Issue:

- Whether FCO and ICO will be deemed to be Associated enterprise ?

Solution:

- Since, FCO directly holds 26% voting rights in ICO, both FCO and ICO would be deemed to be Associated enterprise.

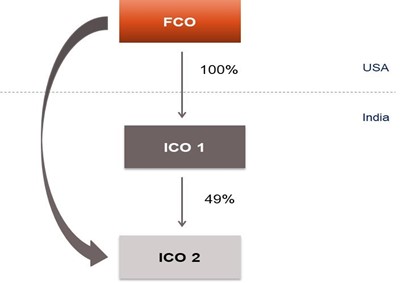

Example 2 : – DIAGRAM 1.20

DIAGRAM 1.20

Facts:

- FCO holds 100% equity shares (all equity shares carry equal voting rights) in ICO 1.

- ICO 1 holds 49% equity shares (all equity shares carry equal voting rights) in ICO 2.

Issue: Who all will be the Associated enterprises based on the above facts ?

Solution:

- Since, FCO directly holds 100% voting rights in ICO 1, both FCO and ICO1 would be deemed to be Associated enterprise.

- Since, ICO 1 directly holds 49% voting rights in ICO 2, both the enterprise are deemed to be Associated enterprise. However, since both ICO 1 and ICO 2 are Indian companies, the Transfer Pricing provision applicable to them would be Domestic Transfer Pricing provisions, and hence the coverage of transaction, threshold and conditions of Domestic Transfer Pricing provisions would need to be applied on transactions between them, if such transaction are covered under the Domestic Transfer Pricing provisions.

- FCO and ICO 2 will also be deemed to be the Associated enterprise because FCO indirectly holds more than 26% voting rights in ICO 2.

VOTING POWER/ OWNERSHIP > 26%

Any person or enterprise holds, directly or indirectly (to be discussed), shares carrying 26% or more of the voting power in each of such enterprises.

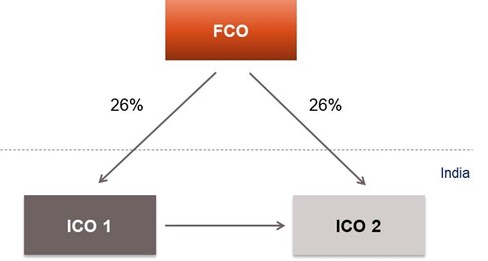

Example : – DIAGRAM 1.21

Consider the following diagram (% represents equity ownership) –

DIAGRAM 1.21

Facts : –

- FCO holds 26% equity shares in ICO 1; and

- FCO also holds 26% shares in ICO 2.

Issue : –

- Who all will be the Associated enterprises ?

Solution:

- Since, FCO directly holds 26% voting rights in ICO 1, both the enterprise would be deemed to be the Associated enterprise.

- Since, FCO directly holds 26% voting rights in ICO 2, both the enterprise would be deemed to be the Associated enterprise.

- Since, common person FCO, holds 26% voting rights in each of the enterprise ICO 1 and ICO 2, hence ICO 1 and ICO 2 will also be deemed to be the Associated enterprise. However, the Transfer Pricing provision applicable for transaction between ICO 1 and ICO 2 would be Domestic Transfer Pricing provisions.

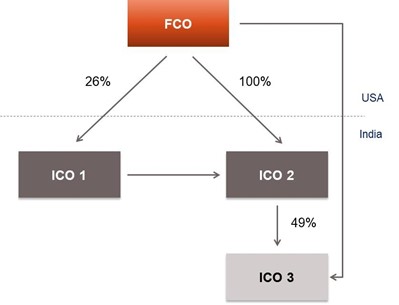

Example 2 : DIAGRAM 1.22

Consider the following diagram (% represents equity ownership) : –

DIAGRAM 1.22

Facts:

- FCO holds 26% equity shares in ICO 1; and

- FCO also holds 100% shares in ICO 2;

- ICO 2 holds 49% shares in ICO 3.

Issue:

- Who all will be Associated enterprises, based on the given facts ?

SOLUTION: –

Direct Participation

- FCO holds 26% voting rights in ICO 1. Hence both the companies would be deemed to be Associated enterprise.

- FCO holds 100% voting rights in ICO 2. Hence both the companies would be deemed to be Associated enterprise.

- ICO 2 holds 49% shares in ICO 3, and hence both the companies would be deemed to be Associated enterprise.

Common Participation

- Since, common person FCO holds 26% and more voting rights in ICO 1 and ICO 2, hence ICO 1 and ICO 2 will also be deemed to be Associated enterprise as regards transactions between themselves .

Indirect Participation

- FCO holds 100% voting rights in ICO 2, and ICO 2 in turn holds 49% voting rights in ICO 3. Hence, we can say that FCO indirectly holds more than 26% voting rights in ICO 3. Hence both FCO and ICO3 will be deemed to be Associated enterprise.

- Since, FCO indirectly holds more than 26% voting rights in ICO 3 and FCO directly holds 26% voting rights in ICO 1, hence, ICO 1 and ICO 3 will be deemed to be Associated enterprise.

LOAN OF 51% OR MORE OF TOTAL BOOK VALUE OF ASSETS

Where loan advanced by one enterprise, to the other enterprise constitutes 51% or more (less than 51% would not be covered under this clause) of the book value of the total assets of the other enterprise, the two enterprise would be deemed to be Associated Enterprises.

In such cases it is not necessary, that there should be a direct or indirect participation of 26% or more voting power by one enterprise into another Enterprise, or that there should be a common person who holds 26% or more voting rights in both the Enterprise.

The comparison needs to be made for the following : –

- Loan advanced by one enterprise ;

- Book value of the total assets of the other enterprise

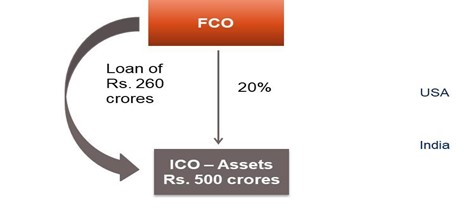

EXAMPLE 1 : –

Consider the following Diagram 1.23 : –

Diagram 1.23

Facts : –

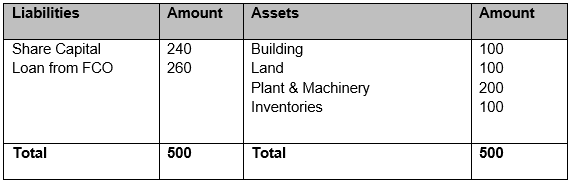

- FCO holds 20% voting rights in ICO, whose

- Balance sheet as on 31.3.2020 is as under : –

Issue: –

Whether FCO and ICO will be deemed to be Associated enterprise ? In the above case, what would be the answer, if the loan amount was 255 crores assuming other facts remain same?

SOLUTION: –

Loan Advanced by FCO = Rs. 260 crores

Book value of total assets to ICO = Rs. 500 crores

% of Loan Advanced by FCO to Book value of total assets to ICO = 260/500*100) % = 52%

Since, FCO has advanced loan of 52% of book value of total assets to ICO, FCO and ICO would be deemed to be the Associated enterprise.

Even if the loan amount was Rs. 255 crores, FCO would have advanced loan of 51% (255/500*100) % = 51%) of book value of total assets to ICO. Hence FCO and ICO would still be deemed to be the Associated enterprise. However, if the loan amount was less than Rs. 255 crores, FCO and ICO would not be deemed to be the Associated enterprise.

EXAMPLE 2: –

In the above case, what would be the position, if the loan amount was 250 crores? Other facts remain same.

SOLUTION: –

Since, FCO has advanced loan of less than 51% of book value (250/500*100)% = 50%) of total assets to ICO, FCO and ICO would not deemed to be the Associated enterprise.

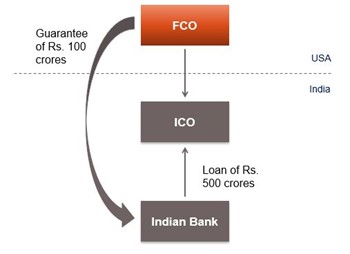

GUARANTOR OF 10% or more BORROWINGS – DIAGRAM 1.24

Where one enterprise (FCO) guarantees 10% or more of the total borrowings of the other enterprise (ICO), the two enterprise will be treated as Associated Enterprises. In such cases it is not necessary, that there should be a direct or indirect participation of 26% or more voting power by one enterprise into another Enterprise or that there should be a common person who holds 26% or more voting rights in both the Enterprise.

Consider the following examples : –

Example 1 : –

DIAGRAM 1.24

Facts:

- ICO has made borrowings of Rs. 500 crores from an Indian Bank;

- FCO, which owns 100% non convertible preference shares and 10% equity of ICO, has guaranteed the borrowings of Rs, 100 crores taken by ICO.

Issue:

Whether FCO and ICO will be deemed to be Associated Enterprise ?

Solution:

Since, FCO has guaranteed more than 10% of the total borrowings (i.e. 100/ 500 = 20%) of ICO, FCO and ICO are Associated Enterprise.

Example 2 : –

What would be the answer if the loan guaranteed was :

(a) Rs. 50 crores ?

(b) Rs. 49 crores ?

In case the borrowings were Rs. 50 crores, FCO would have guaranteed borrowings of ICO of 10% or more (50/500*100) % = 10%), and accordingly , FCO and ICO would be deemed to be the Associated enterprise.

In case the borrowings were Rs. 49 crores, FCO would have guaranteed borrowings of ICO of less than 10% (49/500*100) % = 9.8%) . Hence , FCO and ICO would not be deemed to be the Associated Enterprise under this clause.

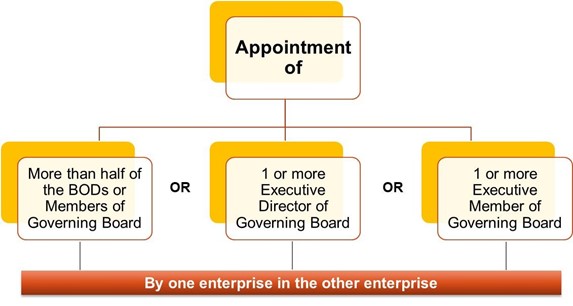

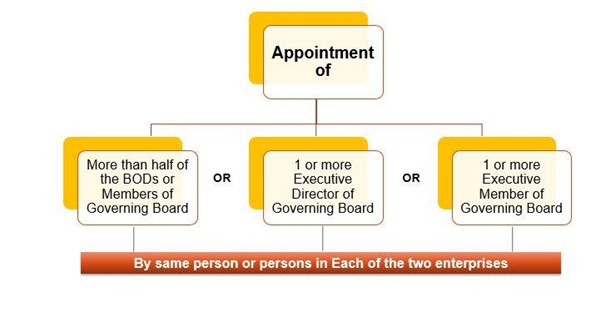

APPOINTMENT OF GOVERNING BOARD

Where one enterprise appoints

- More than half of the Board of Directors (3 out of 5) , or members of the Governing Board (1 out of 3), are appointed by the other enterprise, or

- One or more Executive Directors of the Governing Board are appointed by the other enterprise (1 or 1+), or

- One or more Executive Members of the Governing Board of one enterprise, are appointed by the other enterprise (1 or 1+).

In each of the above cases, the two enterprise will be treated as Associated Enterprises. In such cases , to constitute AE, it is not necessary, that there should be a direct or indirect participation of 26% or more voting power by one enterprise into another Enterprise or that there should be a common person who holds 26% or more voting rights in both the Enterprise.

Note : –

Actual appointment of Directors /Members is relevant for the application of this clause. Merely because the person has the power to appoint, without actual appointment will not make two enterprises Associated Enterprise.

DIAGRAM 1.25

EXAMPLE 1: –

In the following case, list out the Associated enterprises of ICO 1 : –

- FCO 1 has made the appointment of 12 out of 20 Board of Directors of the Governing Board in ICO 1.

- FCO 2 has made the appointment of Mr. B, as Executive Director of the Governing Board in ICO 1.

- FCO 3 has made the appointment of Mr. C as an Executive Member of the Governing Board in ICO 1.

SOLUTION: –

- Since, more than half of Board of Directors in Governing Board in ICO 1 have been appointed by FCO 1, FCO 1 and ICO 1 are deemed to be Associated enterprise.

- Since, an Executive Director in the Governing Board has been appointed in ICO 1 by FCO 2, FCO 2 and ICO 1 are deemed to be Associated enterprise.

- Since, an Executive Member in the Governing Board has been appointed in ICO 1 by FCO 3, FCO 3 and ICO 1 are deemed to be Associated enterprise.

EXAMPLE 2: –

- FCO has the power to appoint three out of five directors of Governing Board of ICO. However, due to certain disputes it was able to appoint only one director during FY 2016-17. Whether FCO and ICO are Associated enterprise ?

SOLUTION: –

Since, FCO has made appointment of less than 50% of Board of Directors of the Governing Board of ICO, FCO and ICO would not be considered as Associated enterprise. In such cases, it is the actual appointment which is the relevant for the purpose of ascertaining whether the two enterprise are Associated Enterprises. Merely because FCO has the power to appoint more than half of the board of Directors would not make FCO and ICO Associated Enterprise, unless such power has been exercised.

APPOINTMENT OF BOARD OF 2 DIFFERENT ENTERPRISES BY SAME PERSON

Where one or more person, have the power, to appoint

- More than half of the Board of Directors of each of the two enterprises , or members of the Governing Board of each of the two enterprises, or

- One or more Executive Directors of the Governing Board of each of the two enterprises, or

- One or more Executive Members of the Governing Board of each of the two enterprises, in such a case, each of the two enterprise would be deemed to be Associated Enterprise, between themselves, as well as with the person who has the power to appoint Board of Directors , or Executive Directors.

DIAGRAM 1.26

In such cases it is not necessary, that there should be a direct or indirect participation of 26% or more voting power by one enterprise into another Enterprise or that there should be a common person who holds 26% or more voting rights in both the Enterprise.

EXAMPLE : –

FCO 1, (US Company) has made the following appointments in ICO (Indian Company) and FCO (US Company) :

- An Executive Director in both FCO and ICO; or

- 8 out of 12, Directors on Board in FCO and 7 out of 13, Directors on Board in ICO.

Identify who all would be treated as AE’s in the transaction ?

SOLUTION: –

a) An Executive Director has been appointed in FCO and ICO by FCO 1, hence, FCO 1 & FCO , and FCO 1 & ICO, are deemed to be the Associated enterprise as FCO1 has the power to appoint Executive Director in FCO and ICO.

(b) Since FCO 1, a common person has appointed more than half of Board of Directors of the Governing Board, both in FCO (8 out of 12) and ICO (7 out of 13), FCO and ICO are Associated Enterprise

Further, since more than half of Board of Directors in FCO and ICO have been appointed by FCO 1, hence, FCO 1 & FCO, and FCO 1 & ICO are deemed to be the Associated Enterprise.

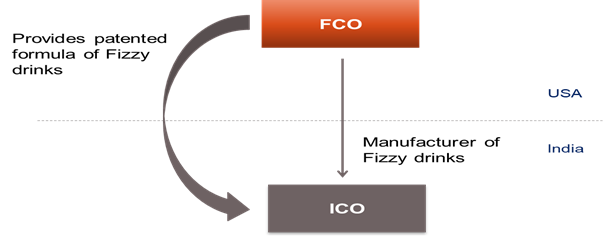

DEPENDENCE ON INTANGIBLES WHICH ARE OWNED BY OR UNDER EXCLUSIVE RIGHT OF ANOTHER ENTERPRISE

Where the business of one enterprise (ICO), or manufacture or processing of goods or articles by one enterprise (ICO), is wholly dependent on

- the know-how, patents, copyrights, trade-marks, licenses, franchises, or any other business or commercial rights of similar nature, or

- any data, documentation, drawing or specification relating to any patent, invention, model, design, secret formula or process

and the other enterprise (FCO), is either the owner, or has exclusive rights to such assets, the two are treated as AE’s.

This clause intends to cover cases where the business of one Enterprise (“ICO”) is significantly dependent upon, certain intangibles, which are either owned by another Enterprise (“FCO”), or such other Enterprise (“FCO”), has exclusive right over them. In such cases, given the dependence of the first mentioned Enterprise (“ICO”), it is assumed, that the owner of intangibles (“FCO”) would be able to exercise significant influence on the business of the first mentioned enterprise (“ICO”) and therefore affect the prices of the transaction.

DIAGRAM 1.27

Facts : –

- ICO (India) manufactures Fizzy drinks by using patented formula owned by a FCO (USA).

- The manufacture of Fizzy drink by ICO is wholly dependent on use of secret patented formula owned by a FCO.

Issue:

- Whether FCO and ICO will be deemed to be Associated enterprise ?

Solution:

Both the enterprises will be deemed to be Associated enterprise u/s 92A(2)(vii), because the business of ICO is wholly dependent on the use of patent provided by FCO.

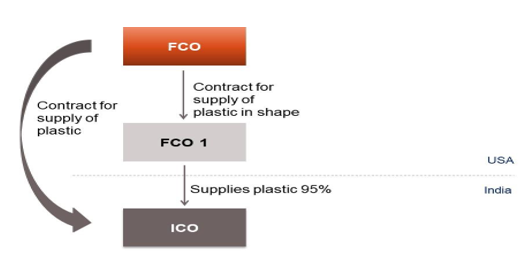

DEPENDENCE ON RAW MATERIALS AND CONSUMABLE

Where 90% or more of raw materials and consumables, required for the manufacture or processing of goods or articles or carrying on of business carried out by one enterprise (ICO), are supplied by

- the other enterprise (FCO), or

- by persons specified by the other enterprise (FCO1), and the prices and other conditions relating to the supply are influenced by such other enterprise.

This clause intends to cover cases where the business of one Enterprise is significantly dependent on raw material supplied by another Enterprise, or by person, specified by such another enterprise, who also influences price and conditions, of supply made by the specified person. In such cases, given the dependence of the first mentioned Enterprise, it is assumed, that the supplier of raw material would be able to exercise significant influence on the business of the first mentioned enterprise, and therefore affect the prices of the transaction. Hence the buyer and supplier are treated as AE’s.

The comparison is to be made based on the value of raw material and consumables.

DIAGRAM 1.28

FCO and ICO will be deemed to be Associated Enterprise because 90% or more than 90% of the goods are supplied by FCO 1 to ICO i.e. the person specified by the other enterprise (FCO) provided the price and other conditions of supplies made by FCO1 are specified by FCO.

Facts:

- ICO manufactures chairs, using plastic manufactured by FCO. FCO sub-contracted the reshaping part of plastics to FCO 1. FCO 1 reshapes the plastic purchased from FCO and on the instructions of FCO sells it to ICO.

- 95% of the plastic consumed by ICO was supplied by FCO 1 out of total plastic consumed by it amounting Rs. 190 crores out of total raw material requirements of Rs. 200 crores.

- Prices and other conditions are decided by FCO in terms of contract between FCO and FCO 1.

Issue : –

- Who all will be deemed to be the Associated enterprise?

Solution

FCO and ICO would be treated as AE, as 90% or more of raw materials and consumables, required for the manufacture by ICO, are supplied by persons (FCO1) specified by the other enterprise (FCO).

EXAMPLE 2: –

In the above case, what would be the position, if the raw material supplied by FCO amounts to Rs. 170 crores out of total raw material consumed of Rs. 200 crores? Other facts remain same.

SOLUTION: –

Since, FCO has supplied less than 90% of the raw material required by ICO, FCO and ICO would not be deemed to be the Associated enterprise

EXAMPLE 3: –

In the above case, what would be the position, if the raw material supplied by FCO amounts to Rs. 180 crores out of total raw material consumed of Rs. 200 crores? Other facts remain same.

SOLUTION: –

Since, FCO has supplied 90% of the raw material required by ICO, both FCO and ICO would be deemed to be the Associated enterprise.

DEPENDENCE ON SALE

Where, the goods or articles manufactured or processed by one enterprise (A) , are sold

- to the other enterprise (B) ; or

- to persons specified by the other enterprise (C ) , and the prices and other conditions relating thereto are influenced by such other enterprise (B).

such enterprise (A and B) would be deemed to be Associated Enterprises.

This clause intends to cover cases where the sales of one Enterprise (A) are so significantly dependent on another Enterprise (B) /person specified by such another Enterprise (C ), that without the buyer (B or C ), the business of the first mentioned Enterprise (A )would not exist. In such a case, it is assumed, that the buyer (B) would be able to exercise significant influence on the business of the first mentioned enterprise, and therefore affect the prices of the transaction.

Facts:

- ICO is engaged in manufacturing of bikes in India.

- It supplied all the bikes it made to FCO, a US Company.

Issue:

- Whether FCO and ICO will be deemed to be Associated enterprise?

Solution:

- Since ICO has supplied all the bikes manufactured by it to FCO, both FCO and ICO will be deemed to be Associated enterprise as goods or articles manufactured or processed by one enterprise, are sold to the other enterprise.

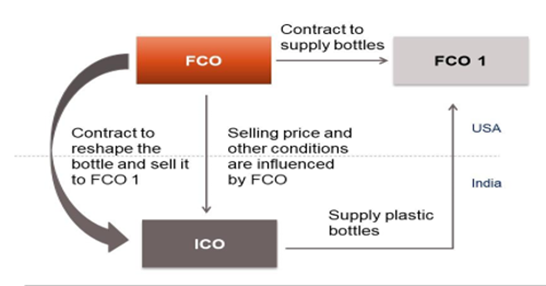

Example 2 : –

Facts:

- FCO 1, a US Co. is engaged in the business of branding and trading of plastic bottles. FCO 1 uses the plastic bottles manufactured by FCO.

- FCO sub-contracts the manufacturing of bottles to ICO.

- ICO (an Indian company whose entire sale are made to FCO1) imports plastic from FCO, reshapes the plastic imported from FCO in bottles and on instructions of FCO, and sells it to FCO 1.

- Price and other conditions of such sale are influenced by FCO .

Issue:

- Whether FCO and ICO will be deemed to be the Associated enterprise

DIAGRAM 1.29

SOLUTION :-

In this case, bottles manufactured by ICO is sold to FCO1 on the instructions of FCO. Further, price and other conditions of such sale are influenced by FCO. Thus, ICO and FCO would be deemed to be associated enterprises.

SECTION 92A(2) – INDIVIDUAL AND RELATIVE CONTROL OVER DIFFERENT ENTERPRISE

The following two enterprises would also be deemed to be Associated Enterprises : –

- Where one enterprise is controlled by an individual, and the other enterprise is also controlled by such individual, or

- Where one enterprise is controlled by an individual, and the other enterprise is controlled by relative of such individual, or

- Where one enterprise is controlled by an individual, and the other enterprise is also controlled jointly by such individual and relative of such individual.

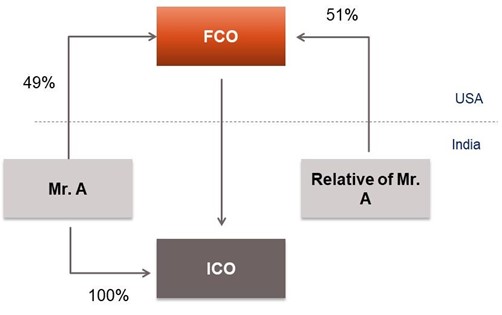

Example : – DIAGRAM 1.30

Consider the following Figure : –

Facts:

- Mr. A controls Indian company (ICO),

- Foreign Company (FCO) is controlled by

- Situation 1 – A

- Situation 2 – Relative of Mr. A

- Situation 3 – Jointly by Mr. A and relative of Mr. A.

Issue:

- Whether FCO & ICO will be deemed to be Associated enterprise ?

Solution:

- Situation 1 – Since, ICO is controlled by Mr. A and FCO is also controlled by Mr. A, both FCO and ICO will be deemed to be the Associated enterprise.

- Situation 2 – Since, ICO is controlled by Mr. A and FCO is also controlled by relative of Mr. A, , both FCO and ICO will be deemed to be the Associated enterprise.

- Situation 3 – Since, ICO is controlled by Mr. A and FCO is Jointly by Mr. A and his relative, both FCO and ICO will be deemed to be the Associated enterprise.

SECTION 92A(2) – CONTROL BY HUF AND MEMBERS

The following two enterprises would also be deemed to be Associated Enterprises :

- Where one enterprise is controlled by a Hindu Undivided Family (“HUF”), and the other enterprise is controlled by a member of such HUF (HUF + {Member of HUF}), or

- Where one enterprise is controlled by a HUF, and the other enterprise is controlled by a relative of a member of such HUF (HUF + {Relative of such member}),, or

- Where one enterprise is controlled by a Hindu Undivided Family (“HUF”), and the other enterprise is controlled by jointly by such member and his relative (HUF + {Member of HUF + relative of such member.

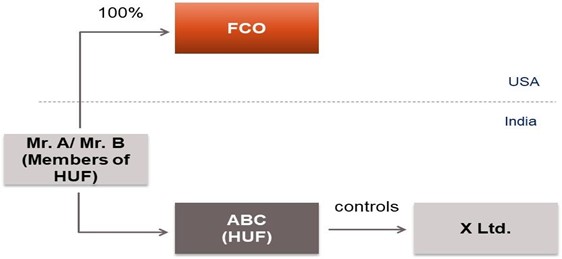

Example 1 – DIAGRAM 1.31

DIAGRAM 1.31

Facts : –

- HUF controls X Ltd., and

- Mr. A and Mr. B are the members of HUF.

- Members of HUF control FCO.

Issue:

- Whether FCO & X Ltd. will be deemed to be Associated enterprise ?

Solution:

- Since, FCO is controlled by members of HUF, and HUF itself controls X Ltd., hence, both FCO and X Ltd. will be deemed to be the Associated enterprise.

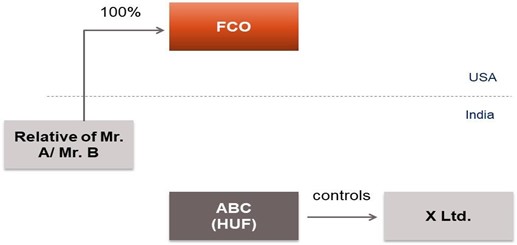

Example 2 – DIAGRAM 1.32

DIAGRAM 1.32

Facts:

- HUF controls X Ltd., and

- Mr. A and Mr. B are the members of HUF.

- Relative of Mr. A/ Mr. B control FCO.

Issue:

- Whether FCO & X Ltd. will be deemed to be Associated enterprise ?

Solution:

- Since, FCO is controlled by relative of members of HUF , and HUF itself controls X Ltd., both FCO and X Ltd. will be deemed to be the Associated enterprise.

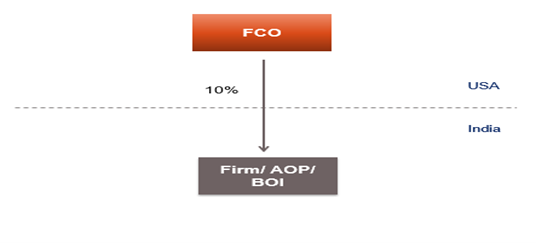

SECTION 92A(2) – ENTERPRISE HOLDING NOT LESS THAN 10% IN A FIRM DIAGRAM 1.33

The two enterprises given below would also be deemed to be Associated Enterprises : –

- Where one enterprise is a Firm and the other enterprise holds 10% or more interest in such Firm,

- Where one enterprise is an Association of Persons (“AOP”) and the other enterprise holds 10% or more interest in such AOP, or

- Where one enterprise is a Body of Individuals (“BOI”) and the other enterprise holds 10% or more interest in such BOI

DIAGRAM 1.33

Facts:

- FCO holds 10% voting rights in a firm/ an association of persons or body of individuals, incorporated in India.

Issue:

- Whether FCO and Firm/ AOP/ BOI will be deemed to be the Associated enterprise?

Solution:

- Both the enterprise will be deemed to be Associated enterprise because FCO holds not less than 10% interest in the Firm/ AOP/ BOI.

SECTION 92A(2) – MUTUAL INTEREST RELATIONSHIP

There exists between two enterprises, any relationship of mutual interest, as may be prescribed.

QUESTION AND ANSWERS ON ASSOCIATED ENTERPRISE

QUESTION 1: –

Advitya India Ltd. holds 26% non-voting Preference shares in AB International (Mauritius). Whether Advitya India Ltd.. and AB International (Mauritius), are Associated enterprise ?

SOLUTION: –

Advitya India Ltd. and AB International are not AE. Since Preference shares do not carry any voting rights., Advitya India Ltd. does not hold shares carrying 26% voting rights in AB International . Hence the two entities are not Associated Enterprises.

QUESTION 2 : –

D Ltd. (India) holds 100% Equity shares in V International (USA). Further, V International holds 100% Equity shares in Z International (UK). Who all would be the Associated enterprises ?

SOLUTION : –

- D Ltd. & V International are Associated enterprise, since D Ltd. owns > 26% voting rights in V International.

- V International and Z International are Associated enterprise, since V International owns > 26% voting rights in Z International.

- D Ltd. and Z International would also be Associated enterprise as D Ltd. indirectly holds more than 26% voting rights in Z International.

QUESTION 3: –

G Ltd. (India) holds 30% Equity shares in VZ Ltd. (India). It also holds 25% Equity shares in XZ International (UK). Who all would be the Associated enterprises ?

SOLUTION: –

- G Ltd. & VZ Ltd. are Associated enterprise, since G Ltd. owns > 26% voting rights in VZ Ltd.

- VZ Ltd. and XZ International are not Associated enterprise as G Ltd. does not hold 26% voting rights in XZ International.

QUESTION 4: –

Y Ltd. (India) holds 30% Equity shares in R Ltd. (India) and 40% Equity shares in Z International (UK). Who all would be the Associated enterprises?

SOLUTION: –

- Y Ltd. & R Ltd. are Associated enterprise, since Y Ltd. owns > 26% voting rights in R Ltd.

- Y Ltd. & Z International are Associated enterprise, since Y Ltd. owns > 26% voting rights in Z International.

- R Ltd. and Z International are Associated enterprise as Y Ltd. (common enterprise) holds more than 26% voting rights, in both the Companies.

QUESTION 5 : –

X Ltd. (India) holds 10% Equity shares in Z International (Switzerland) as on April 1, 2019. It further acquired Equity shares in Z International so that its aggregate shareholding reached at 30% as on November 1, 2019. Whether X Ltd. and Z International would be the Associated enterprise for FY 2019-20 ?

SOLUTION: –

- X Ltd. and Z International are Associated enterprise for F.Y. 2019-20.

- The condition of 26% voting right should exist at any time during the previous year.

- Once that condition is satisfied, then both enterprises shall be deemed to be AE for the entire year.

QUESTION 6 : –

R Ltd. (India) holds 35% Equity shares in T International (Russia) as on April 30, 2019. However, it sold 10% shares on December 1, 2019 to Acqua Singapore Pte Ltd.. Whether R Ltd. and T International would be the Associated enterprise for FY 2019-20?

SOLUTION: –

- R Ltd. and T International are Associated enterprise for F.Y. 2019-20.

- The condition of 26% voting right should exist at any time during the previous year.

- Once that condition is satisfied, then any subsequent reduction in shareholding in same year does not affect the status of Associated enterprise.

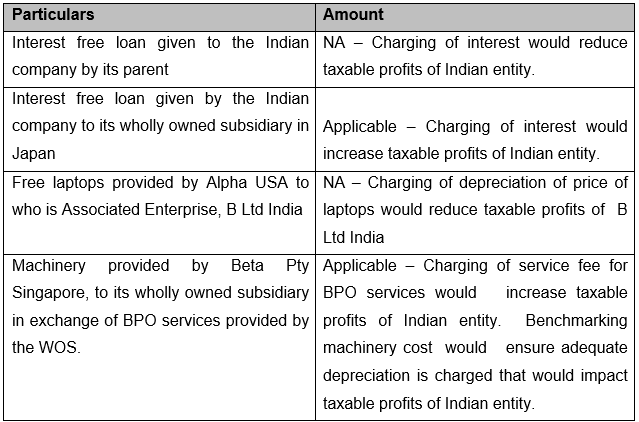

Case Study – Applicability of Transfer Pricing and Base Erosion

Identify whether transfer pricing provisions would be applicable on the following transactions : –

- Interest free loan given to the Indian company by its parent

- Interest free loan given by the Indian company to its wholly owned subsidiary in Japan

- Free laptops provided by Alpha USA to who is Associated Enterprise, B Ltd India

- Machinery provided by Beta Pty Singapore, to its wholly owned subsidiary in exchange of BPO services provided by the WOS.

Solution

Transfer Pricing regulations are designed to prevent shifting of profits, by manipulating prices charged by overseas entity or paid by Indian entity in international transactions, thereby eroding the country’s tax base. However in certain cases, application of the Transfer Pricing provisions, may result in reduction of profits taxable in India or increase the expenses, allowable as a deduction for Indian tax purposes. In such cases, Transfer Pricing provision are not required to be applied where the adoption of the arm’s length price would result in a decrease in the overall tax incidence in India in respect of the parties involved in the international transaction. In view of this, the specific comments are as under : –

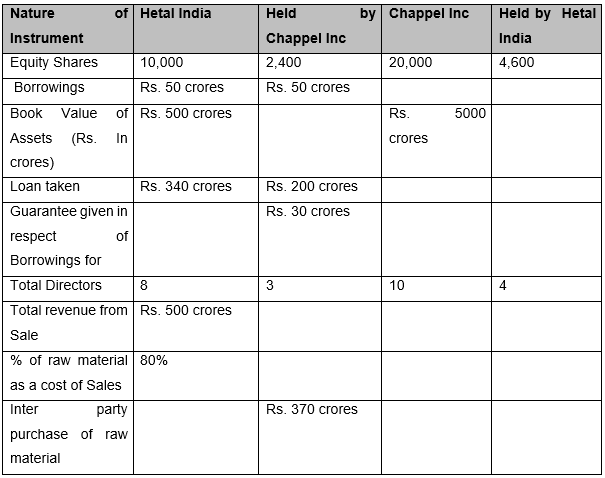

Case Study – Whether two Enterprise are Associated Enterprise?

(a) Based on the following data, you are required to ascertain whether Chappel Inc., and Hetal India Private Limited, are Associated Enterprises, in respect of each of these criterion (assume each one of them on a standalone basis): –

(b) Which transaction will be covered under the Transfer Pricing provisions, if Chapell Inc. held 30% of the equity share capital of Hetal India?

Solution

(a) The various criterion, and whether Hetal India or Chappel Inc, would be considered as AE’s are discussed as under: –

- Since Hetal India or Chappel Inc, does not have more than 26% equity share capital of Chappel Inc. (24%) or vice versa (23%), the two parties would not be considered as AE’s;

- Since, Chappel Inc has advanced loan of 40% (500/200*100) % = 40%) of book value of total assets to Hetal India, the two parties would not be considered as AE’s ;

- Since, Chappel Inc. has guaranteed less than 10% of the total borrowings (i.e. 30/ 500 = 6%) of Hetal India, the two parties would not be considered as AE’s ;

- Hetal India or Chappel Inc would not be treated as AE, as 90% or more of raw materials and consumables, required for the manufacture by ICO, are not supplied by Chappel Inc (Rs. 320/Rs. 400*100) = 80%. The total cost of raw material of Hetal India is 80% of Rs. 500 crores = Rs. 400 crores

- Since, Hetal India has made appointment of less than 50% of Board of Directors of Chappel Inc (4/10 = 40%) , the two enterprise would not be considered as Associated enterprise. Similarly, since, Chappel Inc has made appointment of less than 50% of Board of Directors of Hetal India (3/8 = 37.5 %) , the two enterprise would not be considered as Associated enterprise.

- b) If Chappel Inc,, has more than 26% equity share capital of Hetal India the two parties would be considered as AE’s , and all the transaction between them would be covered under the Transfer pricing provisions.

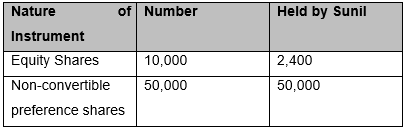

Case Study – Associated Enterprise and Penalties under Transfer Pricing

Fulcrum India Private Ltd., is an Indian company in which Sunil holds following shareholding : –

During financial year 2018-19, Fulcrum India paid a remuneration of Rs. 5 crores to Sunil, who is a non-resident. Fulcrum India failed to report the above transaction in its Transfer Pricing filing. What will be the amount of penalty which shall be leviable on account of this default ?

Solution

Two persons would be treated as Associated Enterprises, where one person holds, directly or indirectly, shares carrying 26% or more of the voting power in the other enterprise . In the present case, since Sunil holds 24% equity share capital of Fulcrum India Private Ltd. and 100% non-convertible preference shares, it cannot be said that Sunil holds 26% or more of the voting power in Fulcrum. In view of this, the two parties would parties not be considered as AE’s, and accordingly this transaction would be outside the purview of Transfer Pricing. In view of this, no penalty shall be levied on Fulcrum India Private Ltd .

Authors Note

Similar to the question above, the students can get the problem in the examination , where they may be asked to quantify the penalty applicable for non-compliance of Transfer Pricing provisions. In every such problem the following approach should be adopted : –

- Ascertain whether the parties involved in the transaction are Associated Enterprises ?

- Ascertain, whether there is any default /delay in complying with the Transfer Pricing provisions ?

- If the answer to both the above question is Yes, quantify the applicable penalties. If the answer to either of the above questions is No, no penalty shall be applicable.