Under Cost plus method, the arm’ s length price is determined by adding appropriate gross profit margin, also known as the “mark up”, (considering the function performed, return on capital and risk assumed by an entity) to the AE’s cost of producing goods/ cost of providing services.

In other words, ALP =

AE’s cost of producing goods/ providing services = A

Appropriate gross profit margin = B

Arm’ s length price = AE’s cost of producing goods/ providing services + Appropriate gross profit margin

Arm’ s length price = A + B

This method is most suitable in cases, where a manufacturer sells tangible goods to both related and unrelated parties.

As per the Organisation for Economic Co-operation and Development (OECD), CPM method is applicable when,

- Semi-finished goods are sold between Associated Enterprises ;

- There are long term supply and purchase agreements between Associated Enterprises;

- Provision of services between Associated Enterprises ;

- Agreements relating to contract manufacturing, between Associated Enterprises.

STEPS INVOLVED IN CPM

STEP 1 : – Direct and indirect costs of production

Determine the direct and indirect costs of production in a tested party transaction.

Note : – Such Direct and Indirect cost should be in respect of property transferred or services provided to an Associated Enterprise.

STEP 2 : – Determine normal gross profit mark-up to such costs

Determine the amount of a normal gross profit mark-up to such costs, arising from the transfer or provision of the same or similar goods or services : –

- By the enterprise itself, (i.e., transfer of similar goods or services by the enterprise – Internal comparable), in a comparable uncontrolled transaction (i.e not with a related party) , or a number of such transactions. or

- By an unrelated enterprise to another unrelated enterprise (i.e., transfer of similar goods or services between unrelated parties) – External comparable, in a comparable uncontrolled transaction, or a number of such transactions

STEP 3 : – Adjust for functional and other differences

The normal gross profit mark-up determined above shall be adjusted to account for the functional and other differences, between the entity being evaluated and the comparable company.

Note : –

Adjustment is to be made only if difference could materially affect such profit mark-up in the open market

STEP 4 : – Increase cost by the adjusted profit mark-up

The costs referred to in Step 1, shall be increased by the adjusted profit mark-up calculated in Step 3 leads to arm’s length price.

Case Study – Cost Plus Method

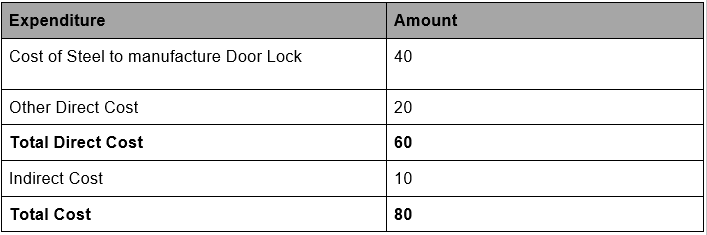

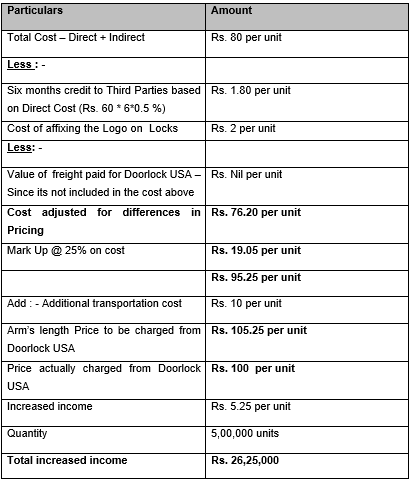

Doorlock India is a company incorporated under the Companies Act, 2013, a wholly owned subsidiary of Doorlock USA, and has a factory in Haryana. It is engaged in manufacture of door locks , door handle and other security product. Amongst several other products, the company manufactures, Category A door lock for which the details are as under : –

During FY 2018-19, it sold 5,00,000 pieces of such locks to Doorlock USA @ Rs.100 per lock (including transportation cost). There were following differences which were available between sale of Category A door lock to third party buyers (included in the above cost ) : –

- Third parties require affixing their Logo on the Locks for which indirect cost of Rs. 2 per lock is incurred.

- Credit period of 6 months is given to third parties while sale to Doorlock USA is on advance basis. The credit cost can be assumed at 5% per month of Direct Cost of the Product

- Goods are sold and delivered to Doorlock USA at their warehouse while in case of third parties, goods are delievered at the Godown of seller. Additional transportation cost is Rs. 10 per unit. Assume there is no mark up on freight charged by company.

Compute the arm’s length price, assuming a margin of 25% on Cost is earned from unrelated parties.

Solution

Cost of Producing Goods

Case Study 12 – Transfer Pricing – Computing Arm’s Length Price using cost plus method

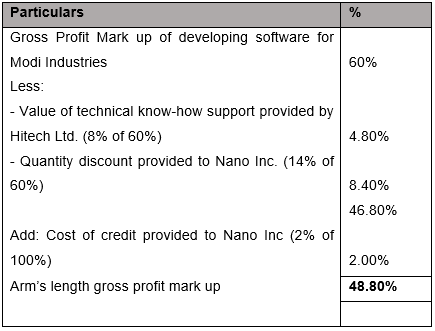

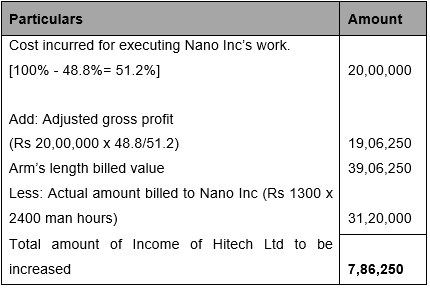

NANO Inc., a German Company, holds 45% of equity in Hitech Ltd., an Indian Company. Hitech Ltd. is engaged in development of software and maintenance of the same for customers across the globe. Its clientele includes NANO Inc.

During the financial year 2018-19, Hitech Ltd. had spent 2400 man hours for developing and maintaining software for NANO Inc. with each hour being billed at Rs 1,300. Cost incurred by Hitech Ltd. for executing work for NANO Inc. amounts to Rs 20 lakhs.

Hitech Ltd. had also undertaken developing software for Modi Industries, for which Hitech Ltd. had billed at Rs 2,700 per man hour. The persons working for Modi Industries and NANO Inc. were part of the same team and were of matching credentials and calibre. Hitech Ltd. made a gross profit of 60% on Modi Industries work. Hitech Ltd.’s transactions with NANO Inc. are comparable to transactions with Modi Industries, subject to the following differences:

(i) NANO Inc. gives technical knowhow support to Hitech Ltd., which can be valued at 8% of the normal gross profit. Modi Industries does not provide any such support.

(ii) Since the work for NANO Inc. involved huge number of man hours, a quantity discount of 14% of normal gross profits was given.

(iii) Hitech Ltd. had offered 90 days credit to NANO Inc., the cost of which is measured at 2% of the normal billing rate. No such discount was offered to Modi Industries.

Compute arm’s length price as per cost plus method and the amount of increase in total income of Hitech Ltd.

Solution

Computation of Arm’s Length Gross Profit Mark Up

Case Study – Transfer Pricing – Computing Arm’s Length Price and adjustment thereof

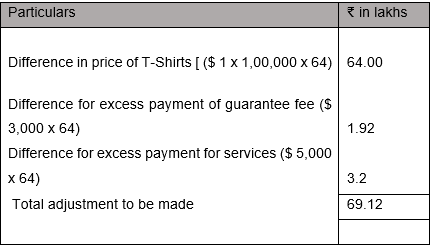

XE Ltd. is an Indian Company in which Zilla Inc., a US company, has 28% shareholding and voting power. Following transactions were effected between these two companies during the financial year 2018-19.

(i) XE Ltd. sold 1,00,000 pieces of T-shirts at $ 2 per T-Shirt to Zilla Inc. The identical T-Shirts were sold to unrelated party namely Kennedy Inc., at $ 3 per T-Shirt.

(ii) XE Ltd. borrowed $ 2,00,000 from a foreign lender based on the guarantee of Zilla Inc. For this, XE Ltd. paid $ 10,000 as guarantee fee to Zilla Inc. To an unrelated party for the same amount of loan, Zilla Inc. collected $ 7000 as guarantee fee.

(iii) XE Ltd. paid $15,000 to Zilla Inc. for getting various potential customers details to improve its business. Zilla Inc. provided the same service to unrelated parties for $ 10,000.

Assume the rate of exchange as 1 $ = ₹ 64

XE Ltd. is located in a Special Economic (SEZ) and its income before transfer pricing adjustments for the year ended 31st March, 2019 was Rs 1,200 lakhs.

Compute the adjustments to be made to the total income of XE Ltd. State whether it can claim deduction under section 10AA for the income enhanced by applying transfer pricing provisions .

Answer

As per section 92A(2) of the IT Act, two enterprises shall be deemed to be associated enterprises, where one enterprise holds 26% of the voting power in other enterprise . In this case, Zilla Inc. holds 28% shareholding and voting power in XE Ltd, thus both companies shall be deemed to be associated enterprises .

As section 92B of the IT Act, transactions of sale of product, lending or borrowing guarantee or guarantee and provision of services between associated enterprises shall be treated as “international transaction”.

Thus, transfer pricing provisions shall be attracted in this case.

Computation of adjustment to be made to total income of XE Ltd.

As per proviso to section 92C(4), no deduction under Section 10AA shall be allowed in respect of the amount of income by which the total income of the assessee is enhanced after computation of income under this sub-section . Accordingly, XE Ltd. cannot claim deduction under section 10AA in respect of amount of Rs 69.12 lakhs by which the total income of XE Ltd. is enhanced .

Case Study – Transfer Pricing – Computing Arm’s Length Price and adjustment thereof

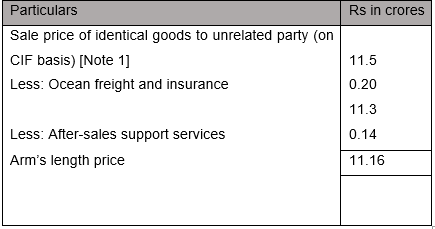

VKS Internationals Ltd., the assessee, has sold goods on 12-1-2018 to L Ltd., located in a notified jurisdictional area (NJA), for Rs 10.5 crores. The sale price of identical goods sold to an unfamiliar customer in New York during the year was Rs 11.5 crores. While the second sale was on CIF basis, the sale to L Ltd. was on F.O.B. basis. Ocean freight and insurance amount to Rs 20 lacs.

India has a Double Taxation Avoidance Agreement with the U.S.A.

The assessee has a policy of providing after-sales support services to the tune of Rs 14 lacs to all customers except L Ltd.

The ALP worked out as per Cost plus method for identical goods is Rs 12.1 crores.

You are required to compute the ALP for the sales made to L Ltd., and the amount of consequent increase, if any, in profits of the assessee company.

Solution

If the assessee enters into a transaction, where one of the parties to the transaction is a person located in a NJA then , the following provision shall apply :

- All parties to the transaction would be deemed as AE, even though they may not be covered as an AE under the provision of the IT Act ;

- Such transaction would be deemed to be international transaction as per section 92B; and

- All the provisions of Transfer Pricing, including such transaction being at an arm’s length conditions, would be attracted in case of such transactions.

In this case L Ltd. is located in Notified Jurisdiction Area. Thus, the transaction of sale of goods by VKS International Ltd. to L ltd. shall be deemed to be an international transaction and L ltd. and VKS International Ltd shall be deemed to be associated enterprises. Accordingly, the transfer pricing provisions shall be attracted in this case.

Section 92C provides that the ALP shall be determined by most appropriate method, having regard to the nature of transaction or other relevant factors .

The ALP of the transaction with L Ltd. shall be computed as under :-

In this case, as Rs 11.16 is taken as the ALP of sale of goods to L ltd., the profits of VKS International shall be increased by an amount of difference between ALP and actual transaction price of Rs 10.50 crores . Thus, in this case an adjustment of Rs 66 lakhs [Rs 11.16 crore – Rs 10.50 crore] shall be made to the taxable profits of VKS International .

Notes:

- VKS international has sold goods to unrelated customer at Rs 11.5 crores, thus, it would be treated as internal CUP . Such price or internal CUP shall be taken as ALP after making certain adjustments .

- In this case, we can either apply CUP method or Cost Plus Method in order to determine the ALP of goods sold by VKS International . As per the Guidance Note on transfer pricing Cost Plus Method is used where raw materials or semi-finished goods are sold or where joint facility agreements or long-term buy- and-supply arrangements, or provision of services are involved. In this case, goods sold are finished goods and it does not fall in any other aforesaid case, thus, we cannot apply Cost Plus Method in this case.

- In this case, we will work out ALP of goods using the CUP Method since the transaction in this case involves transfer of goods and the exact nature of goods transferred is not given .

Judicial Rulings on the Selection of Cost Plus Method