MODE OF COMPUTATION OF CAPITAL GAINS – SECTION 48 OF INCOME TAX ACT

Mode of computation of capital gains means, the method that should be applied to calculate capital gains. Capital gains are normally calculated, by deducting from the sales consideration, the cost spent by the seller, in acquiring the Capital Asset or making improvements to the Capital Asset, which are capital in nature.

Capital Gains =

FULL VALUE OF SALES CONSIDERATION

Less : –

- the Cost of Acquisition of the asset or the Indexed Cost of Acquisition, i.e. purchase cost of asset, and

- the cost of any improvement of asset or the Indexed cost of any improvement [Cost of improvement is capital expenditure incurred by assessee in making any additions or improvement to the capital asset]

- Expenditure incurred wholly and exclusively in connection with transfer of the capital asset. For example, the following can be considered as expenditure incurred wholly and exclusively in connection with transfer of a capital asset : –

- Brokerage or commission paid for securing or purchase the asset

- Cost of stamp registration fees for securing the title of the asset

- Litigation expenditure , incurred for enhancement of compensation awarded in case of compulsory acquisition of the capital asset

However, it may be noted that any sum paid as securities transaction tax, shall not be allowed as deduction while computing the income chargeable under the head “Capital Gains” .

A. INDEXED COST OF ACQUISITION AND INDEXED COST OF IMPROVEMENT

Inflation is an expected phenomena in any economy. Where, a person purchases a Capital Asset, and keeps it over a longer period of time, some part of the appreciation in the value of the Capital Asset, is also due to the inflation. In order to tax only that part of appreciation, which is other than inflation, the income tax law provides that in case of a long-term capital asset, the cost of acquisition should be increased in proportion to the inflation. This would result in increase of cost of acquisition, and correspondingly result in decrease in the overall capital gain, resulting in a lower tax liability for the seller. The increase to the cost of asset, is known as indexation. Search indexation has to be based on the notified cost inflation index, which is provided every year for tax purposes. However, in the case of non-resident seller, such indexation may not be allowed in certain cases.

For computation of long term capital gains, indexed cost of acquisition shall be used instead of cost of acquisition under section 48 of income tax act .Similarly, indexed cost of any improvement shall be used instead of cost of improvement .

COMPUTATION OF INDEXED COST OF ACQUISITION

MODE I – ASSETS ACQUIRED DIRECTLY BY THE ASSESSEE HIMSELF

In cases where the Asset has been acquired by the seller himself, it would need to be ascertained whether such as it was acquired on or after 1 .4 .2001 or it was acquired before 1 .4 .2001 . The indexed cost of acquisition would be calculated as under: –

a) Asset acquired on or after 1 .4 .2001

b) Asset acquired before 1 .4 .2001

CII= Cost Inflation Index

MODE II – ASSETS ACQUIRED FROM PREVIOUS OWNER IN MODE GIVEN UNDER SECTION 49(1)

However, in cases where the Asset has been acquired by the seller from the previous owner under any mode given in Section 49(1), the indexed cost of acquisition would be calculated as under: –

is first held by the assessee

Note :-

Acquisition Mode u/s 49(1)

Where the capital asset became the property of the assessee –

- on distribution of assets on the total or partial partition of a HUF;

- under a gift or will;

- by succession, inheritance or devolution, or

- on distribution of assets on the liquidation of a company, or

- under a transfer to a revocable or an irrevocable trust, or

- On any transfer between holding company and its wholly owned subsidiary which satisfies condition of Section 47(iv) or Section 47(v).

- On any transfer in scheme of amalgamation which satisfies conditions of Section 47(vi)/(via)/(viaa)/(viab)

- On any transfer in scheme of demerger which satisfies conditions of Section 47 (vib)/(vicc)/(vic)

- On any transfer in a scheme of business re-organisation of co-operative bank which satisfies conditions of Section 47(vica)/(vicb)

- On any transfer in a scheme of conversion of private company or unlisted public company into LLP which satisfies conditions of Section 47(xiiib)

- On any transfer in a scheme of conversion of firm or sole proprietary concern into company which satisfies conditions of Section 47(xiii)/(xiv)

- Which is Hindu undivided family when one of its member has converted his self-acquired property into Joint Family Property after the 31st day of December, 1969.

COMPUTATION OF INDEXED COST OF IMPROVEMENT (COI)

MODE I – COST OF IMPROVEMENT INCURRED DIRECTLY BY THE ASSESSEE HIMSELF

In cases where the Asset has been acquired by the seller himself, it would need to be ascertained whether such as it was acquired on or after 1 .4 .2001 or it was acquired before 1 .4 .2001 . The indexed cost of improvement would be calculated as under: –

a) Improvement made on or after 1 .4 .2001

b) Improvement made before 1 .4 .2001 is not considered for computing capital gains

MODE II – IMPROVEMENT MADE BY PREVIOUS OWNER WHERE ASSET IS ACQUIRED THROUGH ANY MODE GIVEN UNDER SECTION 49(1)

However, in cases where the Asset has been acquired by the seller from the previous owner under any mode given in Section 49(1), the indexed cost of acquisition would be calculated as under: –

![]()

SPECIAL PROVISIONS FOR COMPUTING CAPITAL GAINS IN CASE OF NON-RESIDENTS

CAPITAL GAINS ARISING TO A NON-RESIDENT FROM TRANSFER OF SHARES OR DEBENTURES OF AN INDIAN COMPANY ACQUIRED IN FOREIGN CURRENCY – FIRST PROVISO TO SECTION 48 OF INCOME TAX ACT READ WITH RULE 115A

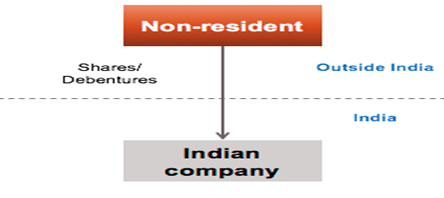

Where are non-resident acquires shares or debentures of an Indian company, by utilizing foreign exchange, and receive foreign exchange at the time of transfer of such shares or debentures, the gains/ losses, incurred by the non-resident could be divided into two parts : –

- Gains or loss arising due to fluctuation in the foreign currency;

- Gains or loss arising due to appreciation in the value of the Asset

In order to, tax only the gains or loss arising due to appreciation in the value of the Asset, there is a special mechanism provided under the income tax act for calculation of capital gains in such cases.

Accordingly, any Capital gains arising to non-resident on transfer of shares or debentures of an Indian company, shall be computed by methodology under first proviso to Section 48 of Income tax act, provided such shares or debentures were acquired by utilizing the foreign currency . It may be noted that these provisions are only applicable on the transfer of shares and debentures acquired in foreign currency. If the shares and debentures were required in Indian rupees, or any other Capital Asset is acquired, the methodology provided under first proviso to Section 48 of Income tax act shall not be applicable.

Conditions : –

- Transferor is a non-resident .

- Capital gain should arise on transfer of shares/debentures (listed or unlisted) of an Indian company.

- Shares or debentures were acquired by utilizing foreign currency

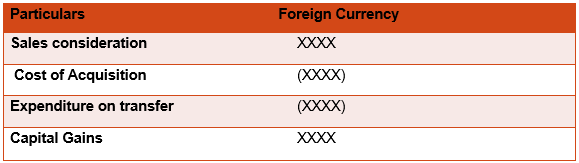

METHOD OF COMPUTING CAPITAL GAINS UNDER FIRST PROVISO TO SECTION 48 OF INCOME TAX ACT: –

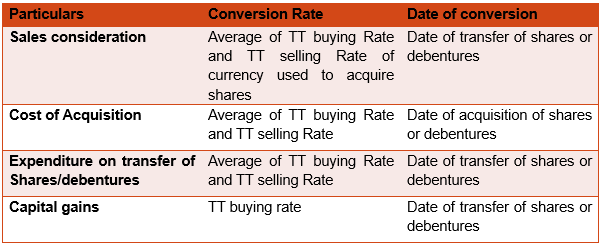

Step 1 : Convert Sales Consideration to foreign currency used to acquire shares/debentures

Divide Sales Consideration by Average Foreign Currency Rate

Step 2: Convert cost of acquisition /into foreign currency used to acquire shares/debentures

Divide Cost of Acquisition by Average Foreign Currency Rate =

Step 3: Convert expenditure incurred wholly and exclusively on transfer of shares/debentures to foreign currency used to acquire them

NOTE : –

*Average Foreign currency rate =

Telegraphic transfer buying rate (on applicable date) + Telegraphic transfer selling rate (on applicable date /2

Step 4 : – Compute Capital Gains

Step 5 : –

The capital gain computed in foreign currency under Step 4, shall be reconverted into Indian currency . Telegraphic transfer buying rate on the date of transfer shall be used to reconvert capital gains in foreign currency into Indian currency .

POINTS TO BE NOTED : –

- This method is applicable only on transfer of listed and unlisted shares or debentures . It is not applicable on transfer of bonds and units of mutual funds.

- Benefit of indexation shall not be available to non-residents under this method.

- Benefit of first proviso to Section 48 of Income tax act would not be available when long-term capital gains are taxable u/s 112A [Section 112A has been inserted by the Finance Act, 2018 in order to tax long-term capital gains on sale of equity shares or unit of equity oriented funds or business trust which were earlier exempt from tax u/s 10(38) . This provision is discussed in succeeding paras]

NOTE : –

Aforesaid manner of computing capital gains shall be applicable in respect of capital gains accruing or arising from every re-investment thereafter (i .e, capital gains accruing from sale of Indian shares/debentures which was purchased out of proceeds of Indian shares/debentures)

SUMMARY OF CONVERSION RATES , AND DATE OF CONVERSION FOR COMPUTING CAPITAL GAINS UNDER FIRST PROVISO TO SECTION 48 OF INCOME TAX ACT

MEANING OF CERTAIN TERMS

TELEGRAPHIC TRANSFER BUYING RATE : –

The rate or rates of exchange adopted by the State Bank of India for buying foreign currency having regard to the guidelines specified from time to time by the RBI for buying foreign currency where such currency, made available to that bank through a telegraphic transfer .

TELEGRAPHIC TRANSFER SELLING RATE : –

The rate of exchange adopted by the State Bank of India for selling foreign currency where such currency is made available by that bank through telegraphic transfer.

EXAMPLE :-

Alex, a non-resident purchases 50,000 shares of an Indian Company at the rate of Rs 20 per share on 30.06.2010 by utilising USD. These shares are sold @ Rs 50 per share on 31.03.2017 .The telegraphic transfer buying and selling rate of US dollars adopted by the State Bank of India on various dates is as follows:-

Compute Capital gain for the AY 2017-18 on both USD and INR on the assumption that long-term capital gains on such shares are not covered under Section 10(38)?

SOLUTION

Step 1: Convert sales consideration from INR to foreign currency

Sales Consideration

Average Foreign Currency Rate

= 50,000 X 50

50

= USD 50,000

Average Foreign currency rate on date of transfer

= 45 + 55

2

= 50

Step 2: Convert cost of acquisition from INR to foreign currency

Cost of Acquisition

Average Foreign Currency Rate

= 50,000 X 20

55

= USD 18,181.82

Average Foreign currency rate on date of purchase

= 50 + 60

2

= 55

Step 3 :- Computation of capital Gains

Step 4: Conversion of capital gains from USD to INR

Capital gains (USD38,818.18 X Rs 45) = Rs 1431818

Converted based on TTBR on the date of Sale

FULL VALUE OF CONSIDERATION IN CASE OF RUPEE DENOMINATED BONDS – SECTION 48 OF INCOME TAX ACT

Where a non-resident acquires debentures of an Indian company which are denominated in Indian rupee, by utilizing foreign exchange, and receive foreign exchange at the time of transfer of such debentures, the non-resident may earn certain gains on account of rupee appreciation against foreign currency , at the time of redemption of rupee denominated bond . This Section provides that any gains arising to non-resident on account of rupee appreciation against foreign currency at the time of redemption of rupee denominated bond of an Indian company shall not be included in computation of full value of consideration . Let us understand this with the help of an example : –

EXAMPLE : –

Alright India issued rupee denominated bonds to Alpha Inc. for Rs 20,000 which were subscribed in USD.Exchange rate at the time of acquisition was 1$=50 .Alpha paid Rs 20,000 (Equivalent to $400) to purchase rupee denominated bonds .

The company redeemed bonds at par (excluding interest) at Rs. 20,000 (The rate of exchange at that time was 1$= 40).Calculate full value of consideration under Section 48 of income tax act?

SOLUTION : –

Alpha Inc. receives (20,000/40) = USD 500. Gains of USD 100 (500-400) is due to appreciation of rupee against dollar , since the bonds have been redeemed at par, and hence such gains would not be considered while determining full value of sales consideration under Section 48 of income tax act. Thus, sales consideration would be USD 400.

ASCERTAINMENT OF COST IN SPECIFIED CIRCUMSTANCES – SECTION 49

Section 49 provides for the guidelines for computing the cost of acquisition under different circumstances including the following cases : –

- Cost of acquisition of the previous owner, is considered as the cost of acquisition of the assessee

- Cost of acquisition of shares required on the redemption of GDR

Under certain circumstances, the Cost of acquisition of the asset shall be deemed to be cost, for which the previous owner of the property acquired the asset, where capital asset became property of assessee under any of the mode of transfer described below. Any cost of improvement of the previous owner would be added to the cost of acquisition :

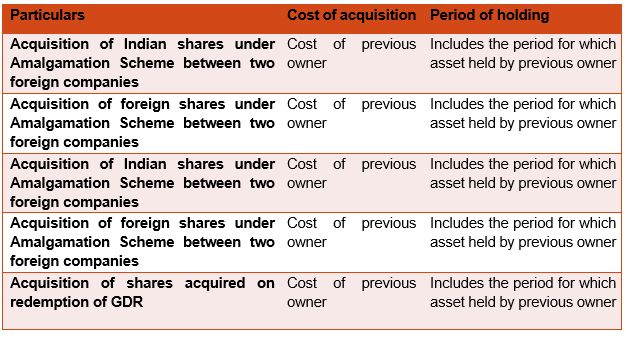

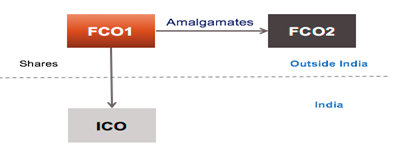

a. Acquisition of shares of Indian company under amalgamation scheme [referred to in section 47(via)]

Where the shares of an Indian company (ICO), are acquired by a foreign company (FCO 2) , in a scheme of amalgamation of two foreign company(FCO 1 amalgamates into FCO 2), the cost of acquisition of shares of Indian company (ICO) in the hands of the amalgamated company (FCO 2) shall be the cost for which such shares were acquired by the amalgamating foreign company (FCO 1), provide that conditions of Section 47(via) are satisfied.

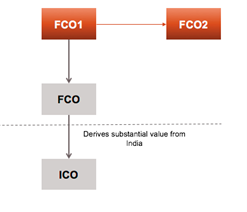

b. Acquisition of shares of foreign company under amalgamation scheme [referred to in section 47(viab)]

Where the shares of a foreign company (FCO), (which derives directly or indirectly its value substantially from the share of an Indian company), are acquired by a foreign company (FCO 2) , in a scheme of amalgamation of two foreign company(FCO 1 amalgamates into FCO 2), the cost of acquisition of shares of FCOin the hands of the amalgamated company (FCO 2) shall be the cost for which such shares were acquired by the amalgamating foreign company (FCO 1), provide that conditions of Section 47(viab) are satisfied.

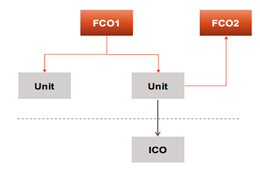

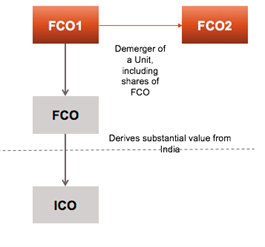

c. Acquisition of Indian shares under demerger scheme [referred to in Section 47(vic)]

Where the shares of a foreign company (FCO), (which derives directly or indirectly its value substantially from the share of an Indian company), are acquired by a foreign company (FCO 2) , in a scheme of demerger , (FCO 1 demerges a unit, which owns shares of an Indian company (ICO) into FCO 2), the cost of acquisition of shares of FCO in the hands of the resulting company (FCO 2) shall be the cost for which such shares were acquired by the demerged foreign company (FCO 1), provide that conditions of Section 47(vic) are satisfied.

d. Acquisition of shares of foreign company under scheme of demerger [referred to in section 47 (vicc)]

Where the shares of a foreign company (FCO), (which derives directly or indirectly its value substantially from the share of an Indian company), are acquired by a foreign company (FCO 2) , in a scheme of demerger for transfer of unit between two foreign company (FCO 1 demerges a unit to FCO 2), the cost of acquisition of shares of FCO in the hands of the resulting company (FCO 2) shall be the cost for which such shares were acquired by the demerged foreign company (FCO 1), provide that conditions of Section 47(vicc) are satisfied.

COST OF ACQUISITION OF SHARES ACQUIRED ON REDEMPTION OF GLOBAL DEPOSITORY RECEIPTS

The cost of acquisition of the shares acquired by a non-resident, on redemption of GDRs [referred to in section 115AC (1)(b)] would be the price of such share or shares prevailing on any recognized stock exchange on the date on which a request for such redemption was made . [Section 49(2ABB)]

Note : –

Cost of improvement borne by the previous owner will also be added in the aforesaid costs

COST OF ACQUISITION AND PERIOD OF HOLDING IN CERTAIN SPECIFIED CIRCUMSTANCES