CA Final Amendment – Country by Country reporting – Provision of Finance Act 2018 –

The various provisions relating to country by country reporting are discussed as under : –

MONETARY THRESHOLD FOR MAINTENANCE OF COUNTRY-BY-COUNTRY REPORT : –

As per Rule 10DB, where the consolidated group revenue of international group exceeds Rs. 5500 crores , the group is required to file Country-by-Country report. In cases where the consolidated group revenue of international group does not exceed this limit, the provisions relating to Country-by-Country report are not applicable on the international group. For this purpose, the consolidated group revenue of international group has to be considered as per the consolidated financial statement.

INTIMATION IN FORM 3CEAC : –

Where the consolidated group revenue of international group exceeds Rs. 5500 crores and the country by country reporting is applicable to the international group, the Indian entity, having a parent entity resident outside India, will be required to provide information on or before the prescribed date in Form 3CEAC :-

a. Whether it is an alternate reporting entity of the international group; or

b. The details of the parent entity or the alternate reporting entity, if any of the international group, and the country of

TIME-LIMIT FOR FILING OF COUNTRY-BY-COUNTRY REPORT UNDER SECTION 286 – AS AMENDED BY THE FINANCE ACT, 2018

The CbC report is required to be filed within a period of 12 months from the end of the reporting accounting year. For example, if the reporting accounting year of the company is FY 2017-18, the CbC report shall be filed till March 31, 2019. [ Section 286(2)].

Intimation in Form 3CEAC shall be filed two months prior to the due date of filing of CbC report. Accordingly, for the FY 2017-18, the intimation shall be filed till January 31, 2019.

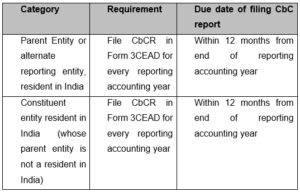

MANNER AND DUE DATE OF FILING OF COUNTRY-BY-COUNTRY REPORT :-

The reporting requirements and filing dates for Country by Country reporting are discussed as under : –

Note :-

Constituent entity resident in India (whose parent entity is not resident in India) needs to submit intimation in Form 3CEAC to specify whether it is alternate reporting entity of the group or details of parent entity, etc. Form 3CEAC should be filed at least two months before the due date of furnishing of CbCR.

- The due date for furnishing of CbCR by the ARE of an international group, the parent entity of which is outside India, with the tax authority of the country or territory of which it is resident, will be the due date specified by that country or territory.

“Reporting accounting year” has been defined to mean the accounting year in respect of which the financial and operational results are required to be reflected in the report referred to in sub-section (2) and sub-section (4).

Amendment

Prior to the amendment by the Finance Act, 2018, the provisions of Section 286, required that the CbC report should be filed on before due date of filing return of income , and intimation in Form 3CEAC shall be filed two months prior to the due date of filing of CbC report i.e., two months prior to due date of filing of income tax return . The Finance Act, 2018 has extended the due date of filing CbC report to 12 months from the end of reporting period and accordingly, the due date of filing intimation in Form 3CEAC is also extended . Given that these amendments are clarificatory in nature, they shall apply in relation to the assessment year 2017-18 and subsequent years.