Meaning of Forfeiture of Shares Class

A shareholder who subscribes to shares is required to make total amount payable for subscription of such shares, in various installments , which are agreed at the time of the issue, which can be as under : –

- At the time of Application ;

- At the time of Allotment ;

- At the time of First call, Second call or subsequent calls/final call.

Generally, the amount of application is received upfront by the company and there are no defaults. However, if a shareholder fails to pay the amount due on allotment of shares, or any of the calls discussed above, within the specified time allowed for such payment, the company has the right to cancel the allotment of such shares i.e., the name of the shareholder is cancelled from the register of shareholders.

In such cases, the amount already received by the company at the time of application, allotment or earlier call, is not refunded/returned to the shareholders. This act of the company is known as forfeiture of shares .

Permission for forfeiture should be given in Articles of Association

Shares can be forfeited only if the Articles of Association of the company permits the company to forfeit the shares.

Before the company can forfeit the shares, the defaulting shareholders has to be given a minimum of 14 days’ notice in order to pay the unpaid amount along with the interest thereon.

Accounting Entry- Forfeiture of Shares

1. Forfeiture of Shares, Issued at par : –

- To pass the Entry, first point is to identify the entries already made in the books of accounts. For example, if the shares were forfeited due to the non payment of first and final call, the amounts which were received /called, would have already been credited to the share capital account, as a credit balance. However, amounts which were due but which was not received, would be lying in the Calls in Arrears Account, as a Debit balance.

- In order to, reverse the existing balances, the following entries are passed : –

- ‘Share Capital A/c’ is debited by the amount which has been called till date .

- “Calls in Arrear A/c’ is credited , in order to cancel the debit balance of Calls in Arrear A/c which represents the amount due from the defaulting shareholder.

REFER QUESTION 1 TO 11 BELOW FOR VARIOUS SITUATIONS WHERE SHARES ISSUED AT PAR CAN BE FORFEITED

2. Forfeiture of Shares, issued at premium : –

In such a case, the forfeiture can take place, either before receipt of premium or after receipt of premium. The accounting entries that would be passed shall be as under : –

(i) Forfeiture of shares before receipt of share premium: When the shares which are forfeited are the one’s on which share premium has become due but not received , ‘Securities Premium A/c’ must be debited. The entry in this case will be:

Share Capital A/c Dr.

Securities Premium Reserve A/c Dr.

To Calls in Arrears A/c

To Share Forfeiture A/c

(ii) Forfeiture of shares after receipt of share premium: When the shares which are forfeited are the one’s on which shares premium is fully collected, share premium cannot be cancelled , even if that share is forfeited later on. Therefore, ‘Securities Premium A/c’ will not be debited in the entry for forfeiture.

REFER QUESTION 12 TO 14 BELOW FOR VARIOUS SITUATIONS WHERE SHARES ISSUED AT PREMIUM CAN BE FORFEITED

Journal Entry-Forfeiture of shares issued at par

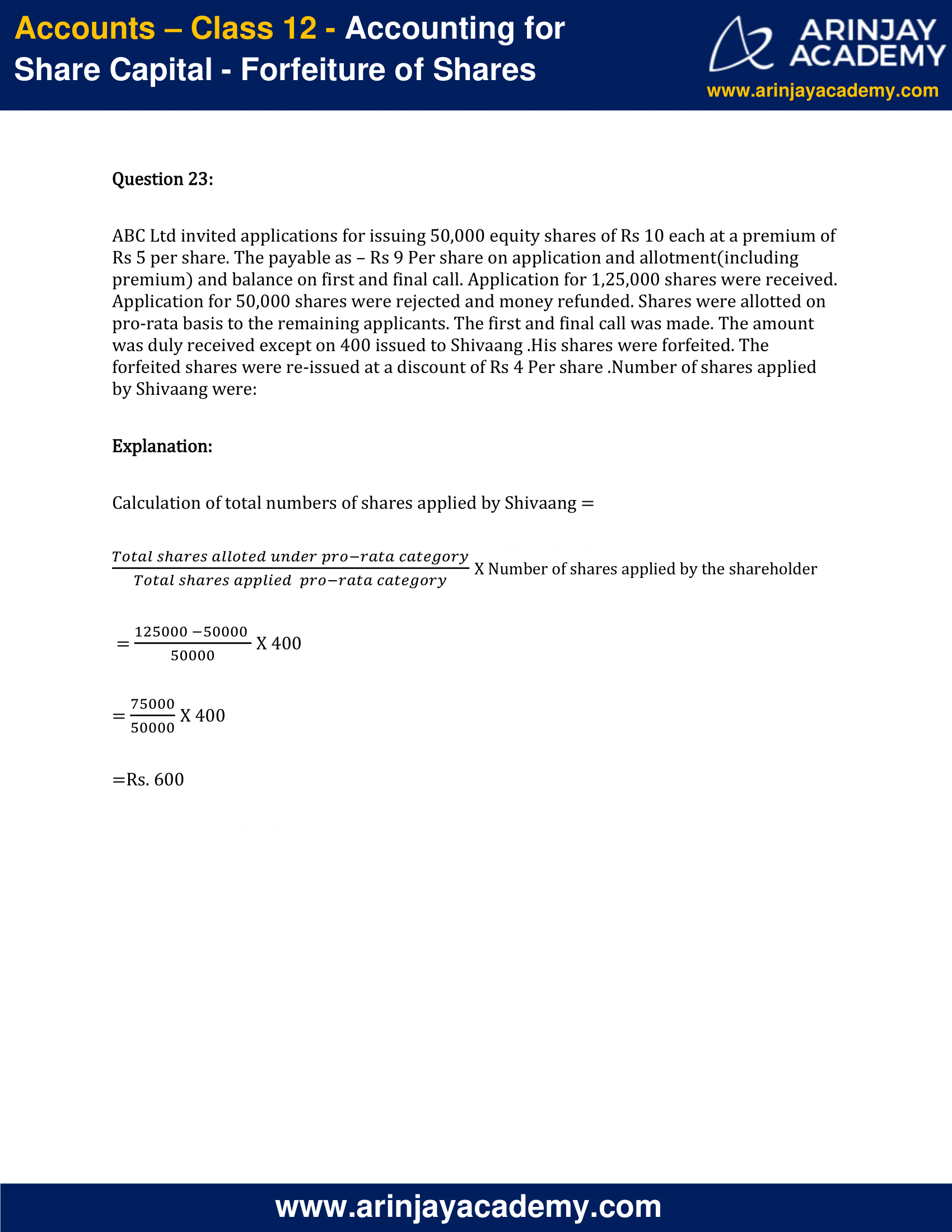

Question 1:

Cipla Ltd. issued 25,000 shares of Rs 30 each at par. Amount payable on the application Rs 10 per share , on allotment Rs 5 per share , on first call Rs 8 per share and on second call Rs 7 Per share. H was allotted 5,000 shares . If H failed to pay allotment money and his shares were forfeited after allotment. The necessary journal entry relating to the forfeiture of shares will be:

Explanation : –

Entry for forfeiture of share : –

Share capital A/c Dr 75,000 ( 5,000 x 15 ) Number of share forfeited x Called up value

To Share allotment A/c 25,000 ( 5,000 x 5 )

To Share forfeiture A/c 50,000 ( 5,000 x 10 )

Journal entry-Forfeiture of Shares (After allotment and first call)- Issue at par

Question 2:

Aircel Ltd issued 75,000 shares of Rs 20 each at par. Amount payable on the application Rs 4 per share , on allotment Rs 12 per share , on first call Rs 2 per share and on second call Rs 2 Per share. A was allotted 300 shares . If A failed to pay allotment money and on his subsequent failure to pay the first call, his shares were forfeited . The necessary journal entry relating to the forfeiture of shares will be:

Explanation:

Entry for forfeiture of shares :

Share capital A/c Dr 5,400 ( 300 x 18 ) Number of share forfeited x Called up value

To Share allotment A/c 3,600 ( 300 x 12 ) Amount not paid on allotment

To Share first call A/c 600 ( 300 x 2 ) Amount not paid on first call

To Share forfeiture A/c 1,200 ( 300 x 4 ) Amount received on shares forfeited

Determination of amount credited to forfeiture account (Forfeiture of shares after allotment and first call) – Shares issued at par

Question 3:

Best Ltd issued 70,000 shares of Rs 10 each at par. Amount payable on the application Rs 6 per share , on allotment Rs 2 per share , on first call Rs 1 per share and on second call Rs 1 Per share. H was allotted 3,500 shares . If H failed to pay allotment money and on his subsequent failure to pay the first call, his shares were forfeited . What will be the amount credited to the forfeiture account.

Explanation:

Amount credited to the forfeiture account:

Number of share forfeited x Amount paid

3,500 x 6

Rs. 21,000

Determination of amount credited to first call account (Forfeiture of shares after allotment and first call) – Shares issue at par

Question 4:

Best Ltd issued 70,000 shares of Rs 10 each at par. Amount payable on the application Rs 6 per share , on allotment Rs 2 per share , on first call Rs 1 per share and on second call Rs 1 Per share. H was allotted 3,500 shares . If H failed to pay allotment money and on his subsequent failure to pay the first call, his shares were forfeited . What will be the amount credited to the first call account.

Explanation:

Amount credited to the first call account:

Number of share forfeited x Amount of first call

3,500 x 1

Rs. 3,500

Forfeiture of shares (after first and final call)- Shares Issued at par

Question 6:

Asad Ltd issued 10,000 shares of Rs 10 each at par. Amount payable on the application Rs 2 per share , on allotment Rs 3 per share , on first call Rs 3 per share and on final call Rs 2 Per share. Z was allotted 80 shares. If Z failed to pay first call and on his subsequent failure to pay the final call, his shares were forfeited after the final call. The necessary journal entry relating to the forfeiture of shares in the following case will be:

Explanation:

Entry for forfeiture of shares :

Share capital A/c Dr 800 ( 80 x 10 ) Number of share forfeited x Called up value

To Share first call A/c 240 ( 80 x 3 ) Amount not paid on first call

To Share final call A/c 160 ( 80 x 2 ) Amount not paid on final call

To Share forfeiture A/c 400 ( 80 x 5 ) Amount received on shares forfeited ( 2 + 3 )

Determination of amount credited to forfeiture account (Forfeiture of shares after first and final call) – Shares issue at Par

Question 7:

A Ltd issued 10,000 shares of Rs 10 each at par. Amount payable on the application Rs 2 per share , on allotment Rs 3 per share , on first call Rs 3 per share and on final call Rs 2 Per share. Z was allotted 80 shares. If Z failed to pay first call and on his subsequent failure to pay the final call, his shares were forfeited after the final call. What will be the amount credited to the forfeiture account.

Explanation:

Amount credited to the forfeiture account:

Number of shares forfeited x Amount paid Application money + Allotment money

80 x 5 ( 2 + 3 )

Rs. 400

Determination of amount credited to first call account (Forfeiture of shares after first and final call) – Shares issued at par

Question 8:

A Ltd issued 10,000 shares of Rs 10 each at par. Amount payable on the application Rs 2 per share , on allotment Rs 3 per share , on first call Rs 3 per share and on final call Rs 2 Per share. Z was allotted 80 shares. If Z failed to pay first call and on his subsequent failure to pay the final call, his shares were forfeited after the final call. What will be the amount credited to the first call account.

Explanation:

Amount credited to the first call account:

Number of share forfeited x Amount of first call

80 x 3

240

Determination of amount credited to final call account (Forfeiture of shares after first and final call) – Shares issued at par

Question 9:

A Ltd issued 10,000 shares of Rs 10 each at par. Amount payable on the application Rs 2 per share , on allotment Rs 3 per share , on first call Rs 3 per share and on final call Rs 2 Per share. Z was allotted 80 shares. If Z failed to pay first call and on his subsequent failure to pay the final call, his shares were forfeited after the final call. What will be the amount credited to the final call account.

Explanation:

Amount credited to the final call account:

Number of share forfeited x Amount of final call

80 x 2

Rs. 160

Determination of amount credited to forfeiture account- Shares issued at par

Question 10:

Cipla Ltd. issued 25,000 shares of Rs 30 each at par. Amount payable on the application Rs 10 per share , on allotment Rs 5 per share , on first call Rs 8 per share and on second call Rs 7 Per share. H was allotted 5,000 shares . If H failed to pay allotment money and his shares were forfeited after allotment. What will be the amount credited to the forfeiture account.

Explanation:

Amount credited to the forfeiture account:

Number of share forfeited x Amount paid

5,000 x 10

Rs. 50,000

(**Amount paid is only application money)

Calculation of amount received on forfeiture of shares

Question 11:

AB Ltd issued 24,000 equity shares of Rs 25 each at par payable on the application Rs 6 per share , on allotment Rs 10 per share , on first call Rs 4 per share and on second call Rs 5 Per share. Shyam was alloted 140 shares .The amount transferred to share forfeiture account will be: if Shyam failed to pay second call money and his shares were forfeited after first call.

Explanation:

Amount transfer to share forfeiture account = Amount received on forfeiture of shares

Total money received on Shyam s share = Number of shares x (Application money + Allotment money + First call money)

= 140 x ( 6 + 10 + 4 )

= 140 x 20

=Rs. 2,800

Entry for Forfeiture of shares – which were originally issued at a premium( and security premium has been received)

Question 12:

Arun Ltd issued 24,000 equity shares of Rs 25 each at a premium of Rs 2 per share , Payable as Rs 10 per share on application , on allotment Rs 12 (including premium) and Rs 5 Per share on first and final call. Amit was alloted 450 shares failed to pay the first and final call and his shares were forfeited. The entry to record shares forfeiture will be:

Explanation:

Amount transferred to share forfeiture account = Amount received on shares forfeited

Total money received on Amit s share = Number of shares x (Application money + Allotment money – Excluding premium received)

= 450 x ( 10 + 10 )

= 450 x 20

= 9,000

( Number of shares forfeited x Called up value on shares

Share capital A/c Dr 11,250 ( 450 x 25 )

To Share first and final call A/c 2,250 ( 450 x 5 )

To Share forfeiture A/c 9,000

Or, we can use call in arrear account also to pass the entry:

Share capital A/c Dr 11,250

To Calls in arrear A/c 2,250

To Share forfeiture A/c 9,000

Entry for forfeiture of shares – which were originally issued at a premium( And security premium has not been received)

Question 13:

AB Ltd issued issued 42,000 shares of Rs 25 each at a premium of Rs 5 per share , Payable as Rs 10 per share on application , on allotment Rs 15 (including premium)Rs 5 Per share on first and final call. Vijay was allotted 300 shares failed to pay the allotment and final call money and his shares were forfeited. The entry to record forfeiture of shares will be:

Explanation:

Amount transferred to share forfeiture account = Amount received on forfeiture of shares

Total money received on Vijay s share = Number of shares x (Application money )

= 300 x 10

= 300 x 10

= 3,000

( Number of shares forfeited x Called up value on shares

Share capital A/c Dr 7,500 ( 300 x 25 )

Security premium reserve A/c Dr 1,500 ( 300 x 5 )

To Share allotment A/c 4500 ( 300 x 15 )

To Share first and final call A/c 1,500 ( 300 x 5 )

To Share forfeiture A/c 3,000

Or, we can use call in arrear account also to pass the entry:

Share capital A/c Dr 7,500

Security premium reserve A/c 1,500

To Calls in arrear A/c 6000 ( 4,500 + 1,500 )

To Share forfeiture A/c 3,000

Calculation of amount forfeited on shares- which were originally issued at a premium(And security premium has been received)

Question 14:

Arun Ltd issued 24,000 equity shares of Rs 25 each at a premium of Rs 2 per share , Payable as Rs 10 per share on application , on allotment Rs 12 (including premium) and Rs 5 Per share on first and final call. was alloted 450 shares failed to pay the first and final call and his shares were forfeited. Amount transfer to share forfeiture account will be :

Explanation:

Amount transferred to share forfeiture account = Amount received on forfeiture of shares

Total money received on Amit s share = Number of shares x (Application money + Allotment money – Excluding premium received)

= 450 x ( 10 + 10 )

= 450 x 20

=Rs. 9,000

Re-issue of forfeited shares

Question 15:

Arjun Ltd which was allotted 500 equity shares of Rs 5 each by a company, failed to pay the final call of Rs 2 per share .These shares were forfeited and re-issued to X Ltd at Rs 5 each. Entry for forfeiture and re-issue in the books will be:

Explanation:

Entry for forfeiture of shares:

Equity Share capital A/c Dr 2,500 ( 500 x 5 )

To Equity share final call A/c 1,000 ( 500 x 2 )

To Equity Share forfeiture A/c 1,500 ( 500 x 3 )

Entry for Re-issue of shares

Bank A/c Dr 2,500 ( 500 x 5 )

To Equity Share capital A/c 2,500

Calculation of amount transferred to capital reserve account

Question 16:

Abhishek who was alloted 600 equity shares of Rs 60 each by a company, failed to pay the final call of Rs 20 per share .These shares were forfeited and re-issued to Sapna at Rs 60 .Amount transferred to capital reserve account will be:

Explanation:

Amount forfeited on Abhishek s share = 600 x 40

=Rs. 24,000 Amount transferred to capital reserve

When forfeited shares are re-issued at par or premium, the whole of the amount forfeited on such shares is a capital profit and is transferred to capital reserve account.

When all forfeited shares are not Re-issued (Calculation of amount transferred to capital reserve)

Question 17:

Ajay who was allotted 240 equity shares of Rs 20 each by a company, failed to pay the final call of Rs 6 per share .These shares were forfeited and out of these 200 shares were re-issued to Sapna at Rs 20 .Amount transferred to capital reserve account will be:

Explanation:

Total amount forfeited on Ajay s shares = 240 x 14

=Rs,. 3,360

Number of shares re-issued = 200

Amount transferred to capital reserve = Amount forfeited on shares re-issued – Discount on issue of shares if any

Amount forfeited on 200 shares = 200 x 14 – 0

=Rs. 2,800

Entry for capital reserve when all forfeited shares are not Re-issued

Question 18:

Akash who was allotted 1,000 Preference shares of Rs 30 each by a company, failed to pay the final call of Rs 8 per share .These shares were forfeited and out of these 500 shares were re-issued to Tarun at Rs 30 .Journal entry for transferring amount to capital reserve will be:

Explanation:

Total amount forfeited on Akash s shares = 1,000 x 22

=Rs. 22,000

Number of shares re-issued = 500

Amount transferred to capital reserve = Amount forfeited on shares re-issued – Discount on issue of shares if any

Amount forfeited on 500 shares = 500 x 22 – 0

=Rs. 11,000

Forfeited shares A/c Dr 11,000

To Capital Reserve A/c 11,000

Calculation of amount transferred to capital reserve When partly shares are re-issued from forfeited shares on discount

Question 19:

Amit who was allotted 400 equity shares of Rs 30 each by a company, failed to pay the final call of Rs 5 per share .These shares were forfeited and out of these 200 shares were re-issued to Deepika at Rs 15 per shares fully paid up. Amount transferred to capital reserve account will be:

Explanation:

Total amount forfeited on Amit s shares = 400 x 25

=Rs. 10,000

Number of shares re-issued = 200

Amount transferred to capital reserve = Amount forfeited on shares re-issued – Discount on issue of shares if any

Amount forfeited on 200 shares = ( 200 x 25 ) – ( 200 x 15 )

= 5,000 – 3,000

= 2,000

Journal Entry When partly shares are re-issued from forfeited shares on discount

Question 20:

Akash who was allotted 600 equity shares of Rs 50 each by a company, failed to pay the final call of Rs 8 per share .These shares were forfeited and out of these 300 shares were re-issued to Rahul at Rs 35 per shares fully paid up. Journal entry for shares re-issued will be:

Explanation:

Total amount forfeited on Akash s shares = 600 x 42

=Rs. 25,200

Number of shares re-issued = 300

Amount transferred to capital reserve = Amount forfeited on shares re-issued – Discount on issue of shares if any

Amount forfeited on 300 shares = ( 300 x 42 ) – ( 300 x 15 )

= 12,600 – 4,500

= 8,100

Entry for re-issue of shares:

Bank A/c Dr 10,500 ( 300 x 35 )

Forfeited share A/c Dr 45,00 ( 300 x 15 )

To share capital A/c 15,000 ( 300 x 50 )

Journal Entry When partly shares are re-issued from forfeited shares on premium

Question 21:

On 1st April 2013 A company issued shares and a shareholder Manish who was allotted 1,500 shares of Rs 25 each by the company, failed to pay the final call of Rs 5 per share .These shares were forfeited and out of these 1,200 shares were re-issued to Rohit at Rs 30 per shares fully paid up. Journal entry for shares re-issued and capital reserve will be:

Explanation:

Total amount forfeited on Manish s shares = 1,500 x 20

=Rs. 30,000

Number of shares re-issued = 1,200

Amount transferred to capital reserve = Amount forfeited on shares re-issued – Discount on issue of shares if any

Amount on forfeiture of shares = ( 1,200 x 20 ) – 0

= 24,000 – 0

=Rs. 24,000. This whole amount will be transferred to capital reserve account.

When forfeited shares are re-issued at par or premium, the whole of the amount forfeited on such shares is a capital profit and is transferred to capital reserve account.

Entry for re-issue of shares:

Bank A/c Dr 36,000 ( 1,200 x 30 )

To share capital A/c 30,000 ( 1,200 x 25 )

To Security premium reserve A/c 6,000 ( 1,200 x 5 )

Entry for capital reserve:

Share forfeiture A/c Dr 24,000

To Capital Reserve A/c 24,000

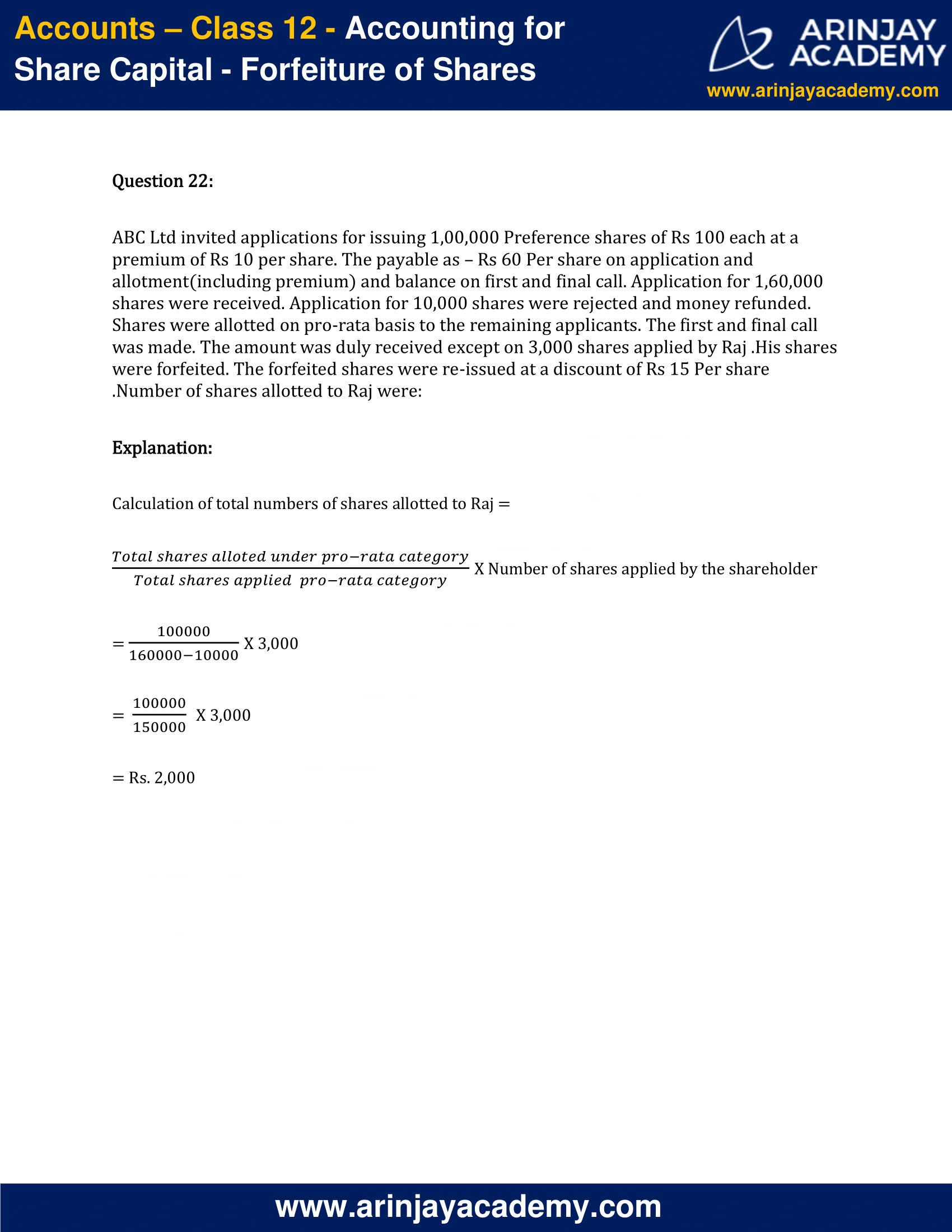

Determination of number of share allotted to a person in case of pro-Rata

Determination of number of share applied by a person in case of Pro-Rata