NO ADVANCE RULING CASES

- Question is pending before other authorities.

- Question involves determination of fair market value of any property.

- Transaction is designed prima facie for tax avoidance

- Quantification of income

- Determination of arm’s length price.

QUESTION IS PENDING BEFORE OTHER AUTHORITIES

In case the question raised in the application is already pending before any income-tax authority, tribunal or any court, the Authority cannot allow application.

For e.g. a notice for initiation of assessment proceedings may be regarded as pendency of proceedings and may create an application invalid before AAR.

QUESTION INVOLVES DETERMINATION OF FAIR MARKET VALUE OF ANY PROPERTY

The second prohibition is on questions relating to the determination of fair market value of any property, movable or immovable.

TRANSACTION IS DESIGNED PRIMA FACIE FOR TAX AVOIDANCE

The application would not succeed if it relates to a transaction which is designed prima facie for the avoidance of income-tax.

WHAT CAN BE SAID TO BE PRIMA FACIE AVOIDANCE OF INCOME-TAX?

Only the prima facie impression created in the mind of the Authority on the facts stated before it that transaction is undertaken to avoid income tax is sufficient cause for rejecting the application.

It is not necessary to refer the detailed facts of the case to determine whether a particular transaction is designed to avoid income tax.

OTHER CASES

Questions cannot be raised with respect to quantification of income of a taxpayer and for determination of arm’s length price under Indian Transfer Pricing regulations.

APPLICATION FOR ADVANCE RULINGS

- Application for advance ruling should be in prescribed form and manner stating the question on which the advance ruling is sought

- Applicant can withdraw his application within 30 days of the date of application

APPLICATION FOR ADVANCE RULINGS

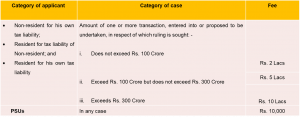

Application shall be in quadruplicate and accompanied by following fees:–

PROCEDURE

Step I: AAR shall forward a copy of application to Commissioner to ascertain whether the case is pending or not, and if necessary call for the records.

Step II: AAR may allow or reject the application. In case application is rejected following points are worth noted: –

- Before rejecting the application, an opportunity of being heard shall be given to the applicant.

- Reason for rejection shall be given in the order.

- Copy of order shall be sent to the applicant and to the CIT.

- No appeal is possible against order of rejection

Step III: After allowing application and examining the information placed before it, AAR pronounces its Advance Ruling on the question specified in the application.

Step IV: On request of applicant before pronouncing its Advance Ruling, AAR shall provide an opportunity of being heard either in person or through a authorized representative.

Step V: AAR shall pronounce its Advance ruling in writing within 6 months from the date of receipt of application.

Step VI: A copy of the Advance Ruling pronounced by AAR shall be sent to applicant and to the Commissioner.

OTHER POINTS

- On occurrence of vacancy in the office of the chairman by reason of his death, resignation or otherwise, the senior most Vice-Chairman shall act as the Chairman until new chairman enters upon his office to fill such vacancy in accordance with provisions of the Act.

- In case Chairman is unable to discharge his functions owing to absence, illness or any other reason, the senior most Vice-Chairman shall discharge the functions of chairman until the chairman resumes his duties.

- On the account of vacancy or defect in the constitution of authority, no advance ruling or proceedings shall be questioned or shall be treated invalid.

- No income tax authority or ITAT shall proceed to decide any issues in respect of which an application has been made by the Applicant.

- The advance ruling pronounced by Authority is binding on

- The applicant who had sought it in respect of the transaction in relation to which the ruling had been sought; and

- On the Commissioner and authorities subordinate to him.

- Where the AAR finds that Advance Ruling sought by applicant by fraud or misrepresentation of facts, then it may by order declare such ruling to be void-ab-initio and all the provisions of the Act shall apply as if such advance ruling has never been made.

- The order of AAR giving its opinion is a final order and no appeal is possible against such an order.