Dissolution of Partnership Accounting – Dissolution by the Order of Court

The partner may give an application to the court for dissolution of firm. The court, on receipt of application may order the dissolution of the partnership firm under the following circumstances:

- On satisfaction of the court that the decision of dissolution is equitable and just

- When a partner has become unsound mind

- When a partner, other than the partner filing the suit is guilty of misconduct or he willfully commits breach of contract

- When a partner, other than the partner filing the suit has become permanently incapable of performing the duties as a partner

- When the court is satisfied that the firm cannot be carried out except on a loss

Dissolution by the Order of Court – Journal Entry for asset realised

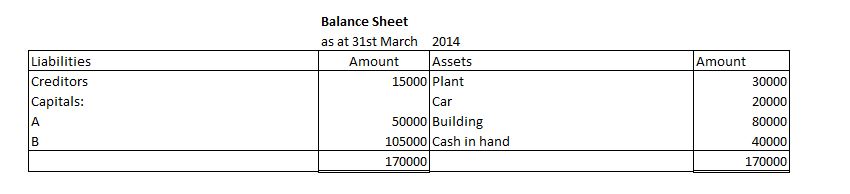

Question 1 : –

A and B were partners.They decided to dissolve their firm on 31st March 2014 .Balance sheet of the firm given below. A was appointed to realise the assets. A was to receive 12 % commission on the sale of assets(except cash) and was to bear all expenses of realisation . A realised the assets as: Plant 55 % , Car 45 % , Building 80 % of the book value. The journal entry for asset realised will be:

Explanation : –

Total value of assets realised :

Plant = 30000 X 55% = 16500

Car = 20000 X 45% = 9000

Building = 80000 X 80% = 64000

= 89500

Cash/Bank A/c Dr 89500

To Realisation A/c 89500

Dissolution by the Order of Court – Journal Entry for the payment of unrecorded liabilities

Question 2 : –

On dissolution of A Ltd .It was found that an unrecorded Trade Payable of Rs. 50000 settled at Rs. 32000 . What will be the journal entry of the transaction?

Explanation : –

Unrecorded liabitlities are those liabilties which are not appeared in the balance sheet of the firm but remain payable . When these liabilities are paid off realisation account is debited and cash/bank account is credited.

Dissolution by the Order of Court – Journal Entry for value of goods taken over by partner

Question 3 : –

The amount of sundry assets transferred to realisation account was Rs. 100000 . 45 % of them have been sold at a profit of Rs. 10000 . 10 % of the remaining were sold at a discount of 20 % and remaining were taken over by B (a partner) at 15 % above book value .what will be the journal entry of assets taken over by B ?

Explanation : –

Calculation of value of asset taken over by X :

Total value of assets transferred to Realisation Account = 60000 Rs.

Less: Sale ( 50% of 60000 ) = – 30000 Rs.

= 30000 Rs.

Less: Sale 20% of 30000 = – 6000 Rs.

Book value of remaining goods = 24000 Rs.

Add: 10% of 24000 = + 2400 Rs.

Goods taken over by X at Rs. = 26400 Rs.

Journal Entry :

X s capital A/c Dr. 26400

To Realisation A/c 26400

Dissolution by the Order of Court – Partner discharge realisation expense & receive remuneration

Question 4 : –

On dissolution of A Ltd , A (a partner) paid realisation expenses of Rs. 20000 out of his private funds, who was to get remuneration of Rs. 10000 for completing the dissolution process and was responsible to bear all the realisation expenses. What will be the journal entry of the transaction?

Explanation : –

When a partner was responsible for all the dissolution process then he can only receive the remuneration decided by the firm. If the amount of realisation expenses paid by the partner is more than the remuneration decided then partner have to pay the excess from his personal funds.

Dissolution by the Order of Court – Treatment of Goodwill on Dissolution

Question 5 : –

A and B were partners in a firm which was dissolved.

No goodwill appeared in the books. What will be the journal entry if Goodwill realised Rs. 80000 ?

Explanation : –

On dissolution every asset and liability of the firm is transferred to realisation account and if any amount is realised for goodwill then bank / cash account is debited and the realisation account is credited.