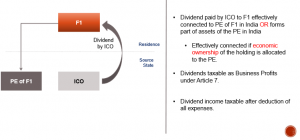

ARTICLE 10(4) OF INDIA USA TREATY – PE OR FIXED BASE

The provisions of paragraphs 1 and 2 shall not apply

if the beneficial owner of the dividends, being a resident of a Contracting State,

carries on business in the other Contracting State, of which the company paying the dividends is a resident, through a permanent establishment situated therein, or performs in that other State independent personal services from a fixed base situated therein, and the dividends are attributable to such permanent establishment or fixed base.

In such case the provisions of Article 7 (Business Profits) or Article 15 (Independent Personal Services), as the case may be, shall apply

PE SITUATION

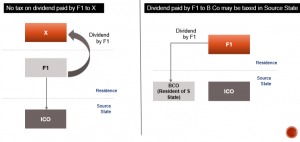

ARTICLE 10(5) – RIGHT TO TAX DIVIDEND DECLARED BY FOREIGN CO DERIVING INCOME FROM OTHER STATE

Where a company which is a resident of a Contracting State derives profits or income from the other Contracting State,

that other State may not impose any tax on the dividends paid by the company except insofar as such dividends are paid to a resident of that other State (Case 2)

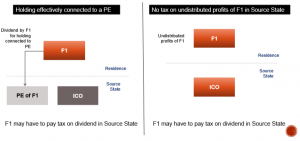

or insofar as the holding in respect of which the dividends are paid is effectively connected with a permanent establishment or a fixed base situated in that other State, (Case 3)

nor subject the company’s undistributed profits to a tax on the company’s undistributed profits, even if the dividends paid or the undistributed profits consist wholly or partly of profits or income arising in such other State (Case 4)

CASE 1 AND 2 – F1 DERIVES INCOME FROM SOURCE STATE

CASE 3 AND 4

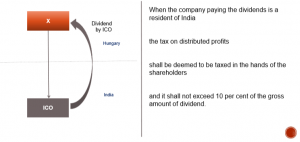

INDIA HUNGARY TREATY – PROTOCOL