CA Final Non Resident Taxation Case Studies on International Taxation by CA Arinjay Jain Sir for November 2020, which help to practice questions related to CA Final International Taxation Elective Paper 6C.

International Taxation Case Study 1 – Non Resident Taxation – Interest paid by a Foreign Bank Branch to overseas HO and other Branch

LLM Bank Ltd. carrying on banking business is incorporated in Melbourne, Australia. It has branches in different countries including India. During financial year 2018-19, the Indian branch of the bank paid interest of ₹ 20 lakhs and ₹ 15 lakhs, respectively, to its head office in Melbourne, and to the branch office in California. State with reasons whether interest so paid shall be liable to tax in India in the hands of head office and California branch ?

Solution:-

As per Explanation to Section 9(1)(v) of the IT Act, interest payable by Indian PE of foreign bank would be deemed to accrue or arise in India if recipient is : –

a) Head office of bank located outside India; or

b) PE of bank located outside India; or

c) Any other branch outside India.

In this case, the Indian branch, being a fixed place of business, shall be treated as the PE of LLM Bank Ltd. in India

Accordingly, interest of Rs 20 lakhs paid by Indian branch of LLM Bank [‘being PE of foreign bank LLM] to its head office in Melbourne, and Rs. 15 lakhs paid to the other branch office in California shall be deemed to accrue or arise in India. Accordingly, such interest income shall be taxable in the hands of Head office and California branch, respectively, in addition to any income attributable to the PE in India.

International Taxation Case Study 2 – Non Resident Taxation – Deduction of TDS on FTS

As per agreement between S Limited, a company incorporated in Korea and Bharti Motors Limited, an Indian company, S limited rendered both off-shore and on-shore technical services to Bharti Motors Limited for setting up a car manufacturing plant in Gujarat. S Limited rendered off-shore services and on-shore services at a fee of Rs 2 crore and Rs 3 crore, respectively. S Limited claims that it is not liable to tax in India in respect of fee of Rs 2 crore as it is for rendering services outside India. Is the view taken by S Limited correct ?

Solution:-

Accordingly, FTS, against services rendered outside India shall also be deemed to accrue or arise in India where such services are utilized for the purpose of business or profession in India irrespective of the fact that services are rendered outside India .

In this case, the foreign company has rendered technical services to Bharti Motors for setting up a Car manufacturing plant in Gujarat. Thus, such services are utilized for purpose of business of Bharti Motors in India . Accordingly, service fee of Rs 2 crore shall be deemed to accrue or arise in India and includible in the total income of JJ Ltd.

Thus, S Ltd. is not correct in holding that it is not liable to tax in India for fee of Rs 2 crores as it is rendering services outside India . This position shall be subject to the beneficial provision of the Treaty between India and Korea

International Taxation Case Study 3 – Non Resident Taxation – NRI returing to India and continuing to have overseas income

Peeyush, a Non-Resident Indian returned to India on 12th June, 2018 for permanently residing in India after a stay of about 20 years in U.K., provides the sources of his various income and seeks your opinion to know about his liability to income tax thereon in India in assessment year 2019-20 : –

i.Income of rent of the flat in London which was deposited in a bank there. The flat was given on rent by him after his return to India since July, 2018.

ii.Dividends on the shares of three German Companies which are being collected in a bank account in London. He proposes to keep the dividend on shares in London with the permission of the Reserve Bank of India.

iii.He has got two sons, one of whom is of 12 years. Both his sons are staying in London and not returning to India with him. Each of his sons is having income of ₹ 75,000 in U.K. (not received in India) and of ₹ 20,000 in India.

iv.During the preceding accounting year when he was a non-resident, he had sold 1000 shares which were acquired by him in British Pound Sterling and the sale proceeds were repatriated. The profit in terms of British Pound Sterling on sale of these 1000 shares was 175% of the cost at ₹ 37,500 while in terms of Indian Rupee it was ₹ 50,000.

Solution

As per Section 6(1), an individual is said to be resident in India in any previous year, if he satisfies any one of the following basic conditions : –

a)He has been in India during the previous year for a total period of 182 days or more; or

b) He has been in India during the 4 years immediately preceding the previous year for total period of 365 days or more and has been in India for at least 60 days in the previous year .

During the P.Y.2018-19, Peeyush’s stays in India is for more than 182 days, thus, he would treated as resident in India for the A.Y.2019-20.

A person is said to be RESIDENT AND ORDINARILY RESIDENT if he satisfies both the additional conditions specified under section 6(6).

ADDITIONAL CONDITIONS : –

CONDITION I : – Individual has been resident in India in 2 out of 10 previous years immediately

preceding the relevant previous year.

CONDITION II : – Individual has during the 7 previous years preceding the relevant previous year been in India for a period of 730 days or more.

However, in the present case, Peeyush never came to India in last 20 years and accordingly, he was a non-resident in nine out of ten previous years preceding P.Y.2018-19 , and his stay in India during the seven previous years is less than 730 days. Thus, he is Resident but Not Ordinarily Resident .

As per section 5(1), an assessee who is resident but not ordinarily resident would be liable pay tax only on income received / deemed to be received in India , accruing or arising / deem to accrue or arise in India . He is not liable to pay tax on income which accrues or arises outside India, unless it is derived from a business controlled in, or a profession set up in, India.

i. In this case, Flat was situated outside India and further, rental income is also not received in India . Thus, such rental income is accrued / received outside India. Accordingly, rental income shall not be included in the income of Peeyush .

ii. In this case, dividend is also collected (received) in a bank account in London. As, such dividend income is accrued and received outside India and it shall not be included in the income of Peeyush

iii. As per section 64(1A), income accruing or arising to a minor child shall be clubbed in income of parent and further, an exemption of Rs 1,500 per child shall also be allowed under section 10(32).

Accordingly, income of Rs 20,000 of his minor son shall be included in the income of Peeyush. However, a deduction of Rs 1,500 shall also be allowed to him.

Further, income of Rs 75,000 accruing to the minor child outside India and which is also received outside India shall not be included in the income of Peeyush. As his other son is a major son his income shall not be included in the income of Peeyush.

iv. Capital gains from sale of shares would be taxable in the year in which such shares are sold . At the time of sale of shares, Peeyush was non-resident, and accordingly, such gains shall not be taxable in India in that year . No taxability would arise in current FY 2018-19 due to repatriation of sale proceeds when shares were sold in preceding years .

International Taxation Case Study 4 – Non Resident Taxation – Taxation of Non-resident sportsperson

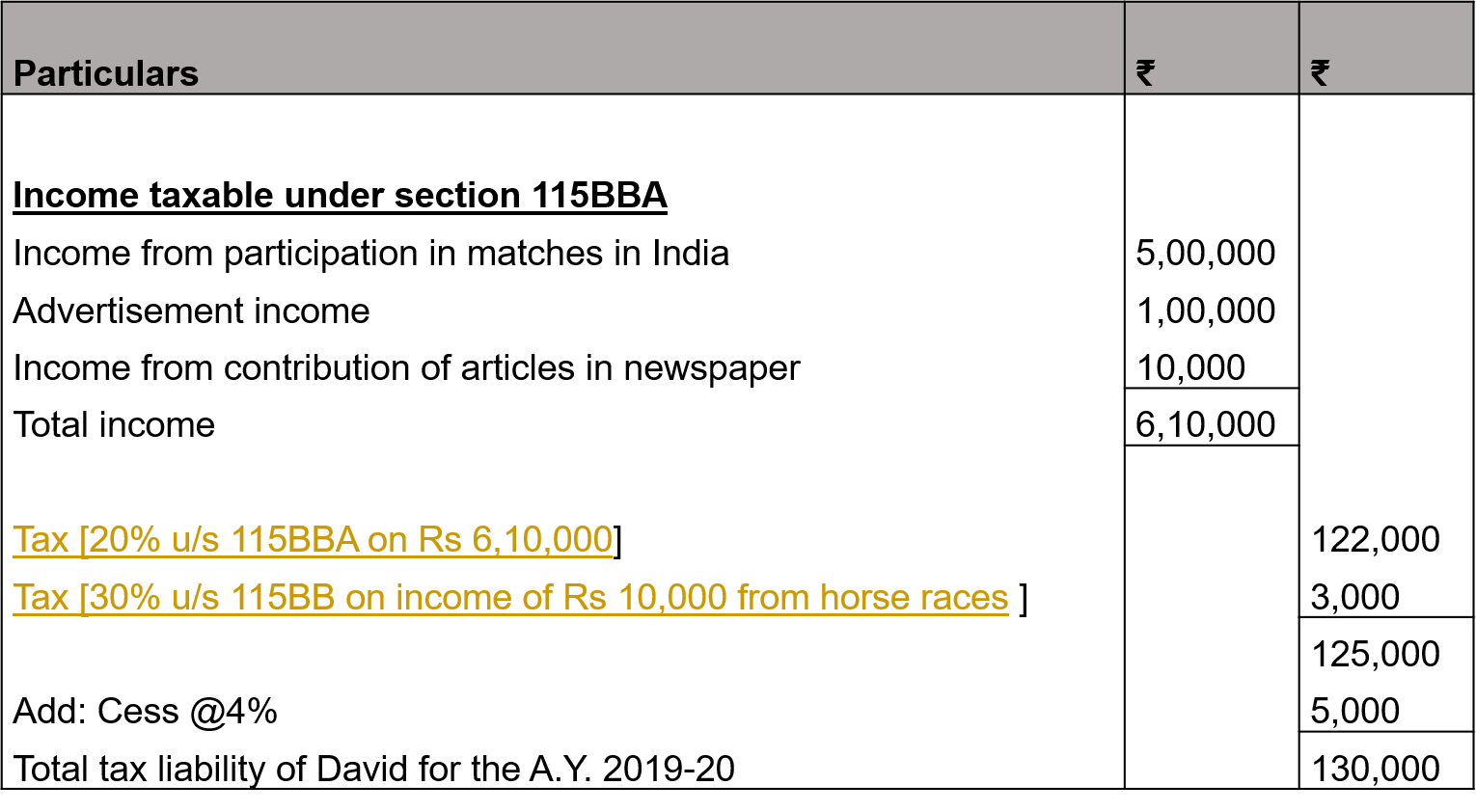

David, a foreign national and a cricketer came to India as a member of Australian cricket team in the year ended 31st March, 2019. He received ₹ 5 lakhs for participation in matches in India. He also received ₹ 1 lakh for an advertisement of a product on TV. He contributed articles in a newspaper for which he received ₹ 10,000. When he stayed in India, he also won a prize of ₹ 10,000 from horse racing in Mumbai. He has no other income in India during the year.

i. Compute tax liability of David for Assessment Year 2019-20.

ii. Are the income specified above subject to deduction of tax at source ?

iii. Is he liable to file his return of income for Assessment Year 2019-20?

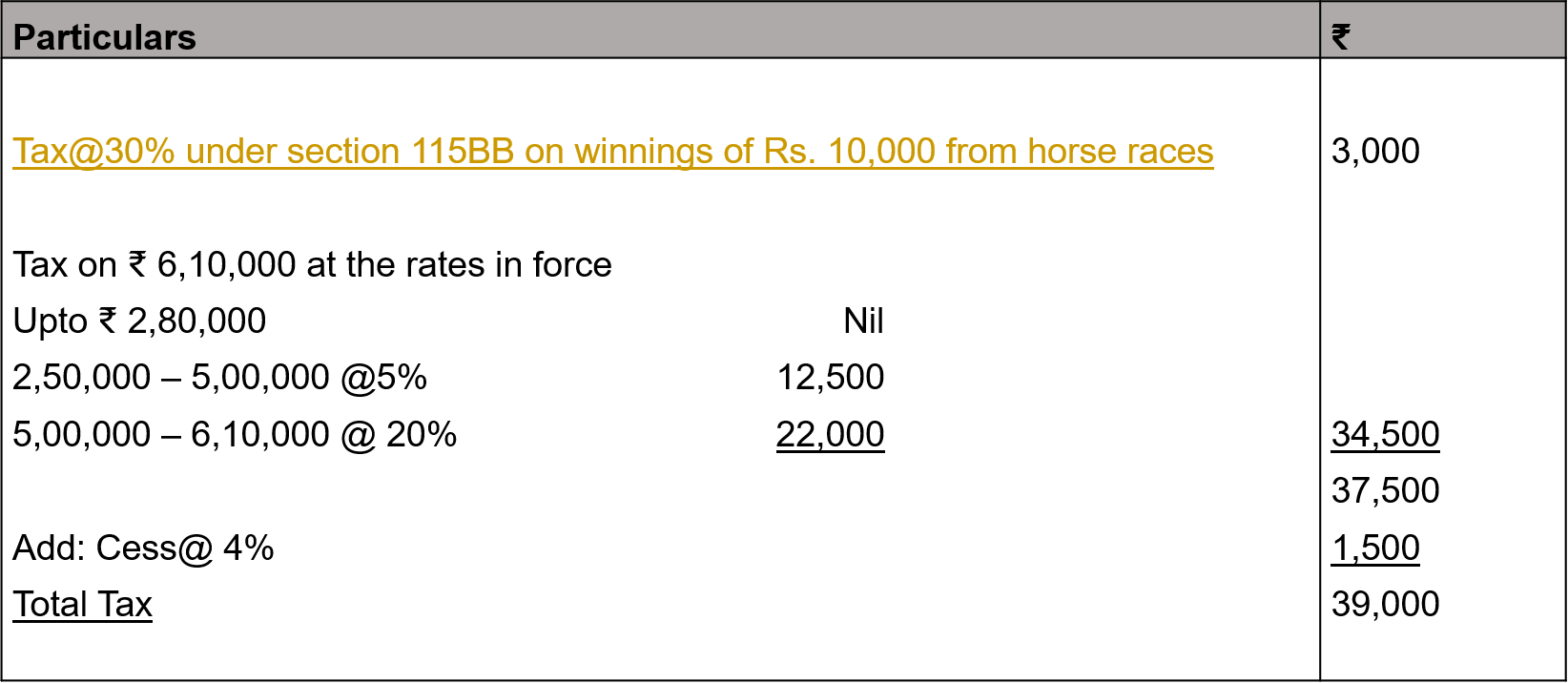

iv. What would have been his tax liability, had he been a match referee instead of a cricketer?

As per section 115BBA, following incomes of non-resident sportsman (including an athlete), who is a foreign citizen are taxable at 20%:

- Income from participation in India in any game (other than winnings from crossword puzzles, races including horse races, etc. u/s 115BB) or sport; or

- Income from advertisement; or

- Income from contribution of articles relating to any game or sport in India in newspapers, magazines or journals.

Computation of tax liability of David for the A.Y.2019-20

ii)Yes, aforesaid income would be subject to withholding tax. Section 194E provides for deduction of tax at source @ 20% in respect of any income referred to in section 115BBA payable to a non-r resident sportsman (including an athlete) or an entertainer or non-resident sports association. However, in respect of winning from lotteries, horse races, etc., TDS shall be deducted u/s 194BB @ 30%. Accordingly, income of David of Rs 6,10,000 would be subject to withholding tax @ 20% and his income from horse race shall be subject to withholding tax @ 30% u/s 194BB. Such withholding tax under section 194E and under section 194BB shall be increased by a cess of 4%.

iii) As per section 115G, it shall not be necessary for a non-resident Indian to furnish a return of his income u/s 139(1) if —

- his total income consisted only of investment income or income by way of long-term capital gains or both; and

- the tax deductible at source has been deducted from such income.

However, in this case, Mr. David has earned income from horse races as well. Therefore, he cannot avail the benefit of such exemption from filing of return of income. Accordingly, Mr. David shall be required to file his return of income for A.Y.2019-20.

(iv) In case of Indcom v. CIT (TDS) (2011) 335 ITR 485, the Calcutta High Court has held that ,payments made to umpires or match referees do not come within purview of section 115BBA because umpires and match referee are neither sportsmen (including an athlete) nor are they non-resident sports association or institution so as to attract provisions contained in section 115BBA and, therefore, liability to deduct tax at source under section 194E does not arise.

Thus, on the basis of aforesaid ruling, we can conclude that payment to non-resident match referee are not covered under section 194E, thus, they shall be subject to the normal rates of tax .

Computation of tax liability when Mr. David is a match referee for AY 2019-20

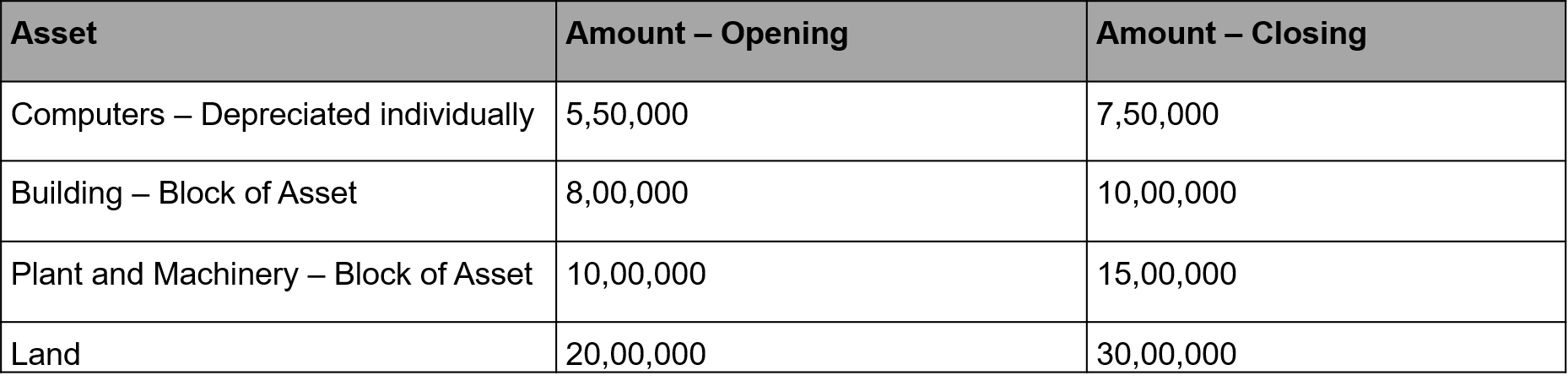

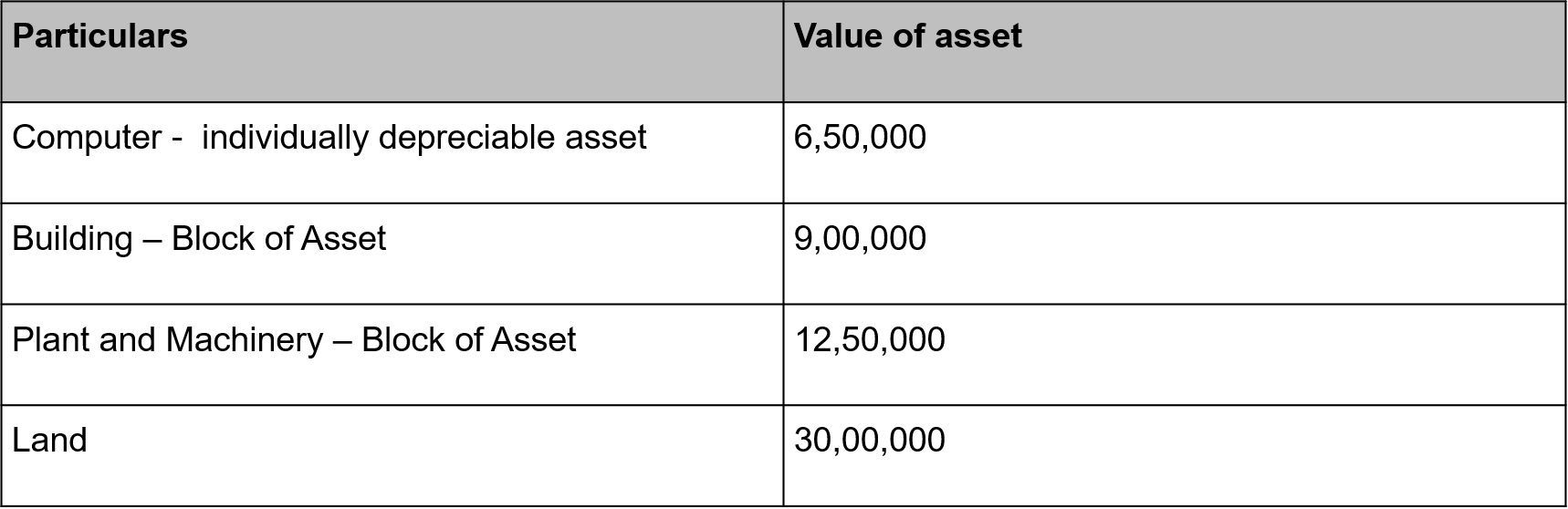

A company shall be said to be engaged in ‘Active Business Outside India’ for the purpose of POEM, if amongst other conditions, less than 50% of its total asset are situated in India. From the following Balance Sheet, compute the value of the asset : –

50% of the Plant and Machinery were purchased on the last date of the FY and depreciation has been claimed thereon assuming they were used for less than 180 days ?

Solution :-

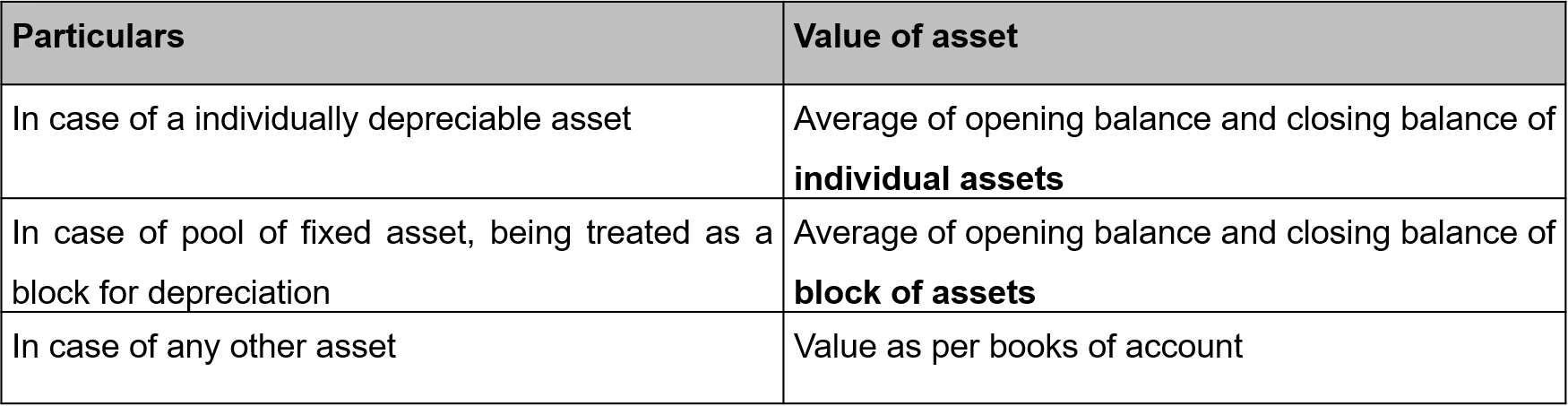

The value of the assets , for the purpose of test of POEM for different categories of asset has to be calculated as under : –

In view of the above provisions, the value is calculated as under : –

International Taxation Case Study 5 – Non Resident Taxation – Power to hold that POEM of Non resident is in India

XYZ BV, a company based out of Netherlands, executed certain infrastructure projects in India from 2014 – 2019. It had been filing its income tax return as a non-resident, due to which the beneficial provision of the Treaty results in payment of Nil tax by XYZ BV. The Assessing Officer having jurisdiction over XYZ BV came to know on 30.3.2019 , that all the projects of XYZ BV were ending on 31.3.2019, but was of the opinion that XYZ BV had a place of effective management in India. AO accordingly issued notice to XYZ BV on 30.3.2019, asking it to show Cause as to why it should not be treated as a Tax resident of India, given that its POEM is in India. When would such a notice be a valid notice ?

Solution:

In order to ensure that the POEM provisions are not misused by the tax office, and are not applied in each and every case, the AO shall, seek prior approval of Principal Commissioner or Commissioner before initiating any proceedings for holding a foreign company as resident in India on the basis of its POEM.

In the present case, if the AO has not obtained prior approval, the issue of notice would be invalid.

International Taxation Case Study 6 – Non Resident Taxation – Salary earned in India and Article 15 short stay exemption

Joseph Clarke, an Australian resident, worked in India on a construction Project, which constituted a PE of the employer in India. For the India work where he was present for 160 days and he earned a taxable salary of Rs. 24,00,000. Based on the following provision of India Australia Treaty, examine the taxability of salary earned by him under all options, if more than one ? Also examine, if TDS has to be withheld on such salary payment ?

ARTICLE 15

DEPENDENT PERSONAL SERVICES

- Subject to the provisions of Articles 16, 17, 18, 19 and 20, salaries, wages and other similar remuneration derived by an individual who is a resident of one of the Contracting States in respect of an employment shall be taxable only in that State unless the employment is exercised in the other Contracting State. If the employment is so exercised, such remuneration as is derived from that exercise may be taxed in that other State.

- Notwithstanding the provisions of paragraph (1), remuneration derived by an individual who is a resident of one of the Contracting States in respect of an employment exercised in the other Contracting State shall be taxable only in the first-mentioned State if :

a)the recipient is present in that other State for a period or periods not exceeding in the aggregate 183 days in a year of income of that other State;

b)the remuneration is paid by, or on behalf of, an employer who is not a resident of that other State; and

c)the remuneration is not deductible in determining taxable profits of a permanent establishment or a fixed base which the employer has in that other State. - Notwithstanding, the preceding provisions of this Article, remuneration in respect of an employment exercised aboard a ship or aircraft operated in international traffic by a resident of one of the Contracting States may be taxed in that State.

Section 9(1)(ii) of the IT Act, provides that if a non-resident individual has certain income , which is taxable under the head “Salaries”, it shall be deemed to accrue or arise in India, if it is earned in India.

Salary income would be treated as earned in India if it is payable for services rendered in India. Thus , salary earned by Joseph Clarke would be liable to tax in India as per the IT Act . However, given that he is a resident of Australia, he can opt to be governed by the provisions of India- Australia treaty, in case they are more beneficial .

Article 15(1) provides that India would have the right to tax the salary income if the employment is exercised in India. However, this Rule is subject to the exception, provided in Article 15(2), which provides that the salary income would be taxable only in Australia if the following conditions are satisfied : –

– the recipient is present in India for a period or periods not exceeding in the aggregate 183 days in a year of income of that other State – This condition is satisfied as he is in India for 160 days

– the remuneration is paid by, or on behalf of, an employer who is not a resident of that other State – This condition is satisfied as Payor is a non-resident ; and

– the remuneration is not deductible in determining taxable profits of a permanent establishment or a fixed base which the employer has in that other State.

In the present case, while condition 1 and 2 are clearly satisfied , we do not know whether the PE of the employer has claimed a deduction in respect of such salary. Therefore the following two situations may arise : –

–PE of the employer has claimed a deduction in respect of such salary

The income will be taxable in India, since all the conditions to claim the exemption has not been satisfied. In view of this, TDS has to be withheld on such salary payment

– PE of the employer has not claimed a deduction in respect of such salary

The income will be taxable only in Australia. Since the income is not taxable in India, no TDS has to be withheld from such salary payment

International Taxation Case Study 7 – Non Resident Taxation – Company engaged in operations of Aircraft

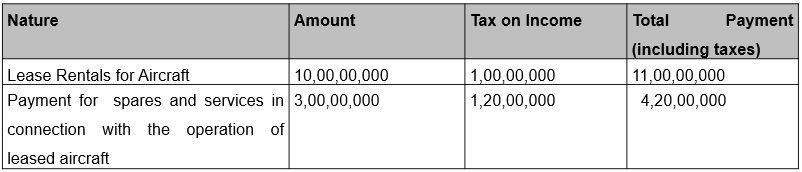

GetSetGo Airways is engaged in operation of aircraft and leased certain aircraft from Goeing UK. During the year, the various payment made by GetSetGo Airways to Goeing UK, were as under : –

Compute the exemption u/s 10, if any , assuming both the agreement were entered into on 31-3-2007 and approved by the Indian Government?

Tax paid by an Indian concern, which is engaged in operation of aircraft , for payment of lease charges/rental for an aircraft or engine of aircraft , to foreign Government or foreign enterprise shall be exempt from tax u/s 10(6BB). However, payment for providing spares or services in connection with the operation of leased aircraft or engine of aircraft , to foreign Government or foreign enterprise are not exempt from tax.

In view of this, tax of Rs. 1,00,00,000 for lease Rentals for Aircraft shall be exempt in the hands of Goeing UK, while tax of Rs. 1,20,00,000 on Payment for spares and services in connection with the operation of leased aircraft shall not be exempt in the hands of Goeing UK .

International Taxation Case Study 8 – Non Resident Taxation – Corporate restructuring overseas

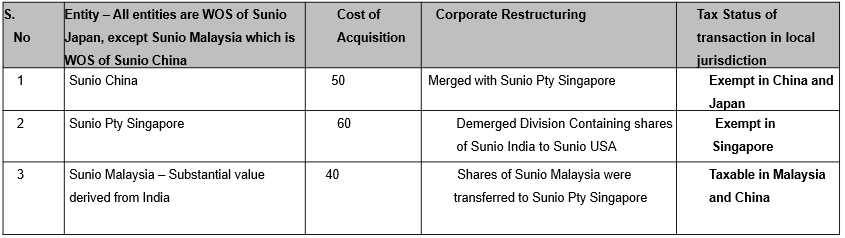

Sunio Japan, is a global company, which has subsidiaries in various countries. Five of its subsidiaries , hold 100% share capital of Sunio India, which were acquired by them at various cost over the years. The group undertook Corporate restructurings in FY 2018-19, wherein certain group reorganizations were carried out. The relevant details are as under (all amounts are in Rs. Crores) : –

Examine the tax implications in above Corporate Restructuring, from an India Tax Perspective ?

a) Merger of Sunio China , which is holding shares of Sunio India, with Sunio Pty Singapore, results in transfer of shares of an Indian company. Such transfer of shares shall not be regarded as transfer and would be exempt from tax , as the following conditions are satisfied : –

- At least 25 percent of the shareholders of Sunio China continue to remain shareholders of Sunio Pty Singapore (both are WOS of Sunio Japan) ;

- Such transfer should not attract capital gains in the country in which Sunio China is incorporated (given).

b) Where Sunio Pty Singapore , demerged division containing shares of Sunio India to Sunio USA, it would be covered u/s 47(vic) which provides that any transfer of shares of Indian company (ICO), in a demerger, by the demerged foreign company (Sunio Pty Singapore) to the resulting foreign company (Sunio USA) shall not be regarded as transfer if following conditions are satisfied –

- Shareholders holding at least 3/4 of the shares (in value) of the demerged foreign company (Sunio Pty Singapore) continue to remain shareholders of the resulting foreign company (Sunio USA) – (both are WOS of Sunio Japan);

- Such transfer does not attract tax on capital gains in the country, in which the demerged foreign company (Sunio Pty Singapore) is incorporated (given) . Accordingly, such transfer of shares shall not be regarded as transfer and would be exempt from tax.

c.Transfer of shares of Sunio Malaysia , which is a subsidiary of Sunio China, to Sunio Pty Singapore in scheme of merger would result in transfer of shares of Sunio India held by Sunio Malaysia. Section 47(viab) provides that any transfer, of a capital asset, being share of a foreign company (referred to in Explanation 5 to section 9(1)(i)), which derives, directly or indirectly, its value substantially from the share or shares of an Indian company, which are held by the amalgamating foreign company (Sunio China ), to the amalgamated foreign company (Sunio Pty Singapore ) in a scheme of amalgamation, shall not be regarded as transfer, provided the following conditions are satisfied : –

- At least 25 percent of the shareholders of the amalgamating foreign (Sunio China) company must continue to remain shareholders of the amalgamated foreign company (Sunio Pty Singapore) – (both are WOS osSunio Japan);

- Such transfer should not attract capital gains in the country in which the amalgamating company is incorporated. However, it is given that such transaction is taxable in China and hence the exemption shall not be available.

Such transaction would be liable to capital gains tax in India.

International Taxation Case Study 9 – Non Resident Taxation – Capital Gains on sale of GDR

Aman, a non-resident for Indian tax purpose, bought Global Depository Receipts

of an Indian Company, MNO Ltd, which were issued in accordance with the notified scheme of the Central Government, in foreign currency. During FY 2018-19, he sold part of the GDRs to an eligible NR outside India and remaining to Mr. Chaman, a ROR. Compute the capital gains tax on such sale ?

Solution :-

There would be no capital gains, that would arise to Aman on sale of GDR purchased in foreign currency to a NR. However, capital gains arising on sale of GDRs to Mr. Chaman, would be liable to be taxed in India @10% without indexation benefit.