Deemed International Transaction in Transfer Pricing [Section 92B] (2)

A transaction shall be treated as deemed international transaction entered into between two AEs, even though the transaction was entered into by an enterprise with a person other than an Associated enterprise (i.e., independent third-party), provided:

- there exists a prior agreement in relation to the relevant transaction between the independent third party and the AE; or

- the terms of the relevant transaction are determined in substance between the independent third party and the AE.

Facts:

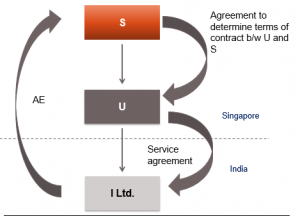

- I Ltd. of India and S International of Singapore are AE.

- I Ltd. and U International enter into an agreement for the provision of services by U International (Non-AE of I Ltd.).

- Terms of the agreement between I Ltd. and U International will be governed by prior agreement between S International and U.

Issue:

- Whether the transaction between I Ltd. and U International would be treated as deemed international transaction?

EXAMPLE 2 : –

- In the above example, if the nature and purpose of the transaction between I Ltd. and U International is entirely different from what was contemplated in the prior agreement between S and U Ltd., whether the transaction between I Ltd. and U International would be treated as deemed international transaction?

SOLUTION : –

- The transaction between I Ltd. and U International cannot be treated as deemed international transaction, as the nature and purpose of the relevant transaction are completely different from what was contemplated in the prior agreement between U Ltd. and S International.

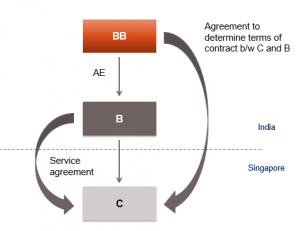

Facts:

- BB Ltd. and B Ltd. of India are AE. BB Ltd. entered into an agreement with C international (non AE) to determine the terms of provision of services between C International and B Ltd.

- B Ltd. and C International enter into a service agreement for provision of services.

Issue:

- Whether the transaction between B Ltd. and C International would be treated as deemed international transaction?

Solution:

- For an international transaction, one of the AE should be non-resident. In this case neither B Ltd. nor BB Ltd. is non-resident. Hence, the transaction between B Ltd. and C International cannot be treated as deemed international transaction.

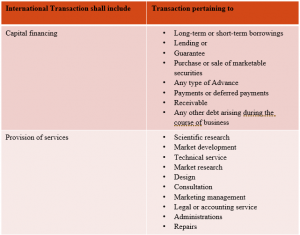

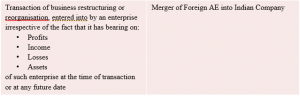

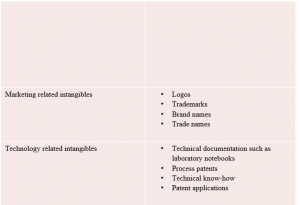

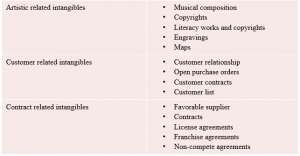

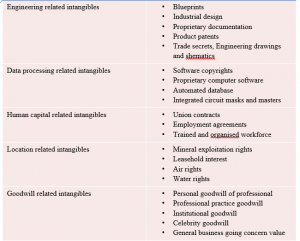

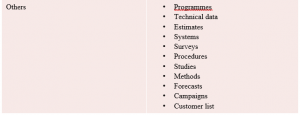

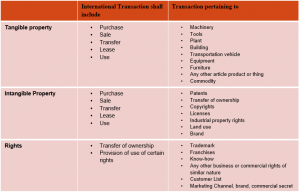

EXPLANATION TO SECTION 92B – INTERNATIONAL TRANSACTION

The definition of the term ‘international transaction’ also includes several other items including tangible/ intangible property.

![]()