Dissolution of Partnership Accounting – Modes of dissolution without intervention of court:

- On the Basis of Mutual Agreement : A partnership firm is being setup on the basis of mutual agreement between partners. In the similar way, a partnership firm can be dissolved on the basis of mutual agreement between partners.

- On the Happening of an Event : A partnership firm can be dissolved on the basis of happening of any of the below mentioned events: a) Due to the fulfillment of the objective of business b) Due to insolvency of partners c) On the expiry of period for which the firm was formed.

- Compulsory Dissolution : A firm is compulsorily dissolved either if the business is unlawful or any or all of the partners have become insolvent.

- By Notice : When the duration of the partnership firm is not fixed and it is at will then any partner can dissolve the business by giving a notice.

Dissolution Without Intervention of Court – Asset credited to realisation account when realisation %given

Question 1 : –

If on the dissolution of the firm A Ltd. Sundry assets transferred to realisation account is Rs. 50000 .Asset realised 50 % of their book value. What amount should be credited to realisation account ?

Explanation : –

Realised value of asset = 50000 X 50% = 25000

Cash/Bank A/c Dr 25000

To Realisation A/c 25000

Dissolution Without Intervention of Court – Calculation of amount realised from sale of asset

Question 2 : –

The amount of sundry assets trasferred to realisation account was Rs. 100000 . 70 % of them have been sold at a profit of Rs. 10000 . 20 % of the remaining were sold at a discount of 15 % .The amount realised from the sale is:

Explanation : –

Calculation of amount realised from sale

1. Sale ( 50% of 60000 ) = 30000 Rs.

Add: Profit on sale = 4000 Rs.

A = 34000 Rs.

Remaining goods at book value = 60000 – 30000 = 30000 Rs.

2. Sale ( 40% of 30000 ) = 12000 Rs.

Less: Discount on sale 25% of 12000 = 3000 Rs.

B = 9000 Rs.

Total amount realised from assets A + B

= 34000 9000

= 43000 Rs.

Dissolution Without Intervention of Court – Calculation of realised value of assets

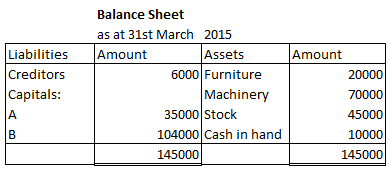

Question 3 : –

A and B were partners.They decided to dissolve their firm on 31st March 2015 .Balance sheet of the firm on dissolution given below. A was appointed to realise the assets. A was to receive 6% commission on the sale of assets(except cash) and was to bear all expenses of realisation . A realised the assets as: Furniture 50% , Machinery 40% , Stock 80% of the book value.The amount realised from assets is:

Explanation : –

Total value of assets realised :

Furniture = 20000 X 50% = 10000

Machinery = 70000 X 40% = 28000

Stock = 45000 X 80% = 36000

= 74000

Dissolution Without Intervention of Court – Calculation of value of asset taken over by a partner

Question 4 : –

The amount of sundry assets trasferred to realisation account was Rs. 100000 . 30 % of them have been sold at a profit of Rs. 10000 . 10 % of the remaining assets were sold at a discount of 15 % and remaining were taken over by D (a partner) at 20 % above book value .At what value were the assets taken over by D ?

Explanation : –

Calculation of value of asset taken over by D

Total value of assets transferred to realisation account = 100000 Rs.

Less: Sale 30% of 100000 = 30000 Rs.

=70000 Rs.

Less: Sale 10% of 70000 = 7000 Rs.

Book value of remaining goods = 63000 Rs.

Add: 20% of 63000 = 12600 Rs.

Goods taken over by D at Rs. = 75600 Rs.