F.No.370142/10/2018-TPL

Government of India

Ministry of Finance

Department of Revenue

Central Board of Direct Taxes

(TPL Division)

***

New Delhi, dated the 17th August, 2018

Subject: Draft notification proposing an amendment of the Income-tax Rules, 1962 for making the process of issue of certificate for no deduction, lower deduction and collection of tax electronic – reg.

Section 197 of the Income-tax Act, 1961 („the Act‟) contains provisions enabling the Assessing Officer („AO‟) to give the assessee a certificate for deduction of income-tax at any lower rates or no deduction of income-tax, if he is satisfied, upon an application made by the assessee in this behalf, that the total income of the recipient justifies no deduction or deduction at lower rates. Similarly, sub-sections section 206C of the Act contain provisions enabling the AO to give a certificate for collection at lower rate if he is satisfied and upon an application made by the assessee

in this behalf. Further, rules 28, 28AA & 28AB, 37G & 37H and Form No. 13 have been inserted in the Income-tax Rules, 1962 („the Rules‟) to specify the form and manner in which the application for grant of the certificate for lower rate of deduction or collection or no deduction may be made.

2. It is felt that the existing Form No. 13 and relevant rules are required to be rationalised. Hence, in order to rationalise and make the process of issuance of certificate for no deduction of tax or deduction/collection of tax at lower rate electronic, the existing Form No.13 and relevant rules are required to be amended. Accordingly, certain amendments in Form No. 13, and rules 28, 28AA, 28AB, 37G and 37H of the Income-tax Rules, 1962 are proposed.

3. The draft proposal is as under: __

“In the Income-tax Rules, 1962,-

(I) for rule 28, the following rule shall be substituted, namely: __

Application for certificates for deduction of tax at lower rates.

28. (1) An application by a person for a certificate under sub-section (1) of section 197 shall be made

in Form No. 13 electronically, ___

(i) under digital signature; or

(ii) through electronic verification code.

(2) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall specify procedures, formats and standards for ensuring secure capture and transmission of data and uploading of documents. The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to the furnishing of Form No.13.‟;

(II) in rule 28AA, __

(a) in sub-rule (2), in clause (ii), for the words “income, as the case may be, of the last three”, the words “or estimated income, as the case may be, of last four” shall be substituted;

(b) in sub-rule (2), in clause (iv), after the word “payment”, the words “, tax deducted at source and tax collected at source” shall be inserted”;

(c) in sub-rule (2), clause (v) and clause (vi) shall be omitted;

(d) in sub-rule (4), after the word “deduction”, the words “or lower deduction” shall be inserted;

(e) for sub-rule (6), the following shall be substituted:

(6) The certificate for deduction of tax at lower rate may be issued to the person who made an application for issue of such certificate, authorising him to receive income or sum after deduction of tax at lower rate, where the number of persons responsible for deducting the tax is likely to exceed hundred and the details of such persons are not available at the time of making application with the person making such application.

(7) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall specify procedures, formats and standards for issuance of certificate under sub-rule (5) and sub-rule (6). The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to the issuance of said certificate‟;

(III) in rule 28AB, __

(a) in sub-rule (2), in clause (i), after the word “made;” the word “and” shall be inserted;

(b) in sub-rule (2), in clause (ii), for the words “income-tax; and” the word “income-tax.” shall be substituted;

(c) in sub-rule (2), clause (iii) shall be omitted.‟;

(IV) for rule 37G, the following rule shall be substituted, namely: __

Application for certificate for collection of tax at lower rates under sub-section (9) of section 206C.

37G. (1) An application by the buyer or licensee or lessee for a certificate under sub-section (9) of section 206C shall be made in Form No. 13 electronically, –

(i) under digital signature; or

(ii) through electronic verification code.

(2) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems), as the case may be, shall specify procedures, formats and standards for ensuring secure capture and transmission of data and uploading of documents. The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to the

furnishing of Form No.13‟;

(V) in rule 37H, __

(a) for sub-rule (1), following rule shall be substituted, namely:-

(1) Where the Assessing Officer, on an application made by a person under sub-rule (1) of rule 37G is satisfied that existing and estimated tax liability of a person justifies the collection of tax at lower rate, the Assessing Officer shall issue a certificate in accordance with the provisions of sub-section (9) of section 206C for collection of tax at such lower rate;

(1A) The existing and estimated liability referred to in sub-rule (1) shall be determined by the Assessing Officer after taking into consideration the following:-

(i) tax payable on estimated income of the previous year relevant to the assessment year;

(ii) tax payable on the assessed or returned or estimated income, as the case may be, of the last four previous years;

(iii) existing liability under the Income-tax Act, 1961 and Wealth-tax Act, 1957;

(iv) advance tax payment, tax deducted at source and tax collected at source for the relevant assessment year relevant to the previous year till the date of making application under subrule (1) of rule 37G.‟;

(b) after sub-rule (5), the following rule shall be inserted, namely, :-

(6) The Principal Director General of Income-tax (Systems) or the Director General of Income-tax

(Systems), as the case may be, shall specify procedures, formats and standards for issuance of certificate under sub-rule (5). The Principal Director General of Income-tax (Systems) or the Director General of Income-tax (Systems) shall also be responsible for evolving and implementing appropriate security, archival and retrieval policies in relation to the issuance of said certificate.‟;

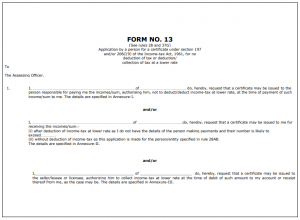

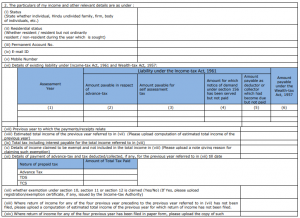

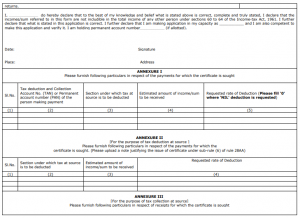

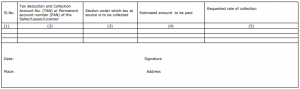

(VI) in Appendix II, for Form No.13, the following shall be substituted, namely:__

4. The comments and suggestions of stakeholders and general public on the above draft notification are invited. The comments and suggestions may be sent electronically by 04th September, 2018 at the email address, ts.mapwal@nic.in

(Sanyam Suresh Joshi)

DCIT (OSD) (TPL-III)

Tel: 011-23095470