Death of a Partner

In case of death of a partner, the amount payable to him is to be paid to his legal representatives. The partnership between the partner comes to an end in case of death of the partner. The profit sharing ratios between the partners’ changes. The books of accounts are maintained in the same way as in case of retirement of partner. All the adjustments are being made in the capital account of the deceased partner and then the balance of the capital account is transferred to his executor’s account.

The legal representative of the partner are entitled to claim the following amount in case of death of partner:

- The amount which is standing to the credit of his capital account.

- Deceased partner’s share of profit upto his death.

- His share of increase in the value of goodwill of the firm.

- Interest on capital

- Revaluation profits and losses

The below given amount will be debited from the deceased partner’s capital account:

- Drawings, if any

- Interest on drawings

- Losses on revaluation of assets and liabilities

- His share of undistributed losses

Profit in case of Death of a Partner

The deceased partner is eligible to his share of profit upto his date of death. Such profit will be ascertained by any of the following methods:

- On Time Basis: In this method, we consider the profit earned by the firm during last year and calculate the proportionate profit for the period served by the deceased partner.

- On Turnover Basis: In this method, we consider the profit and total sales earned during the last year. So, the profit of the current year is calculated on the basis of sales for last year and upto the death of the deceased partner.

Deceased Partner’s share in Goodwill – When Goodwill on Average Profits

Death of a Partner : Example 1

A , B and C are partners sharing profits and losses in the ratio of 1/6 : 2/6 : 3/6. Goodwill of the firm was valued on the basis of 2 year’s purchase of the average profits of the last 4 years.Profits for the last 4 years was Rs 10000 , 8000 , 12000 and 10000 C died. What is C s share of goodwill?

Explanation : –

Total profits of 4 years = 10000 + 8000 + 12000 + 10000

= 40000

= 40000/4 = 10000

Value of goodwill = Average profits of 4 years X Number of years purchase

= 10000 x 2

= 20000

C s share of goodwill = Value of goodwill x share of C in profits of the firm

= 20000 x 3/6

= 10000

Gaining ratio among remaining partners

Death of a Partner : Example 2

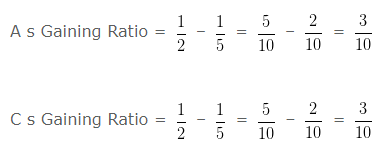

A , B and C are partners sharing profits and losses in the ratio of 1/5 : 3/5 : 1/5 B died.what will be the gaining ratio between A and C ?

Explanation : –

New Ratio between A and C after retirement of B = 1/2 : 1/2

Gaining Ratio = New Ratio – Old Ratio

Gaining Ratio = 3 : 3

New PSR when gaining share of continuing partners given

Death of a Partner : Example 3

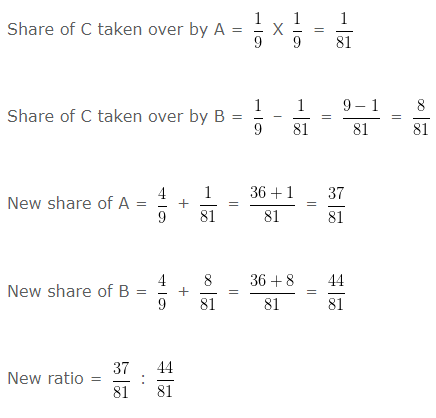

A , B and C are partners sharing profits and losses in the ratio of 4/9 : 4/9 : 1/9 C died and 1/9 of his share is taken over by A and remaining by B . Calculate the new profit sharing ratio between A and B .

Explanation : –

Old ratio between A B and C = 4 : 4 : 1

= 37 : 44

Gaining ratio = The ratio in which the continuing partners acquire the outgoing (deceased ) partner share

New share – Old share

Gaining ratio between A and B = 1/81 : 8/81

= 1 : 8

Share of deceased partner in Goodwill

Death of a Partner : Example 4

Akash , Amol and Anoop are partners sharing profits and losses in the ratio of 3/6 : 2/6 : 1/6. Goodwill of the firm was valued at Rs. 240000 Amol dies. What is Amol ‘s share of goodwill?

Explanation : –

Total value of Goodwill = 240000

Amol s share in profits = 2/6

Amol s share of goodwill = Total value of goodwill x Amol s share in profits

= 240000 X 2/6

= 80000

Share of deceased partner in JLP

Death of a Partner : Example 5

Akash , Anoop and Anmol are partners sharing profits and losses in the ratio of 2/5 : 2/5 : 1/5.They had a joint life policy of Rs. 700000 ,Surrender value of JLP in Balance Sheet is Rs. 200000 Anmol dies. What is the share of Anmol in JLP?

Explanation : –

Amount of policy to be distributed to partner = Policy value – Surrender value of joint life policy in Balance sheet

700000 – 200000

=500000

Share of partners in joint life policy =

Anmol s share in policy 500000 X 1/5 = 100000

Share of deceased partner in the profit

Death of a Partner : Example 6

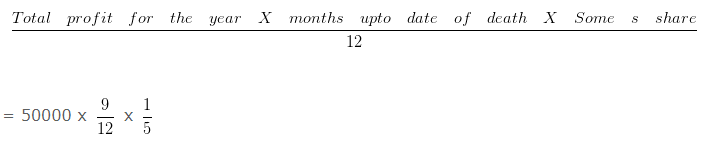

Any , Many and Some are partners sharing profits and losses in the ratio of 3/5 : 1/5 : 1/5. Some died on 31-12-2016 and profit for the year 2016-17 were Rs. 50000 . How much profit for the period 1st April 2016 to 31st March 2017 will be credited to Some ‘s Capital Account?

Explanation : –

Profit for the year 2016-17 = 50000

Number of Month’s profit entitlement to Some = 9

Total Month in a Year = 12

Some s share in profits =

= 7500

Share of partners in Joint Life Policy

Death of a Partner : Example 7

Akash , Anoop and Anmol are partners sharing profits and losses in the ratio of 2/5 : 2/5 : 1/5.They had a joint life policy of Rs. 700000 ,Surrender value of JLP in Balance Sheet is Rs. 200000 . Anmol dies. What is the share of each partner in JLP?

Explanation : –

Amount of policy to be distributed to partner = Policy value – Surrender value of joint life policy in Balance sheet

700000 – 200000

=500000

Share of partners in joint life policy =

Akash’s share in policy 500000 X 2/5 = 200000

Anoop’s share in policy 500000 X 2/5 = 200000

Anmol’s share in policy 500000 X 1/5 = 100000