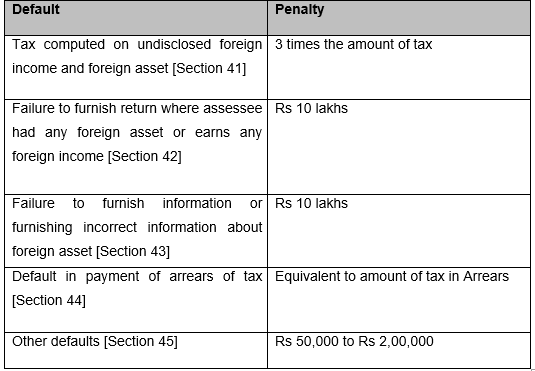

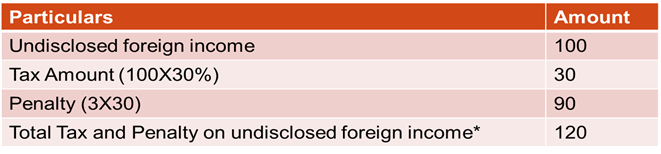

PENALTY IN RELATION TO UNDISCLOSED FOREIGN INCOME AND ASSET – SECTION 41

The Assessing Officer may levy penalty where tax has been computed in respect of undisclosed foreign income and undisclosed foreign asset. The amount of penalty, shall be equal to three times the tax so computed, in addition to tax.

EXAMPLE : –

PENALTY FOR FAILURE TO FURNISH RETURN FOR FOREIGN INCOME AND ASSET – SECTION 42

Failure to furnish return of income u/s 139(1) by a person, being a resident and ordinarily resident in India would invite penalty of Rs 10 lakhs, if such person –

- Has held any asset located outside India (including financial interest in any entity like interest / shareholding of a person in foreign firm or company etc.).

- Was a beneficiary of any asset located outside India; or

- Had any income from a source located outside India.

PENALTY FOR FAILURE TO FURNISH INFORMATION OF FOREIGN ASSET OR FOREIGN INCOME IN RETURN OF INCOME – SECTION 43

Where a person, who is a resident and ordinarily resident in India in India , fails to furnish any information or furnishes inaccurate particulars in return of income relating to any foreign asset, such person would be liable to penalty of Rs 10 lakhs. Such foreign asset, may be held by such person as a beneficial owner or otherwise, and would also include financial interest in any entity located outside India.

Similar penalty would be levied when there is failure to furnish any information or furnishing of inaccurate particulars in return of income, relating to income from a source located outside India.

Note :-

Penalty shall not be levied if aforesaid failure is in respect of foreign bank accounts having an aggregate balance of Rs. 5 lakh or less at any time during the previous year.

DETERMINATION OF VALUE OF FOREIGN BANK ACCOUNT IN INR – EXPLANATION TO SECTION 42

We have already discussed the valuation mechanism of foreign bank account in detail. However, for determining the value in INR of the balance in an foreign bank account, the rate of exchange shall be the telegraphic transfer buying rate of such foreign currency as on the date for which the value is to be determined, as adopted by the State Bank of India constituted under the SBI Act, 1955 .

PENALTY FOR DEFAULT IN PAYMENT OF TAX ARREAR -SECTIONS 44

Where an assessee has defaulted in payment of tax under the Black Money Act, he would be liable for penalty which , would be equivalent to the amount of tax arrears in case of an assessee in default, or an assessee deemed to be in default in making payment of tax.

Such penalty would also be levied in case of continuing default by such assesse and is in addition to the penalty prescribed under any other provisions of the Black Money Act.

Where the assessee has defaulted in payment of tax, but has paid all the taxes before the penalty is actually levied, the assessee cannot ask for non-imposition of penalty merely by reason of the fact that before levy of such penalty, tax has been paid by him. Even in such a case, penalty shall also be levied .

PENALTY FOR OTHER DEFAULTS – SECTION 45

Under this Section, penalty of Rs. 50,000 to Rs. 2 lakh would be attracted where a person liable to penalty has, without reasonable cause , has committed –

- Failed to answer any question of a tax authority;

- Failed to sign any statement made by him in the course of any proceedings under the Act which a tax authority may legally require him to sign,

- Failed to attend or produce books of account or documents at the place or time, in response to summons issued u/s 8 .

PROCEDURE FOR IMPOSING PENALTY – SECTION 46

The procedure for imposing penalty under the Black Money Act is as under : –

Show-cause notice : –

For the purpose of imposing penalty, the tax authority shall issue a notice to an assessee, requiring him to show cause why the penalty should not be imposed on him.

1. Time-limit for issuing show-cause notice : –

The show cause notice (SCN) shall be issued –

- During the pendency of any proceedings under the Black Money Act, in respect of penalty referred to in Section 41, which prescribes penalty equivalent to 300% of tax on undisclosed foreign income and asset.

- Within a period of 3 years from the end of the financial year in which the default is committed, in respect of penalties referred to in section 45, which prescribes penalty for other defaults.

2. Opportunity of being heard : –

An order imposing a penalty shall be made only after giving the assessee an opportunity of being heard.

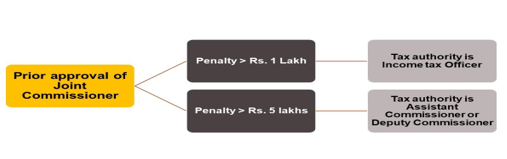

3. Prior approval : –

An order imposing a penalty shall be made with the approval of the Joint Commissioner or the Joint Director , if –

- the amount of penalty is more than Rs. 1 lakh and the tax authority levying the penalty is in the rank of Income-tax Officer; or

- The amount of penalty is more than Rs. 5 lakhs and the tax authority levying the penalty is in the rank of Assistant Commissioner or Deputy Commissioner or Assistant Director or Deputy Director

BAR OF LIMITATION FOR IMPOSING PENALTY – SECTION 47

1. Time-limit for passing order imposing penalty : –

A penalty order cannot be passed after expiry of 1 year from the end of the financial year, in which the notice for imposition of penalty is issued under section 46 (i.e., show cause notice under Section 46). For example, if the notice for imposition of penalty is issued on November 30, 2017, the penalty order cannot be passed after March 31, 2019.

2. REVISION OR REVIVAL OF ORDER IMPOSING PENALTY : –

The penalty under the Black Money Act may be levied at the initial stage when assessment is made by the Assessing Officer. In such a case, if such order of AO is challenged before higher authorities like Commissioner (Appeals) or Tribunal or High Court or Supreme Court or such order is revised u/s 23 and 24 of the Black Money Act, then any variation made by the higher authority in the order of the Assessing Officer, shall require revision of the penalty order.

Thus, an order (which imposes, or drops penalty) may be revised, or revived on the basis of assessment of the undisclosed foreign income and undisclosed foreign asset, after giving effect to the order of higher tax authority or order of revision under section 23 or section 24.

3. TIME-LIMIT FOR REVISION OR REVIVAL OF PENALTY ORDER : –

An order revising or reviving the penalty cannot be passed after the expiry of six months from the end of the month –

- in which order of the Commissioner (Appeals), the Appellate Tribunal, the High Court or the Supreme Court is received by the Principal Chief Commissioner or the Chief Commissioner or the Principal Commissioner or the Commissioner ; or

- the order of revision under section 23 or section 24 is passed .

For example, if the Commissioner (Appeals) or High Court or Tribunal has passed the order and made substantial changes in the order of Assessing Officer on June 15, 2017, an order for revision of penalty cannot be passed after December 31, 2017.

4. Period to be excluded while computing the period of limitation : –

In computing the period of limitation for imposition of penalty, the following time or period shall not be included –

- time taken in giving an opportunity of being heard to the assessee under section 7 (in case of change in tax authority); and

- the period during which a proceeding for the levy of penalty is stayed by an order, or injunction, of any court.

SUMMARY OF PENALTY PROVISIONS