Financial Statement Analysis MCQs with Answer are covered in this Article. Financial Statement Analysis MCQs Test contains 13 questions. Answers to MCQ on Financial Statement Analysis Class 12 Accountancy are available at the end of the last question. These MCQ have been made for Class 12 students to help check the concept you have learnt from detailed classroom sessions and application of your knowledge. For more MCQ’s, subscribe to our email list.

Financial Statement Analysis MCQs – Question 1: –

Following is the information available from the records of BEE Ltd

| Particulars | 2008 | 2007 |

| Revenue from Operations | 1800000 | 1500000 |

| Expenses | 1080000 | 970000 |

| Other Income | 250000 | 165000 |

Absolute Change and Percentage Change in Revenue from Operations is:

a) 1800000 and 20 %

b) 300000 and 20 %

c) 1500000 and 20 %

d) None of the above

Financial Statement Analysis MCQs – Question 2: –

Following is the information available from the records of O Ltd

| Particulars | 2008 | 2007 |

| Revenue from Operations | 3000000 | 1800000 |

| Expenses | 2100000 | 1400000 |

| Other Income | 250000 | 200000 |

Absolute Change and Percentage Change in Expenses is:

a) 2100000 and 50 %

b) 1400000 and 50 %

c) 700000 and 50 %

d) None of the above

Financial Statement Analysis MCQs – Question 3: –

Following is the information available from the records of DEF Ltd

| Particulars | 2008 | 2007 |

| Revenue from Operations | 2000000 | 1500000 |

| Expenses | 1550000 | 1050000 |

| Other Income | 600000 | 400000 |

Absolute Change and Percentage Change in Other income is:

a) 200000 and 50 %

b) 600000 and 50 %

c) 400000 and 50 %

d) None of the above

MCQs on Financial Statement Analysis – Question 4: –

Following is the information available from the records of Two Ltd

| Particulars | 2008 | 2007 |

| Revenue from Operations | 1600000 | 1000000 |

| Expenses | 900000 | 600000 |

| Other Income | 270000 | 200000 |

Profit before tax is :

a) 2007 – 600000

2008 – 970000

b) 2007 – 1200000

2008 – 1870000

c) 2007 – 1000000

2008 – 1600000

d) None of the above

MCQs on Financial Statement Analysis – Question 5: –

Following is the information available from the records of MANY LTD

| Particulars | 2008 | 2007 |

| Revenue from Operations | 2500000 | 2000000 |

| Expenses | 2000000 | 1600000 |

| Other Income | 400000 | 320000 |

Rate of Tax is 40 %

Profit after tax is :

a) 2007 – 2320000

2008 – 2900000

b) 2007 – 432000

2008 – 540000

c) 2007 – 2000000

2008 – 2500000

d) None of the above

MCQs on Financial Statement Analysis – Question 6: –

Following is the information provided by B LTD

| Particulars | 2008 | 2007 |

| Revenue from Operations | 7000000 | 5000000 |

| Purchase of Stock | 3500000 | 2500000 |

| Other Expenses | 500000 | 250000 |

| Rate of Income Tax | 30% | 30% |

Purchase of Stock Percentage to Revenue from Operations is:

a) 2007 – 50

2008 – 50

b) 2007 – 40

2008 – 60

c) 2007 – 45

2008 – 65

d) None of the above

MCQs on Financial Statement Analysis – Question 7: –

Following is the information provided by B LTD

| Particulars | 2008 | 2007 |

| Revenue from Operations | 500000 | 400000 |

| Purchase of Stock | 350000 | 280000 |

| Other Expenses | 200000 | 100000 |

| Rate of Income Tax | 40% | 40% |

Other Expenses Percentage to Revenue from Operations is:

a) 2007 – 28

2008 – 46

b) 2007 – 30

2008 – 45

c) 2007 – 25

2008 – 40

d) None of the above

Financial Statement Analysis MCQs – Question 8: –

Following is the information provided by B LTD

| Particulars | 2008 | 2007 |

| Revenue from Operations | 750000 | 680000 |

| Purchase of Stock | 650000 | 500000 |

| Other Expenses | 85000 | 50000 |

| Rate of Income Tax | 30% | 30% |

Profit after Tax for year 2007 is

a) 10500

b) 130000

c) 91000

d) None of the above

Financial Statement Analysis MCQs – Question 9: –

Following is the information provided by B LTD

Absolute Change and Percentage Change in share capital is

a) Absolute Change – 1030000, Percentage Change – 28

b) Absolute Change – 1000000, Percentage Change – 25

c) Absolute Change – 980000, Percentage Change – 23

d) None of the above

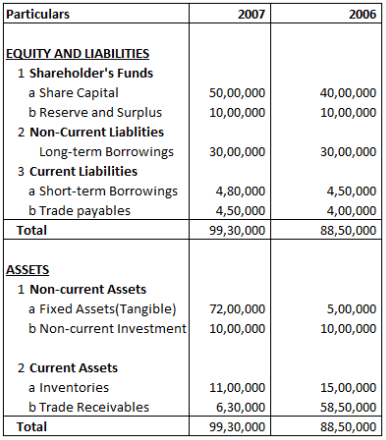

Financial Statement Analysis MCQs – Question 10: –

Following is the Balance sheet of BB Ltd

Absolute Change and Percentage Change in Reserve and Surplus is:

a) Absolute Change -170000, Percentage Change -17

b) Absolute Change -200000, Percentage Change -20

c) Absolute Change -220000, Percentage Change -22

d) None of the above

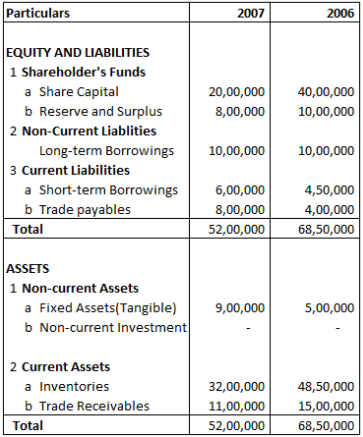

Financial Statement Analysis MCQs – Question 11: –

Following is the Balance sheet of C Ltd

Absolute Change and Percentage Change in Long-term Borrowings is:

a) Absolute Change 100000, Percentage Change 25

b) Absolute Change 70000, Percentage Change 23

c) Absolute Change 90000, Percentage Change 21

d) None of the above

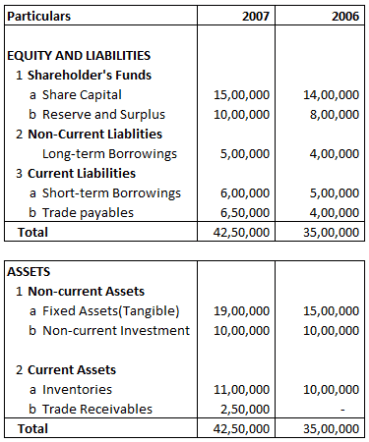

MCQs on Financial Statement Analysis – Question 12: –

Following is the Balance sheet of B Ltd

Absolute Change and Percentage Change in Fixed Assets(Tangible) is:

a) Absolute Change – 250000, Percentage Change – 47

b) Absolute Change – 220000, Percentage Change – 44

c) Absolute Change – 200000, Percentage Change – 42

d) None of the above

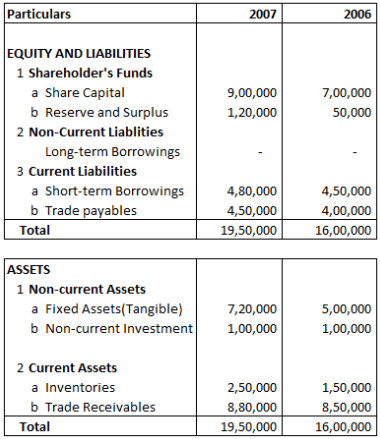

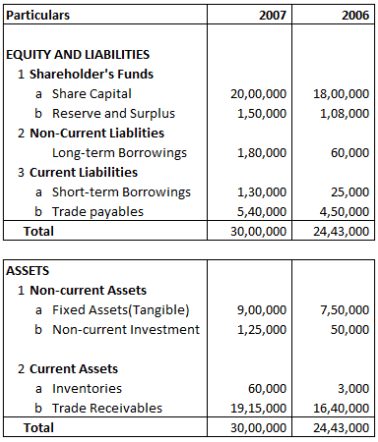

MCQs on Financial Statement Analysis – Question 13: –

Following is the balance sheet of B Ltd

Fixed Assets(Tangible) Percentage of Balance Sheet Total for 2007 will be:

a) 30

b) 26

c) 28

d) None of the above

Financial Statement Analysis MCQs Answers and Explanations

Financial Statement Analysis MCQs – Explanation 1: –

Comparative Statement of Profit and Loss

| Particulars | 2007 | 2008 | Absolute Change | Percentage Change % |

| A | B | C = (B-A) | D = C/A x 100 | |

| Revenue from Operations | 1500000 | 1800000 | 300000 | 20 |

Absolute Change = Current year balance – Previous year balance

Absolute Change = 1800000 – 1500000 = 300000

Percentage Change % = (Absolute Change/ Previous Year Balance) X 100

Percentage Change % = (300000/1500000) X 100

= 20 %

Correct Answer – b) 300000 and 20 %

Explanation 2: –

| Particulars | 2007 | 2008 | Absolute Change | Percentage Change % |

| A | B | C = (B-A) | D = C/A x 100 | |

| Expenses | 1400000 | 2100000 | 700000 | 50 |

Absolute Change = Current year balance – Previous year balance

Absolute Change = 2100000 – 1400000 = 700000

Percentage Change % = (Absolute change/Previous year balance) x 100

Percentage Change % = (700000/1400000) X 100

= 50 %

Correct Answer – c) 700000 and 50 %

Financial Statement Analysis MCQs – Explanation 3: –

Comparative Statement of Profit and Loss

| Particulars | 2007 | 2008 | Absolute Change | Percentage Change % |

| A | B | C = (B-A) | D = C/A x 100 | |

| Expenses | 400000 | 600000 | 200000 | 50 |

Absolute Change = Current year balance – Previous year balance

Absolute Change = 600000 – 400000 = 200000

Percentage Change % = (Absolute change/Previous year balance) x 100

Percentage Change % = (200000/400000) X 100

= 50 %

Correct Answer – a) 200000 and 50 %

Explanation 4: –

Comparative Statement of Profit and Loss

| Particulars | 2007 | 2008 | Absolute Change |

| A | B | C = (B-A) | |

| Revenue for Operations | 1000000 | 1600000 | 600000 |

| Other Income | 200000 | 270000 | 70000 |

| Total Revenue | 1200000 | 1870000 | 670000 |

| Expenses | 600000 | 900000 | 300000 |

| Profit before Tax | 600000 | 970000 | 370000 |

Absolute Change = Current year balance – Previous year balance

Revenue from Operations = 1600000 – 1000000 = 600000

Other Income = 270000 – 200000 = 70000

Expenses = 900000 – 600000 = 300000

Percentage Change = (Absolute change/Previous year balance) x 100

Revenue for Operations = (600000/1000000) X 100 = 60

Other Income = (70000/200000) X 100 = 35

Expenses = (300000/600000) X 100 = 50

Correct Answer – a) 2007 – 600000, 2008 – 970000

Financial Statement Analysis MCQs – Explanation 5: –

Comparative Statement of Profit and Loss

| Particulars | 2007 | 2008 | Absolute Change |

| A | B | C = (B-A) | |

| Revenue for Operations | 2000000 | 2500000 | 500000 |

| Other Income | 320000 | 400000 | 80000 |

| Total Revenue | 2320000 | 2900000 | 580000 |

| Expenses | 1600000 | 2000000 | 400000 |

| Profit before Tax | 720000 | 900000 | 180000 |

| Less: Tax 40% | 288000 | 360000 | 72000 |

| Profit after Tax | 432000 | 540000 | 108000 |

Absolute Change = Current year balance – Previous year balance

Revenue from Operations = 2500000 – 2000000 = 500000

Other Income = 400000 – 320000 = 80000

Expenses = 2000000 – 1600000 = 400000

Percentage Change = (Absolute change/Previous year balance) x 100

Revenue for Operations = (500000/2000000) X 100 = 25

Other Income = (80000/320000) X 100 = 25

Expenses = (400000/1600000) X 100 = 25

Correct Answer –

b) 2007 – 432000

2008 – 540000

Explanation 6: –

Percentage of Revenue from Operations (Net Sales) = (Amount of particular expense in that year/Total Revenue in that year) x 100

Purchase of Stock

2007 = (2500000/5000000) x 100 = 50

2008 = (3500000/7000000) x 100 = 50

Correct Answer – a) 2007 – 50, 2008 – 50

Explanation 7: –

Percentage of Revenue from Operations(Net Sales) = (Amount of particular expense in that year/Total revenue in the year) x 100

Other Expenses

2007 = (100000/400000) x 100 = 25

2008 = (200000/500000) x 100 = 40

Correct Answer – c) 2007 – 25, 2008 – 40

Financial Statement Analysis MCQs – Explanation 8: –

| Particulars | 2007 | 2008 |

| Revenue for Operations | 680000 | 750000 |

| Expenses | ||

| Purchase of Stock | 500000 | 650000 |

| Other Expenses | 50000 | 85000 |

| Total Expenses | 550000 | 735000 |

| Profit before Tax | 130000 | 15000 |

| Less: Income Tax | 39000 | 4500 |

| Profit after Tax | 91000 | 10500 |

Correct Answer – c) 91000

Explanation 9: –

| 2006 | 2007 | Absolute Change | Percentage Change | |

| Share Capital | 4000000 | 5000000 | 1000000 | 25 |

Absolute Change = Current year’s figure – Previous year’s figure

= 5000000 – 4000000

= 1000000

Percentage Change = (Absolute Change/Amount of Previous Year) x 100

= (1000000/4000000) x 100

= 25 %

Correct Answer – b) Absolute Change – 1000000, Percentage Change – 25

Explanation 10: –

| 2006 | 2007 | Absolute Change | Percentage Change | |

| Reserve and Surplus | 1000000 | 800000 | -200000 | -20 |

Absolute Change = Current year’s figure – Previous year’s figure

= 800000 – 1000000

= -200000

Percentage Change = (Absolute Change/Amount of Previous Year) x 100

= (−200000/1000000) x 100

= -20

Correct Answer – b) Absolute Change -200000, Percentage Change -20

Explanation 11: –

Comparative Balance Sheet

| 2006 | 2007 | Absolute Change | Percentage Change | |

| Long Term Borrowings | 400000 | 500000 | 100000 | 25 |

Absolute Change = Current year’s figure – Previous year’s figure

= 500000 – 400000

= 100000

Percentage Change = (Absolute Change/Amount of previous year) x 100

= (100000/400000) x 100

= 25%

Correct Answer – a) Absolute Change 100000, Percentage Change 25

Financial Statement Analysis MCQs – Explanation 12: –

Comparative Balance Sheet

| 2006 | 2007 | Absolute Change | Percentage Change | |

| Fixed Assets (Tangible) | 500000 | 720000 | 220000 | 44 |

Absolute Change = Current year’s figure – Previous year’s figure

= 720000 – 500000

= 220000

Percentage Change = (Absolute Change/Amount of previous year) x 100

= (220000/500000) x 100

= 44

Correct Answer – b) Absolute Change – 220000, Percentage Change – 44

Financial Statement Analysis MCQs – Explanation 13: –

Extract of Common size Balance Sheet

| Particulars | 2007 | Percentage of Balance sheet Total |

| Fixed Assets (Tangible) | 900000 | 30 |

Fixed Assets(Tangible) Percentage of Balance Sheet Total 2007

= (Balance of Fixed Assets(Tangible) in the year/Total of Balance Sheet in the year) x 100

= (900000/3000000) x 100

= 30

Correct Answer – a) 30