WITHHOLDING TAX FROM PAYMENTS TO NON-RESIDENTS

SALARY PAYABLE IN FOREIGN CURRENCY – SECTION 192

In terms of Rule 26 read with Rule 115, where tax is required to be deducted on salary payable in foreign currency, TDS deductible on such salary is to be calculated, after converting the salary payable into Indian currency, at the TT buying rateon the date of deduction of tax and applying average rate of income tax to such income.

In other words , the following steps needs to be undertaken : –

- Converting the salary payable into Indian currency ;

- For conversion, apply the TT buying rate on the date of deduction of tax. TT buying rate means Telegraphic transfer buying rate, as adopted by State Bank of India.

- Such converted income has to be used to calculate tax based on the average rate of income tax to such income

Points to be considered

- As per section 9(1)(ii), salary is deemed to accrue or arise in India, if salary is earned in India. Therefore, if a non-resident renders services in India, the salary income would be chargeable to tax in India. The employer has to deduct withholding tax as per Section 192.

- Such income-tax has to be calculated at the average rate of income-tax computed on the basis of the rates in force for the relevant financial year in which the payment is made, on the estimated total income of the assesse.

- Average rate of income-tax means the rate arrived at by dividing the amount of income-tax calculated on the total income, by such total income.

EXAMPLE : –

FCO, (foreign company), seconded an employee to its wholly owned subsidiary in India (i.e., ICO) for which ICO had to pay salary of USD 6,000 per month to the employee, for one month on February 1, 2017 for the month of January, 2017. Calculate the amount of TDS to be deducted by ICO on the basis of following data (assuming such salary is taxable in India) : –

- TT buying rate on 31-1-2017 is Rs 65 per USD

- TT buying rate on 1-2-2017 is Rs 64 per USD

SOLUTION: –

WINNINGS FROM LOTTERIES, CROSSWORD PUZZLES AND HORSE RACES – SECTION 194B AND 194BB

The following incomes would be charged to income-tax at a flat rate of 30% u/s 194B

- Income by way of winnings from lotteries,

- Income by way of Crossword puzzles,

- Income by way of Card game and other game of any sort,

- Income by way of races including horse races, etc.

However, income from owning and maintaining race horses are not covered under these provisions.

NOTE : –

Such tax rate of 30% would be further increased by applicable surcharge, EC and SHEC of 3% .

Points to be considered

- As per Section 2(24)(ix), income includes any winnings from lotteries,crossword puzzles,races including horse races, card games and other games of any sort or from gambling or betting of any form or nature whatsoever.

- “Lottery” includes winnings from prizes awarded to any person by draw of lots or by chance or in any other manner whatsoever, under any scheme or arrangement by whatever name called.

- “Card game and other game of any sort” includes any game show, an entertainment programme on television or electronic mode, in which people compete to win prizes or any other similar game.

- Such incomes are taxable under the head “Income from other sources” under Section 56.

TDS ON WINNINGS FROM LOTTERIES, CROSSWORD PUZZLES ETC – SECTION 194B

Every person, who is responsible for paying such sum discussed above to any resident or non-resident, is required to deduct TDS at the rate of 30% if the amount of payment exceeds Rs. 10,000.

NOTE : –

- EC and SHEC of 3% would be further added on 30%. Surcharge would also be added if applicable.

- Benefit of slab rate is not available at the time of computation of income and such income would be taxable at flat rate of 30%

EXAMPLE 1 : –

Shawn, a non-resident, won the prize money of Rs. 40 lakhs in reality game show during PY 2017-18. Calculate the amount of TDS to be deducted from such payments?

SOLUTION : –

The rate of TDS on such prize money would be 30.90% (including EC and SHEC) under Section 194B. Thus, the amount of TDS would be Rs. 12,36,000 (40,00,000*30.9%). Shawn will get prize money of Rs. 27,64,000 after deduction of TDS.

EXAMPLE 2 : –

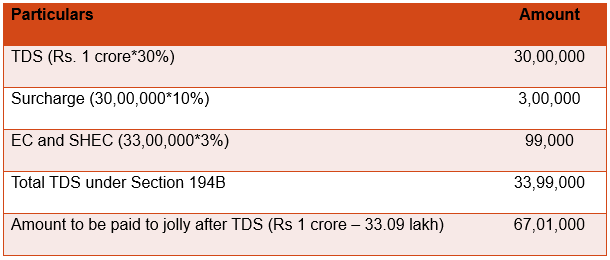

Jolly, a non-resident, won the prize money of Rs 1 crores in Dance Show. Calculate the amount of TDS to be deducted from such payments?

SOLUTION : –

The rate of TDS on such prize money would be 30% under Section 194B. The surcharge of 10% would also apply as the income is in the range of Rs 50 lakh- Rs 1 crore.

EXAMPLE 3 : –

John, a non-resident, won the prize money of Rs. 10,000 in a game show . Calculate the amount of TDS to be deducted from such payments ?

SOLUTION : –

TDS under Section 194B would apply on winning from any game show only when the prize money is more than Rs. 10,000. As John has won prize money of only Rs. 10,000, no TDS would be deducted on such payment. John will get the entire prize money of Rs. 10,000.

CASES WHERE WINNINGS ARE WHOLLY /PARTLY IN KIND, AND PARTLY IN CASH

In certain cases, the winnings earned may be wholly in kind , or partly in cash and partly in kind .

Where these winnings are wholly in kind, or partly in cash and partly in kind , but the part in cash is not sufficient to meet the liability of TDS, the person responsible for paying shall, before releasing the winnings, ensure that tax has been paid in respect of the winnings. Where the cash is sufficient to cover TDS, such cash shall be adjusted to TDS and remaining cash and winnings in kind shall be paid to the winner.

TDS ON WINNINGS FROM LOTTERIES, CROSSWORD PUZZLES ETC

EXAMPLE 1 : –

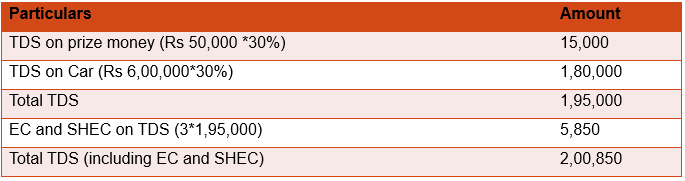

In August 2017, Paul, a non-resident, won the prize money of Rs 50,000 in a Singing reality show. He also won a car worth Rs 6 lakhs in the same show. Calculate the amount of TDS on such prize and how such TDS liability would be paid by deductor ?

SOLUTION : –

TDS would be deducted under Section 194B on the monetary prize and non-monetary prize (i.e., Car).

The amount of cash prize money (i.e., Rs 50,000), is less than the TDS (i.e., Rs 2,00,850). In this case , the deductor can recover only Rs 50,000 from amount payable. Deductor would request Paul to pay balance amount of TDS of Rs 150,850 (2,00,850-50,000) , before releasing the Prize to Paul.

EXAMPLE 2 : –

In the Example 1, assume that Paul has won only Car worth Rs 6 lakhs in singing reality show. Calculate the amount of TDS to be paid by Paul to get the Car ?

SOLUTION : –

Paul is required to pay TDS of Rs 1,85,400 (Rs 6,00,000*30.9%)

TDS FROM WINNINGS BY BOOKMAKER/ HORSE RACING – SECTION 194BB

As per Section 194BB, following persons are liable to deduct TDS at 30%, before paying any income by way of winnings from any horse race (it includes more than one horse race), or for winning from wagering or betting in any race course.

- a bookmaker ; or

- a Government permitted licensee

Further, winnings by way of jackpot would also fall within the scope of section 194BB.

The TDS provision shall be applicable only when the total winnings are above Rs 10,000. However, where the total winnings are above Rs. 10,000, but the winnings are paid in instalments of less than Rs. 10,000, TDS will have to be deducted .

EXAMPLE 1 : –

Philip won prize money of Rs 10,000 from betting in horse race. Calculate the TDS on such amount under Section 194BB ?

SOLUTION : –

TDS under Section 194BB would apply on winning from horse race exceeding Rs 10,000. As Philip has won only Rs 10,000, no TDS would be deducted on such payment.

EXAMPLE 2 : –

Shane, a non-resident, won prize money of Rs 40 lakhs from betting in horse race during PY 2017-18. Calculate the amount of TDS to be deducted from such payments ?

SOLUTION : –

The rate of TDS on such prize money would be 30.90% (including EC and SHEC) under Section 194BB. Thus, the amount of TDS would be Rs 12,36,000 (40,00,000*30.9%). Shane will get prize money of Rs 27,64,000 after deduction of TDS.

EXAMPLE : –

Alex, a non-resident, won prize money of Rs 21,000 from betting in horse race. However, prize money would be paid in three installments of Rs 7,000 each. Calculate the TDS on such amount under Section 194BB?

SOLUTION : –

TDS of Rs 6,489 (21,000*30.9%) would be deducted and remaining amount of Rs 14,511 would be paid to the Alex in three installments. Even though the winnings are paid in instalments of less than Rs. 10,000, sonce totoal winnings exceeds Rs. 10,000, TDS will have to be deducted .

Set off of losses in some transactions against profits of other transactions

As per section 58(4) , in computing income by way of any winnings from lotteries, crossword puzzles, races including horse races, card games and other games of any sort or from gambling or betting of any form or nature, whatsoever, no deduction of any expenditure shall be allowed .

Further, no losses shall not be set-off against aforesaid income while computing the amount of TDS. Where the payor credits such winnings, and debits the losses to the individual account of the punter, TDS would still be deducted on the gross winnings.

EXAMPLE : –

Shaun, a non-resident, won Rs 50,000 on betting from horse race. He also incurred a loss of Rs 10,000 from such betting. Bookmaker sets off the loss with the prize money and is liable to pay Rs 40,000 to Shaun. Calculate the amount of TDS?

SOLUTION : –

The rate of TDS would apply on prize money (i.e., Rs 50,000) without adjusting losses. Thus, the amount of TDS would be Rs 15,450 (50,000*30.9%). Shaun will get prize money of Rs Rs 24,550 (50,000 -10,000- 15,450) after deduction of TDS.

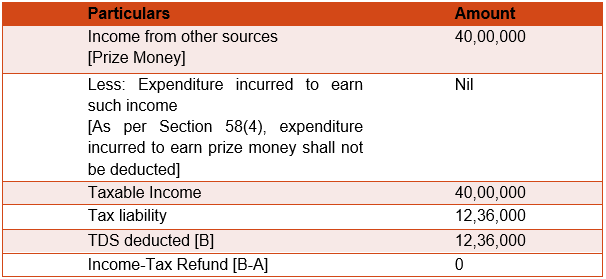

EXAMPLE : –

Mr. Bond, a non-resident, won the prize money of Rs. 40,00,000 from reality show during PY 2017-18. TDS of Rs 12,36,000 has been deducted on such income. He has also incurred travelling expenditure of Rs 50,000 to earn such income Calculate the amount of taxable income ?

SOLUTION : –

PAYMENTS TO NON-RESIDENT SPORTSMEN OR SPORTS ASSOCIATION – SECTION 194E

i. APPLICABILITY : –

Section 194E provides for deduction of tax at source @20% in respect of the following incomes, referred to in section 115BBA which are payable to a non-resident sportsman (including an athlete) or an entertainer ornon-resident sports association.

- income by way of participation in India in any game or sport;

- income by way of advertisements; and

- income by way of contribution.

Section 194E is applicable to non-resident sportsman/entertainer who is not a citizen of India.

ii. TIME OF DEDUCTION OF TAX : –

Tax has to be deducted from such payments at the time of credit of such income to the account of the payee or at the time of payment thereof, whichever is earlier.

EXAMPLE : –

During the FY 2017-18, Del Villiers, a non Indian citizen participated in Cricket Tournament in India. He earned prize money of Rs 20 lakhs during such Tournament. What would be the TDS liability on such income ?

SOLUTION : –

Prize money earned by Del Villiers from Cricket Tournament in India would be taxable at 20.6% (including EC and SHEC). Thus, the TDS liability would be Rs 4,12,000 (40,00,000*20.6%).

SPECIAL RATE OF TAX ON INTEREST RECEIVED FROM NOTIFIED INFRASTRUCTURE DEBT FUNDS – SECTION 115A

Interest income received by a non-corporate non-resident , or a foreign company from infrastructure debt funds would be subject to taxed and liable for deduction of TDS at a rate of 5% of interest paid/credited by such fund.

While the income of the infrastructure fund is exempt from Tax under section 10(47), where such fund distributes interest income to its investors, such income would be taxable in the hands of the recipient

1. TIME OF DEDUCTION : –

The person responsible for making the payment shall deduct income-tax @5%, at the time of credit of such income to the account of the payee , or at the time of payment thereof, whichever is earlier.

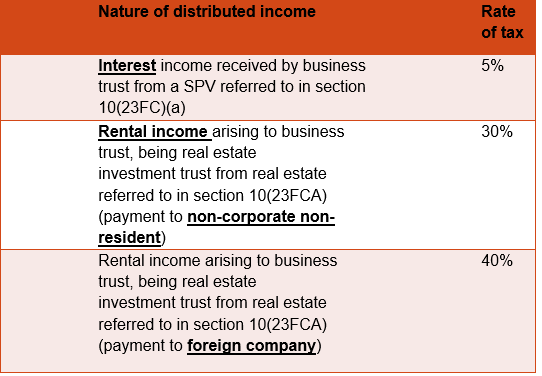

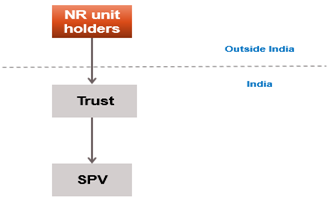

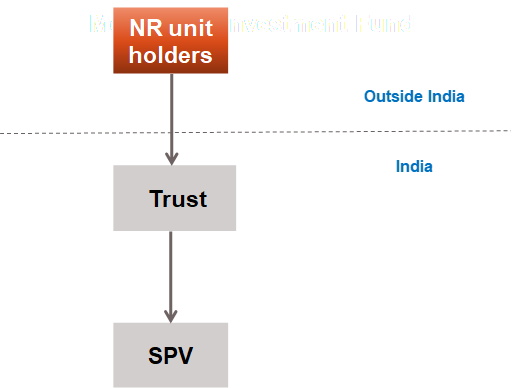

INCOME FROM UNITS OF A BUSINESS TRUST TO NON-RESIDENT – SECTION 194LBA

1. APPLICABILITY : –

Where a business trust has specified distributed income, which is payable to its unit holder, who are non-resident non-corporate assessee or a foreign company, the business trust shall be liable to deduct tax at source on such income at the following rates : –

SPECIFIED DISTRIBUTED INCOME MEAN : –

- Interest income received by business trust from SPV [referred to in Section 10(23FC)(a)] or

- Rental income arising to Real Estate Investment Trust from real estate referred to in section 10(23FCA)

It may be noted that such interest income and rental income is exempt in the hands of business trust under Section 10(23FC) and Section 10(23FCA), respectively. However, when such interest income and rental income is distributed to unit holders, TDS would be charged .

Business trust means a trust registered as an Infrastructure Investment Trust (Invit) or a Real Estate Investment Trust (REIT) under SEBI norms, whose units of are required to be listed on a recognized stock exchange in accordance with the aforesaid regulations.

- TIME OF DEDUCTION : –

TDS shall be deducted at the time of credit of such payment to the account of the payee or at the time of payment thereof, whichever is earlier.

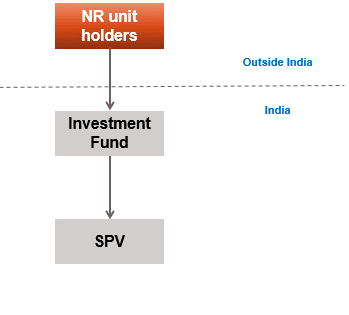

INCOME OF UNITS OF INVESTMENT FUND OF NON-RESIDENT UNIT HOLDERS – SECTION 194LBB

WHAT IS AN INVESTMENT FUND

An investment fund is any fund established or incorporated in India, which has been granted a certificate of registration as a Category I or a Category II , Alternative Investment Fund and is regulated under the SEBI (Alternative Investment Fund) Regulations, 2012, made under the SEBI Act, 1992 . Such a fund can be organized in the form of a: –

- Trust or

- Company or

- LLP or

- Body corporate

1. APPLICABILITY AND RATE OF TAX : –

Where the Investment funddistributesany income (other than business income taxable at fund level)to a unit holder , who is a non-resident non-corporate or foreign company, the fund shall deduct tax at source at rates in force on such income. Such tax has to be deducted at the time of credit of such income to the account of the payee or at the time of payment, whichever is earlier.

2. CREDIT OF INCOME TO SUSPENSE ACCOUNT : –

Any credit to a “suspense account” or any other account in the books of account of payer, shall be deemed to be the credit of such income to the account of the payee, and the provisions of section 194LBB shall apply accordingly.

3. NO TDS IF INCOME IS NOT CHARGEABLE UNDER THE ACT : –

No deduction is to be made in respect of any income that is not chargeable to tax under the IT Act.

INCOME IN RESPECT OF INVESTMENT MADE IN A SECURITISATION TRUST – SECTION 194LBC

Where any income is payable to an investor, being a resident, in respect of an investment in a securitisation trust (referred to in clause (d) of the Explanation occurring after section 115TCA), the person responsible for making the payment shall deduct income-tax thereon.

MEANING OF INVESTOR : –

Investor means a person who is holder of any securitised debt instrument or securities or security receipt issued by the securitisation trust .

MEANING OF SECURITIES : –

Securities means debt securities issued by a Special Purpose Vehicle as referred to in the guidelines on securitisation of standard assets issued by RBI .

1. RATE OF TDS : –

TDS shall be deducted at

- 40% when payee is a foreign company.

- 30% when payee is non-corporate non-resident.

2. CREDIT OF INCOME : –

Any such income credited to any “suspense account” or by any other name, in the books of account of the person liable to pay such income, shall be deemed to be the credit of such income to the account of the payee, and the provisions of section 194LBC shall apply accordingly .

3. TIME OF DEDUCTION : –

TDS shall be deducted at the time of credit of such payment to the account of the payee or at the time of payment, whichever is earlier.

4. APPLICATION FOR LOW OR NIL DEDUCTION OF TAX AT SOURCE : –

Investors can obtain low or nil deduction of tax certificateby making an application to the Assessing Officer, who can issue a certificate under section 197 for no deduction of income-tax or deduction of income-tax at a lower rate .

INCOME BY WAY OF INTEREST FROM AN INDIAN COMPANY ON FOREIGN CURRENCY BORROWINGS – SECTION 194LC

Interest paid by an Indian company or a business trust to a foreign company or

a non-corporate non-resident in respect of borrowing made in foreign currency from a source outside Indiashall attract concessional withholding tax @5%

NOTE : –

This provision is applicable if interest is paid or payable at rate approved, by Central Government considering terms of the loan or bond and its repayment

CONDITIONS : –

Concessional rate of TDS on interest is applicable, if the money has been borrowed in foreign currency from sources outside India : –

- Under a loan agreement (at any time on or after 01.07.2012 but before 6.2020)

- By way of issue of long term infrastructure bonds ( at any time on or after July 1, 2012 but before October 1, 2014); or

- By way of issue of long-term bonds (at any time on or 01.10.2014 but before 01.07.2020)

- In respect of monies borrowed from sources outside India by way of rupee denominated bond before 01.07.2020.

NOTE : –

Loan agreement or bonds should be approved by the Central Government .

NON-APPLICABILITY OF HIGHER RATE OF TDS UNDER SECTION 206AA FOR NON-FURNISHING OF PAN

Higher TDS rate of 20% u/s 206AA for non-furnishing of PAN would not be applicable on payment of interest on long-term bonds, referred to in Section 194LC, to a non-corporate non-resident or to a foreign company.

INTEREST ON GOVERNMENT SECURITIES OR RUPEE-DENOMINATED BONDS OF AN INDIAN COMPANY – SECTION 194LD

Rate of TDS

Interest payable to FII or QFI on rupee denominated bond of an Indian company or a Government security,shall be subject to tax deduction at source at a concessional rate of 5% .

Extent of interest entitled to lower withholding

However, the concessional rate of 5% shall be applicable only on interest, which does not exceed the rate of interest notified by the Central Government in this behalf.

Time period of investment

In order to claim lower withholding tax, investment should be made by FII or QFI during the period 1.6.2013 and 30.06.2020in rupee denominated bonds of Indian company or Government Security.

Tax shall be deducted at the time of credit of such income to the account of the payee or atthe time of payment of such income, whichever is earlier.

FII means Foreign Institutional Investors specified by the Central Government by notification in the Official Gazette .

QFI means Qualified Foreign Investors i.e., Foreign Investors, being non-residents, who meet certain KYC requirements under SEBI laws and are hence permitted to invest in equity and debt schemes of Mutual Funds, thereby enabling Indian Mutual Funds to have direct access to foreign investors and widen the class of foreign investors in Indian equity and debt market. QFI does not include FII.

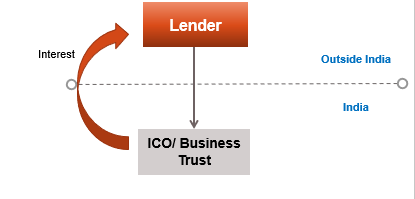

APPLICABILITY OF WITHHOLDING TAX ON PAYMENT OF INTEREST OR ANY OTHER SUM TO NON-RESIDENT – SECTION 195(1)

Any person (whether resident or non-resident), responsible for paying interest (other than interest referred to in Section 194LB/194LC/194LD) or any other sum (other than salaries)chargeable to tax, to a non-corporate non-resident or to a foreign companyis liable to deduct tax at source at the rates prescribed by the relevant Finance Act .

The following person should be noted in this regard : –

- Payment may be made by any person (whether resident or non-resident) ,

- Payment could be in the nature of : –

- Interest (other than interest referred to in Section 194LB/194LC/194LD) or

- Any other sum (other than salaries)

- Such sum should be chargeable to tax

- Sum could be payable to a non-corporate non-resident or to a foreign company

- Tax is to be deducted at the rates prescribed by the relevant Finance Act .

Person responsible for paying any such sum to non-resident shall furnish the information relating to payment in Form 15CA/CB.

The tax is to be deducted at source at the time of credit of such income to the account of the payee or at the time of payment thereof, whichever is earlier.

Where any interest or other sum as aforesaid is credited to any account (whether called “Interest payable account” or “Suspense account” or by any other name) in the books of account of the payer, such crediting shall be deemed to be credit of such income to the account of the payee

POINTS TO CONSIDER

i. INTEREST PAYMENTS : –

In order to attract withholding tax under Section 195, interest payments to non-resident should be chargeable to tax . No withholding tax liability would arise on interest payments when such interest income is exempt either under IT Act or under DTAA or both.

ii. OTHER PAYMENTS : –

For any other payments to non-residents, withholding tax liability would not arise when such payment is exempt either under IT Act or under DTAA or both.

iii. SALARY PAYMENTS : –

For salary payments to non-resident, provisions of Section 195 would not be attracted. In such case, withholding tax would be made as per provisions of Section 192.

iv. STATUS OF PAYEE : –

In order to subject an item of income to deduction of tax under this section the payee must be a non-corporate non-resident or a foreign company.

v. STATUS OF PAYER: –

Withholding tax obligation u/s 195(1) would be applicable on both resident and non-resident.If the payment by a non-resident person represents income of non-resident payee which is chargeable to tax in India, then tax has to be deducted at source even by non-resident Payor.

Example 1

Indian Bank is crediting interest on NRE account to non-resident Individual. Whether Indian Bank is liable to withhold tax under Section 195 ?

SOLUTION : –

Withholding tax obligation would arise under Section 195 only when interest income is chargeable to income-tax.In this case, interest paid by Indian bank on money credited in NRE Account of non-resident individual would be exempt from tax under Section 10(4)(ii) of the IT Act. Thus, such interest income is not chargeable to income-tax . Accordingly, no withholding tax would arise on such interest payments under Section 195.

Example 2 : –

Yama India Pvt. Ltd. pays royalty of Rs 1 lakhs to Bicroloft Inc. (USA) . Such royalty payment is taxable under Section 9(1)(vi). However, it is excluded from the definition of royalty under India-USA DTAA. Whether Yama India Pvt. Ltd is liable to withhold tax on such payments?

SOLUTION : –

No withholding tax liability arise on any payments to non-residents, when such payment are exempt either under IT Act or under DTAA. In this case, payment made by Yama India are outside the purview of royalty definition as per India-USA DTAA . Accordingly, no withholding tax would arise on royalty payment to Bircroloft Inc. as such payment is exempt from tax under DTAA .

Example 3

X India Pvt. Ltd pays royalty of Rs 1 lakhs to Y India Pvt. Ltd. (another Indian company). Whether such payment is liable to withhold tax at source under Section 195 ?

SOLUTION : –

Section 195 would be attracted only when payment is made either to a foreign company or non-corporate non-resident. In this case, Section 195 would not be attracted as payee is resident. However, the provisions of Section 194J may be attracted.

Example 4

Zata USA pays royalty of Rs 1 lakhs to Aahoo Inc. , which is for services pertaining to its Indian operations .Whether Zata USA is liable to withhold tax at source under Section 195?

SOLUTION : –

In this case Zata USA would be liable to withhold tax under Section 195, if the payment is taxable both under the IT Act and the Treaty.

Example 5

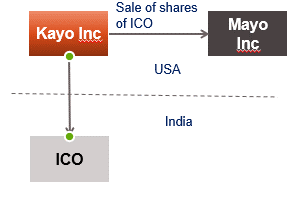

Kayo Inc. (USA) has wholly owned subsidiary in India (i.e., ICO). Kayo Inc. sold shares of ICO to Mayo Inc.. Whether Mayo Inc. is liable to withhold tax under Section 195 while making payment to Kayo Inc. ?

SOLUTION : –

As per Section 9(1)(i), any income arising from transfer of capital asset situated in India would be deemed to accrue or arise in India. In this case, capital gains from sale of shares would be deemed to accrue or arise in India as shares were situated in India.

Mayo Inc is required to withhold tax before making payment to Kayo Inc. as the payment represents income of Kayo Inc. , chargeable to tax in India, provided such income is not exempt from tax under the applicable DTAA.

RELEVANCE OF BUSINESS CONNECTION FOR WITHHOLDING TAX – EXPLANATION 2 TO SECTION 195(1)

The obligation to comply with section 195(1)is applicable on all persons, resident or non-resident, irrespective of whether the non-resident has : –

- A residence in India; or

- Place of business in India; or

- Business connection in India; or

- Any other presence in India.

This explanation is clarificatory in nature and Is therefore applicable for earlier period as well.

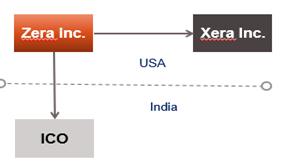

Example 6 : –

Zera Inc. sold shares of Indian company (ICO) to Xera Inc. Such Xera Inc. does not have any business connection or place of business in India. Whether Xera Inc. is liable to withhold tax while making payment to Zera Inc. on purchase of shares of ICO ?

SOLUTION : –

Xera Inc. is liable to withhold tax as payment is chargeable to tax in India irrespective of the fact that it does not have any presence in India.

WITHHOLDING TAX WHEN INTEREST IS PAYABLE BY GOVERNMENT OR PUBLIC SECTOR BANK – SECTION 195(1)

Where interest is payable by the Government or a public sector bank or a public financial institution deduction of tax shall be made only at the time of payment (and not on accrual basis).

EXPLANATION TO SECTION 10(23D)

“Public sector bank” means –

- The State Bank of India constituted under the State Bank of India Act, 1955,

- A subsidiary bank as defined in the State Bank of India (Subsidiary Banks) Act, 1959,

- A corresponding new Bank constituted under section 3 of the Banking Companies (Acquisition and Transfer of Under-takings) Act, 1970, or under section 3 of the Banking Companies (Acquisition and Transfer of Under-takings) Act, 1980 and

- A bank included in the category “other public sector banks” by the Reserve Bank of India

SECTION 4A OF THE COMPANIES ACT, 1956 provides that the following institutions shall be regarded as “Public financial institution” –

- the Industrial Credit and Investment Corporation of India Limited (“ICICI”), a company formed and registered under the Indian Companies Act, 1913 ;

- the Industrial Finance Corporation of India (“IFCI”), , established under section 3 of the Industrial Finance Corporation Act, 1948 ;

- the Industrial Development Bank of India (“IDBI”),, established under section 3 of the Industrial Development Bank of India Act, 1964 ;

- the Life Insurance Corporation of India (“LIC”), established under section 3 of the Life Insurance Corporation Act, 1956 ;

- the Unit Trust of India (“UTI”), established under section 3 of the Unit Trust of India Act, 1963 ;

- the Infrastructure Development Finance Company Limited, a company formed and registered under the Companies Act

NO WITHHOLDING TAX ON DIVIDEND PAYMENT TO NON-RESIDENT – SECTION 195(1)

No tax deduction shall be made in respect of any dividends declared/distributed/paid by a domestic company to non-resident, which is exempt in the hands of the shareholders under Section 10(34) .

Example : –

Yoho India Pvt. Ltd. declares dividend of Rs 1,00,000 to non-resident shareholders , on which it paid Dividend Distribution tax (“DDT”).

Whether Yoho India is liable to withhold tax on such payment?

SOLUTION : –

Since Yoho India has paid dividend distribution tax on such dividend, such dividend would be exempt from tax in the hands of non-resident under Section 10(34) . Accordingly, Yoho not deduct TDS on such dividend payment .

APPLICATION BY PAYOR TO AO TO DETERMINE THE APPROPRIATE PROPORTION OF SUM CHARGEABLE TO TAX – SECTION 195(2)

In certain cases, where a person is responsible for making any payment to the non-resident, the entire sum so payable may not be income of the non-resident. The issue which arises is, how should the income on which tax has to be deducted should be calculated ?

To deal with such situation, section 195(2) provides that where the person responsible for making payment to the non-resident considers that the whole of payment would not be income chargeable to tax in the hands of non-resident recipient, he may make an application to the Assessing Officer to determine, the appropriate proportion of such sum so chargeable .

When the AO determines such proportion, tax shall be deducted under section 195(1) only on that proportion of the sum which is so chargeable.

Example : –

ICO obtains certain installation services and onshore/offshore supply of equipment from ICO and was not sure whether such payments were taxable. Whether ICO can make application before AO to determine the sum which is liable to TDS ?

SOLUTION : –

As per provisions of Section 195(2), the Payor can make application before the AO to determine the portion of payment which is liable to TDS.

CERTIFICATE OF NON-DEDUCTION OF TAX AT SOURCE – SECTION 195(3)

Non-resident recipient , which can be a non-corporate non-resident or foreign company, can also make an application to the Assessing Officer for grant of certificate authorizing him to receive interest or other sum [on which TDS has to be deducted u/s 195(1)]without deduction of tax.

Where any such certificate is granted, every person responsible for paying such interest or other sum to the person to whom certificate is granted, shall make payment of such interest or other sum without deduction of tax at source under section 195(1), so long as the certificate in force.

VALIDITY PERIOD OF CERTIFICATE OF NON-DEDUCTION OF TAX AT SOURCE – SECTION 195(4)

Certificate of non-deduction of TDS issued u/s 195(3) shall remain in force till the expiry of the period specified therein .Generally, such certificates are valid for a particular financial year. However, if it is cancelled by the Assessing Officer before the expiry of such period, the certificate shall remain in force till such cancellation .

Example 1 : –

ICO has to make royalty payment of Rs 1,00,000 to FCO on August 7, 2017. FCO provides certificate to ICO from AO, wherein a Nil withholding tax rate is granted by AO for PY 2017-18. The rate of withholding tax under IT Act is 10%. At what rate TDS should be deducted ?

SOLUTION : –

ICO is not liable to withhold tax on such royalty payments as FCO has valid certificate permitting payor for nil withholding during the entire PY 2017-18 .

EXAMPLE 2 : –

ICO has to make payment of fees for technical services of Rs 1,00,000 to FCO on August 7, 2017. FCO provides certificate for nil withholding tax to ICO. Such certificate is valid for PY 2016-17. The rate of withholding tax under IT Act is 10%. At what rate TDS should be deducted?

SOLUTION : –

ICO should not consider certificate for nil withholding tax as such certificate is valid for PY 2016-17 but payment is to be made during PY 2017-18. ICO would deduct TDS of Rs 10,000 on such payment.

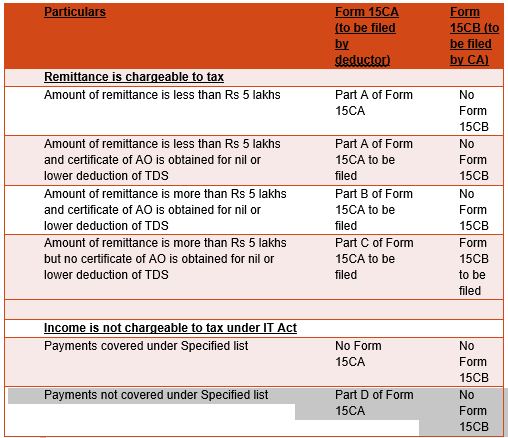

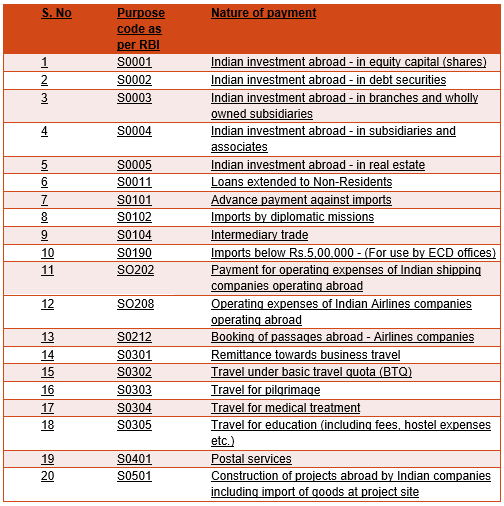

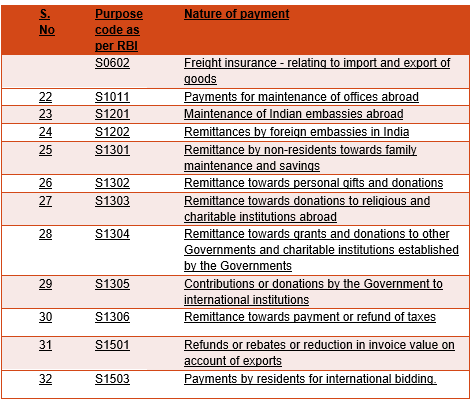

FURNISHING OF FORM 15CA/15CB FOR PAYMENTS TO NON-RESIDENT – SECTION 195(6)

Section 195(6) requires the Payor of a sum to non-resident, to furnish certain prescribed information in Form 15CA/15CB, before paying any sumto non-resident, whether or not the payment is chargeable to tax .

Payor would be required to furnish form 15CA/15CB as per the following table even if payment to non-resident is not taxable : –

SPECIFIED LIST : –

PROCEDURE FOR REFUND OF TDS UNDER SECTION 195

In certain cases, the payor any sum to non-resident make a duct and deposit the higher amount of TDS, then what is applicable in a particular transaction. In such a case, if the deductee were to claim the credit/ refund, of such TDS, it would be a time consuming and lengthy process. In order to deal with such situations Circular No.07/2007 dated 23.10.2007 of CBDT (as modified by Circular No. 7/2011 dated 27.9.2011), lays down the procedure for refund of TDS under section 195 , to the person deducting tax at source from the payment to a non-resident .this is due to the reason that the excess amount paid to the Government, in such cases does not constitute tax.

The said Circular allows refund to the person making payment under section 195 [in the circumstances indicated in point c in next slide) ] if the income does not accrue to the non-resident or if the income is accruing, but no tax is due or tax is due at a lesser rate . The circumstances for TDS refund are as under : –

- The contract is cancelled and no remittance is made to the non-resident ;

- The remittance is duly made to the non-resident, but the contract is cancelled. In such cases, the remitted amount has been returned to the person responsible for deducting tax at source ;

- The contract is cancelled after partial execution and no remittance is made to the non-resident for the non-executed part ;

- The contract is cancelled after partial execution and remittance related to non-executed part is made to the non-resident. In such cases, the remitted amount has been returned to the person responsible for deducting the tax at source or no remittance is made but tax was deducted and deposited at the time of credit of amount to the account of the non-resident ;

- There occurs exemption of the remitted amount from tax either by amendment in law or by notification under the provisions of Income-tax Act, 1961 ;

- An order is passed under section 154 or 248 or 264 of the Income-tax Act, 1961 reducing the tax deduction liability of a deductor under section 195 ;

- There occurs deduction of tax twice from the same income by mistake ;

- There occurs payment of tax on account of grossing up which was not required under the provisions of the Income-tax Act, 1961 ;

- There occurs payment of tax at a higher rate under the domestic law while a lower rate is prescribed in the relevant double taxation avoidance treaty entered into by India .

PROCEDURE FOR REFUND OF TDS UNDER SECTION 195 – TDS DEDUCTED AT DTAA RATES WHICH ARE HIGHER THAN IT ACT RATE

Under the provisions of the Revised Circular No.7/2011 dated 27.9.2011, modified old Circular and the CBDT has allowed refund of TDS under section 195 to Payor , where deduction of tax is made at a higher rate under the relevant DTAA while a lower rate is prescribed under the domestic law .

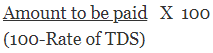

INCOME PAYABLE NET OF TAX – SECTION 195A

Where, TDS is to be borne by Payor under an agreement or other arrangement with the Non-resident, then, for deducting TDS, income shall be increased to such amount as would, after deduction of tax thereon, be equal to the net amount payable under such agreement or arrangement .

TDS COMPUTATION IN CASE OF GROSSING UP : –

STEP 1 :

Calculate the grossed-up amount

STEP 2 :

Rate of TDS X Amount calculated in Step 1

Example : –

ICO has to pay royalty of Rs 90,000 to FCO. However, as per the agreement TDS would be borne by ICO. Rate of TDS as per IT Act is 10%. Calculate the amount of TDS ?

SOLUTION : –

In such a case, the TDS would be calculated as under :

NOTE : –

No grossing up is required in the case of tax paid under section 192(1A), by an employer on the non-monetary perquisites provided to the employee.

INCOME FROM UNITS – SECTION 196B

1) RATE OF TDS : –

Any person, responsible for making the following payment to an overseas financial organisation (i.e., Offshore Fund) shall deduct tax @ 10% on : –

A ) income in respect of units of mutual funds or UTI (referred to in section 115AB) ; or

B ) income by way of long-term capital gains arising from the transfer of such units.

2 TIME OF DEDUCTION OF TDS : –

TDS shall be deducted at the time of credit of such income to the account of the payee or at the time of payment thereof, whichever is earlier.

INCOME FROM FOREIGN CURRENCY BONDS OR SHARES OF INDIAN COMPANY – SECTION 196C

The person responsible for making the following payment to a non-resident shall deduct tax @ 10%-

- Income by way of Interest on bonds [referred to in Section 115AC] or

- Dividends in respect of Global Depository Receipts [referred to in section 115AC] or

- Long-term capital gains arising from the transfer of such bonds or Global Depository Receipts.

NOTE : –

- No TDS shall be deducted in respect of any dividends referred to in section 115-O..

- TDS shall be deducted at the time of credit of such income to payee or at the time of payment, whichever is earlier.

INCOME OF FOREIGN INSTITUTIONAL INVESTORS FROM SECURITIES – SECTION 196D

The person responsible for making the any payment in respect of securities referred to in Section 115AD(1)(a) to a Foreign Institutional Investor shall deduct tax @ 20% at the time of credit of such income to payee or at the time of payment, whichever is earlier.However, no TDS shall be deducted in respect of the following –

- Any dividends referred to in section115-O ;

- Income, by way of capital gains arising from the transfer of securities referred to in section 115AD, payable to a Foreign Institutional Investor.

CERTIFICATE FOR DEDUCTION OF TAX AT A LOWER RATE – SECTION 197

A non-resident can make an application for lower deduction or Nil deduction of TDS where, income-tax is required to be deducted atthe “rates in force”under the following Sections : –

- Section 192 : TDS obligation on salary payments

- Section 194G : TDS obligation on commission, etc. on sale of lottery tickets

- Section 194LBB : TDS on income of units of investment funds

- Section 194LBC : TDS on income distributed by securitisation trust

- Section 195 : TDS obligation on interest and other payments

I. PROCEDURE TO OBTAIN LOWER WITHHOLDING : –

Assessee can make an application to the Assessing Officer for deduction of tax at a lower rate or for non-deduction of tax.If the Assessing Officer is satisfied that the total income of the recipient justifies the deduction of income-tax at lower rates or no deduction of income-tax, he may give such certificate.

II. TDS ON BASIS OF CERTIFICATE : –

Where the Assessing Officer issues such a certificate for lower deduction or nil deduction of TDS, then the Payorshall deduct income-tax at such lower ratesspecified in the certificate or deduct no tax, until such certificate is cancelled by the Assessing Officer.

EXAMPLE : –

ICO has to make payment of royalty of Rs 2,00,000 to FCO (foreign company). The rate of TDS as per IT Act is 10%. However, such FCO has taken certificate of lower deduction, which specifies TDS rate of 5%. Compute the amount of TDS to be deducted by ICO ?

SOLUTION : –

ICO should deduct TDS as per the rate specified in certificate. Thus, ICO should deduct TDS of Rs 10,000 and remit Rs 1,90,000 to ICO.

CREDIT FOR TDS – SECTION 199

Where any TDS is paid to the credit of the Central Government , such payment shall be treated as payment of tax on behalf of the following persons: –

- Person from whose income such TDS deduction was made (i.e., recipient of income) ; or

- Owner of the security ; or

- Depositor , in case of payment of interest on deposits) ; or

- Owner of property ; or

- Unit-holder, in case of income from units of UTI, Mutual funds, etc. ; or

- Shareholder, in case of payment of dividend.

Any sum referred to in Section 192(1A) from income in the nature of salary, and paid to the Central Government, shall be treated as the tax paid on behalf of the person in respect of whose income, such payment of tax has been made .

Section 192(1A)

An employer has been given an option to pay tax on the whole or part value of perquisite (not provided for by way of monetary payments), on behalf of an employee, without making any deduction from the income of the employee .

RULE 37BA – CREDIT FOR TDS FOR THE PURPOSES OF SECTION 199

TDS CREDIT TO PAYEE : –

Where any TDS has been deducted by the payor, such payor is under an obligation to deposit the tax so deducted, file a TDS return and inform the tax office that the tax has been deposited on behalf of the non-resident payor.

Rule 37BA(1) provides, that credit for TDS shall be given to the person to whom the payment has been made or credit has been given (i.e., the deductee) , on the basis of information furnished by the deductor in TDS return.

TDS CREDIT TO OTHER PERSON : –

Clause (i) of Rule 37BA(2) provides that where, the whole or any part of the income , on which TDS has been deducted is assessable in the hands of a person other than the deductee, credit for such TDS shall be given to the other person and not to the deductee.

In such a case, the deductee should file a declaration with the deductor to this effect, and the deductor should report the tax deduction in the name of the other person in TDS return.

EXAMPLE : –

ICO has paid technical fees to FCO (foreign company) amounting Rs. 90,000 after deducting TDS of Rs 10,000 on such payment. FCO files declaration with ICO that such income is taxable in the hands of FCO 1 (other foreign company). Whether FCO 1 will get credit of TDS?

SOLUTION : –

FCO 1 will get credit of TDS of Rs 10,000 when ICO files TDS return with PAN of FCO 1.

HIGHER RATE OF TDS ON NON-FURNISHING OF PAN TO DEDUCTOR – SECTION 206AA(1)

In order to track various payment to non-resident, and ensure, that all such non-resident make tax payments on income which are liable to tax in India, Section 206AA was introduced in the Income Tax Act paper submission of PAN was made mandatory for submission by the non-resident , failing which a higher rate of TDS was to be deducted from all such payments.

Section 206AA(1) provides, that any person entitled to received any income,on which tax is deductible in India, shall mandatorily furnish his PAN to the deductor (i.e, Payor) . If such a person fails to pay the PAN to the deductor, tax shall deducted on such payments at source at higher of the following rates : –

- The rate prescribed in the IT Act ;

- The rate mentioned in the Finance Act or DTAA (i.e., rates in force) ; or

- At the rate of20% .

POINT TO CONSIDER :-

The deductee shall furnish his PAN to the deductor and both shall indicate the same in all the correspondence, bills, vouchers and other documents which are sent to each other .

SECTION 206AA(6) : –

Where the PAN provided to the deductor is invalid or does not belong to the deductee,

- it shall be deemed that the deductee has not furnished his PAN to the deductor ; and

- TDS would be deducted at aforesaid rates .

EXAMPLE 1 : –

ICO has to make payment of royalty of Rs 5,00,000 to FCO . FCO does not furnish its PAN to ICO or any other document, that would evidence that it is a resident of the other Treaty country.As per IT Act the rate of withholding tax would be 10% on such royalty payment .

At what rate TDS should be deducted ?

SOLUTION : –

As per Section 206AA, if the payee does not furnish its PAN to the deductor, then TDS would be deducted at higher of the following rates : –

- The rate prescribed in the IT Act;

- The rate mentioned in the Finance Act or DTAA; or

- At the rate of 20%.

Rate of TDS on royalty is 10%. However, the highest rate of 20% would be apply under Section 206AA as FCO failed to furnish its PAN to ICO. Thus, TDS of Rs 1,00,000 would be deducted on such royalty payment.

EXAMPLE 2 : –

ICO has to make payment of interest of Rs 5,00,000 to Mauritius Bank. Such bank does not furnish its PAN to ICO. The rate of withholding tax would be 20% as per IT Act and the rate of withholding tax would be 7.5% under India-Mauritius DTAA. At what rate TDS should be deducted?

SOLUTION : –

TDS would be deducted at higher of the following rates:

- The rate prescribed in the IT Act (i.e., 20%);

- The rate mentioned in the Finance Act or DTAA (i.e., 7.5%); or

- At the rate of 20%.

Thus, the highest rate of 20% would be apply under Section 206AA as Mauritius Bank failed to furnish its PAN to ICO. Thus, TDS of Rs 1,00,000 would be deducted on such interest payment.

NON-FURNISHING OF PAN IN FORM 15G/15H DECLARATION – SECTION 206AA(2)/ (3)

No declaration in Form 15G/15H (under Section 197A) shall be valid,unless the person furnishes his PAN in such declaration .When such declaration becomes invalid due to non-furnishing of PAN, the deductor shall deduct the tax at source as per the highest rate given u/s 206AA(1).

NON – FURNISHING OF PAN IN CERTIFICATE FOR LOWER DEDUCTION OR NIL DEDUCTION OF TDS – SECTION 206AA(4)

No certificate for lower deduction or Nil deduction of TDS (under section 197) will be granted by the Assessing Officer unless the application contains the PAN of the applicant .

NON-APPLICABILITY OF SECTION 206AA ON INTEREST PAYMENTS – SECTION 206AA(7)

The provisions of section 206AA , requiring deduction of tax at higher rate, shall not apply in respect of payment of interest to non-resident (non-corporate non-resident or foreign company)on long-term bonds (as referred to in Section 194LC ), even when the non-resident payee failed to furnish PAN to the Payor. Interest on such long-term bonds are liable to withholding tax at concessional rate of 5% when such bonds satisfy the conditions prescribed u/s 194LC .

EXAMPLE : –

ICO pays interest of Rs 2,00,000 to FCO on long-term bonds. The rate of TDS on such payment is 5% under Section 194LC. FCO does not provide its PAN to ICO. What would be the TDS amount ?

SOLUTION : –

Tax would be deducted at higher rate under Section 206AA when the payee does not provide PAN to the Payor. However, Section 206AA is not applicable on interest payment under Section 194LC. Accordingly, TDS would be deducted at 5% under Section 194LC.

NON-APPLICABILITY OF SECTION 206AA ON OTHER PAYMENTS TO NON-RESIDENTS- RULE 37BC

Section 206AA shall not be applicable in respect of following payments to non-resident , provided the conditions mentioned hereunder are satisfied : –

- Interest (other than interest on bonds u/s 194LC),

- Royalty,

- Fees for technical services and

- Payment on transfer of any capital asset .

CONDITION : –

TDS shall not be deducted at higher rate u/s 206AA in respect of aforesaid payments when non-resident payee submits prescribed information and documents

Information and documents to be submitted by non-resident to escape from rigours of Section 206AA: –

- Name, e-mail id, contact number ;

- Address in the country or specified territory outside India of which the deductee is a resident ;

- A certificate of his being resident in any country or specified territory outside India from the Government of that country or specified territory if the law of that country or specified territory provides for issuance of such certificate (Tax residency certificate) ;

- Tax Identification Number of the deductee in the country or specified territory of his Residence. In case no such number is available, then a unique number on the basis of which the deductee is identified by the Government of that country or the specified territory of which he claims to be a resident .

EXAMPLE : –

ICO has to make payment of Rs 2,00,000 to FCO (USA) for Fees for Technical services. FCO does not have PAN in India. FCO provides Tax identification Number of USA, Tax Residency Certificate of USA and its basic details. At what rate TDS would be deducted when the rate of TDS is 10% under IT Act ?

SOLUTION : –

Section 206AA which provides for higher rate of TDS when payee failed to furnish its PAN to Payor, is not applicable when the payee furnishes Tax identification number and its basic details in place of PAN. Thus, TDS would be deducted at 10% (i.e., Rs 20,000) as Section 206AA is not applicable.