Redemption of debentures – Methods and Meaning

The methods of redemption of debentures and , meaning of redemption of debentures are explained below.

Redemption of Debentures Meaning

When the company which has issued Debentures and borrowed money from such issue, repays the owner of such Debentures, it is called the redemption of Debentures : –

(i) Redemption of Debentures in lump-sum (at one go): –

Redemption of Debentures in lump-sum, means that the Debentures are repaid to Debenture Holders in lump-sum (at once or in one go the entire amount is repaid) , after a specified period of time, as per the terms of the Debentures. The company , which has issued the Debentures, pays the entire amount payable to the Debenture holders (as per the term of the issue of such Dedebentures) in lump sum .

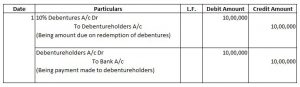

Redemption of Debentures Journal Entries – Debentures issued at par and redeemable at Par

Example 1: ABC Ltd. issued 10,000 10% debentures of Rs. 100 each at par. The debentures are redeemable at the end of 5 years out of capital. Pass the journal entry for such redemption.

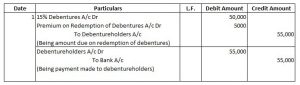

Redemption of Debentures Journal Entries – Debentures issued at par and redeemable at Premium

Example 2: Ravish Ltd. issued 5,000 15% debentures of Rs. 10 each at par. The debentures are redeemable at 10% premium the end of 3 years out of capital. The journal entry for such redemption will be:

(ii) Redemption of Debentures by payment in installments:

In this method of redemption of Debentures, the amount is repaid to debenture holders in installments on specified date (which are agreed in advance at the time of issue of Debentures), during the life of the debentures. In order to calculate the amount of installment, the total amount payable to the debenture holders is divided by the total number of years.

Redemption of Debentures by payment in Installments – Journal Entries

1 If redeemed out of profits:

a) Statement of Profit & Loss A/c Dr.

To Debenture Redemption Reserve A/c

(Being DRR transferred to P&L A/c)

b) Debentures A/c Dr.

To Debenture holders A/c

(Being amount payable to debenture holders)

c) Debentureholders A/c Dr.

To Bank A/c

(Being amount paid to debenture holders)

2 If redeemed out of capital:

a) Debentures A/c Dr.

To Debentureholders A/c

(Being amount payable to debenture holders)

b) Debentureholders A/c Dr.

To Bank A/c

(Being amount paid to debenture holders)

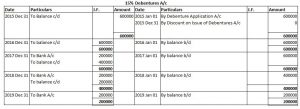

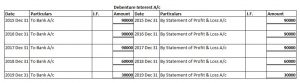

Example 3: XYZ Ltd. issued 6,000, 15% debentures of Rs. 100 each at par on January 1, 2015. The due date for payment of interest on these debentures is December 31 every year. The debentures are redeemable at par in three equal installments, beginning from the end of 3rd year. Prepare 15% Debentures Account & Debenture Interest Account.

(iii) Redemption by way of Purchase in open market:

Where a company purchases its own debentures from the market , and cancels the Debentures so purchased, such an act of purchasing and cancellation of own debentures by the company is known as redemption of debentures by way of purchase in the open market.

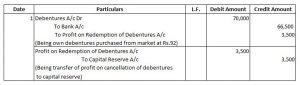

Example 4: Kayaan Ltd. purchased its own debentures of Rs 100 each of the face value of Rs. 70,000 from the open market for cancellation at Rs 95. Record necessary journal entries.

(iv) Conversion of Debentures into new shares or new debentures:

In this method, debentures are redeemed by the company by converting them into new shares, or issuance of Debentures of other class. Such a conversion can be done as per the terms of issue of the original debentures. The debenture holders who holds convertible Debentures only get this option to redeem their debenture by way of conversion into shares or debentures.

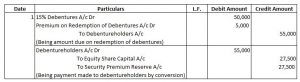

Example 5: AB&D Ltd redeemed 5,000 15% Debentures of Rs 10 each at a premium of 10 % on 31st March 2018. Debenture holders were given equity shares of Rs 10 each at premium of Rs 10 per share. Journal entries in the books of Anil Ltd will be:

Amount of Debenture due for payment = Total number of Debentures X Value of per Debenture

= 5,000 X 10

= 50,000

Amount of premium on redemption of per Debenture = 10 X 10/100 = 1

Total amount of premium payable = No of Debenture to be redeemed X Amount of premium on redemption of per Debenture

= 5,000 X 1

= 5,000

Total amount due to Debenture holders = 50,000 + 5,000

= 55,000

Issue price of share = 10 + 10

Issue price of share = 20

= (50,000+5,000)/20

= 2,750

Entry for amount due to Debentureholders on conversion of 5,000 15 % Debentures will be:

Learn More..

4 thoughts on “Methods of Redemption of Debentures | Accounts Class 12”

Really very helpful and Luv the way it is explain ❤❤❤❤❤

Nice explanation of redemptions methods of debentures.???

Nice explanation of redemptions methods of debentures.???

helpful explanation of methods of redemption of debenture ?????