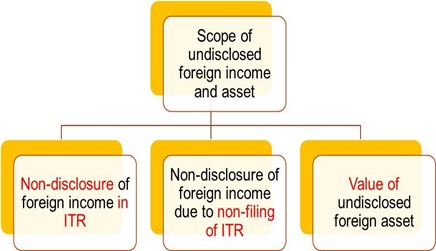

SCOPE OF TOTAL UNDISCLOSED FOREIGN INCOME AND ASSET – SECTION 4(1)

Undisclosed foreign income or undisclosed foreign asset would arise, where the assesse :-

- Files ITR, but does not discloses foreign income in ITR

- There is non-disclosure of foreign income, due to non-filing of ITR

- Does not discloses foreign asset

Thus, total undisclosed foreign income and undisclosed foreign asset shall include following incomes :-

- Income from a source located outside India (i.e., foreign income like rental income from property situated outside India) which has not been disclosed in the ITR.

Note :-

It may be noted , that this clause is applicable , where the return of income has been filed , but the foreign income has not been disclosed in such ITR. Such ITR could have been filed within the time-limit u/s 139(1) [which includes revised return] or after the due date as belated return.

Suppose, Mr. R has rental income from property situated outside India. He had filed his ITR and disclosed all India sourced income. However, he had not disclosed foreign sourced rental income in his ITR. Now such rental income would be considered as undisclosed foreign income under the provisions of the Black Money Act.

- Income from a source located outside India, when the assessee is required to file return of income u/s 139 of the Income-tax Act , but he has not filed any return [including belated return].

Note :-

In the first case, ITR is filed by the assessee but foreign income is not disclosed in such return. In this case , assessee has income from source located outside India , he is required to file return in India, but such assessee has not filed the return.

Suppose Mr. M has interest income of Rs 5 lakhs from outside India, and he also has income of Rs. 2 lakhs from India. He did not file his ITR in India. In such a case, such interest income would be considered as undisclosed foreign income of Mr. M.

- The value of undisclosed asset located outside India.

Note :-

It may happen that a resident and ordinarily resident person has a foreign assets in the form of immovable property, bullion, Jewellery, share in foreign firm, etc. However, such value has not been disclosed to income-tax authorities. In such a case, the value [i.e., fair value as per Rule 3] shall be considered as undisclosed

EXAMPLE: –

An Indian resident earns interest income of USD 9,000 (Equivalent to Rs 5,85,000) during the PY 2017-18 from money stashed in foreign bank account .

He also earns other income of Rs 6,00,000 during the PY 2017-18. He did not file his income tax return for the PY 2017-18 and the time limit for filing belated return has also expired .

In this case, the Indian resident is liable to file income-tax return as his total income is more than maximum exemption limit. Further, such interest income would be considered as undisclosed income from a source located outside India .

VARIATION MADE IN FOREIGN INCOME DURING ASSESSMENT OR REASSESSMENT- SECTION 4(2)

In certain cases, an assessee may earn certain foreign income, which has been disclosed in his ITR. Subsequently, his case is selected for scrutiny assessment. During, assessment certain additions are made by the AO to such foreign income . The question which arises is, whether, such addition to the foreign income would also be included in the undisclosed foreign income under the provisions of the Black Money Act ?

As per the provisions of Section 4(2) of the Black Money Act, any variation made (i.e., additions made) in the income from a source outside India shall not be included in the total undisclosed foreign income if such addition is made during assessment or reassessment and variation is made in accordance with the provisions of : –

- Section 29 to section 43C of the IT Act ; or

- Section 57 to section 59 of the IT Act (i.e., additions made during assessment or reassessment proceedings while computing income from other sources); or

- Section 92C of the IT Act (i.e., transfer pricing adjustment made during assessment or reassessment proceedings).

NON-INCLUSION OF UNDISCLOSED FOREIGN INCOME AND ASSET IN INCOME COMPUTED UNDER INCOME-TAX ACT- SECTION 4(3)

The Black money would be taxed in the hands of assessee under two circumstances : –

- Where the Assessing Officer has discovered the undisclosed foreign income or undisclosed foreign asset of the assesse, which is considered as black money under the provisions of the Black Money Act.

- The assessee has voluntarily included his undisclosed foreign income or fair market value of undisclosed foreign asset in his ITR.

In both the aforesaid cases, such black money would be taxed under the provisions of the Black Money Act. Once such amount is considered under the Black Money Act, it shall not be included again in the total income of the assesse under the Income-Tax Act.

EXAMPLE : –

Kalu Singh, an Indian resident had USD 10,000 in foreign bank account on which he earned interest of USD 500. Such bank account was discovered by AO during the PY 2017-18 and it has been taxed as undisclosed foreign asset and interest as undisclosed foreign income under the Black Money Act . Such interest shall not be considered while computing income of Indian resident under the Income-Tax Act .