RELEVANCE OF ARTICLE 7 BUSINESS PROFITS

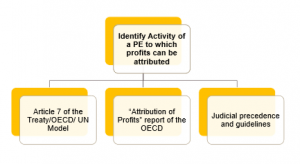

METHODOLOGY OF ATTRIBUTION OF PROFITS

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

ARTICLE 7 – INDIA USA TREATY

ARTICLE 7(1) – INDIA USA TREATY

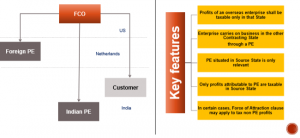

The profits of an enterprise of a Contracting State shall be taxable only in that State

unless the enterprise carries on business in the other Contracting State

through a permanent establishment situated therein.

If the enterprise carries on business as aforesaid,

the profits of the enterprise may be taxed in the other State

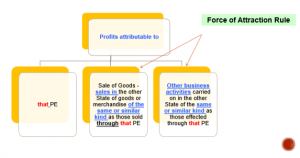

but only so much of them as is attributable to

(a) that permanent establishment ;

(a) sales in the other State of goods or merchandise of the same or similar kind as those sold through that permanent establishment ; or

(b) other business activities carried on in the other State of the same or similar kind as those effected through that permanent establishment.

CHARACTERSTICS OF ARTICLE 7(1)

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

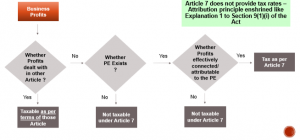

WHAT IS TAXABLE UNDER ARTICLE 7 BUSINESS PROFITS

TURNKEY CONTRACTS – ACTIVITIES IN & OUTSIDE INDIA

ARTICLE 7(2) – INDIA USA TREATY

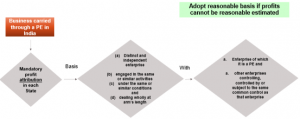

Subject to the provisions of paragraph 3,

where an enterprise of a Contracting State carries on business in the other Contracting State through a permanent establishment situated therein,

there shall in each Contracting State be attributed to that permanent establishment

the profits which it might be expected to make if it were a

distinct and independent enterprise

engaged in the same or similar activities

under the same or similar conditions and

dealing wholly at arm’s length

with the enterprise of which it is a permanent establishment and other enterprises controlling, controlled by or subject to the same common control as that enterprise.

In any case where the correct amount of profits attributable to a permanent establishment is incapable of determination or the determination thereof presents exceptional difficulties, the profits attributable to the permanent establishment may be estimated on a reasonable basis. The estimate adopted shall, however, be such that the result shall be in accordance with the principles contained in this Article.

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

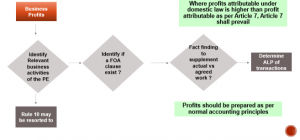

BASIS OF ALLOCATING PROFITS

HOW TO ASCERTAIN PROFITS OF A PE ?

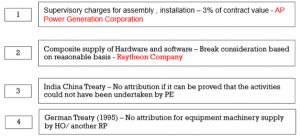

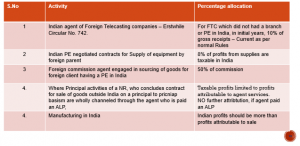

EXAMPLES

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

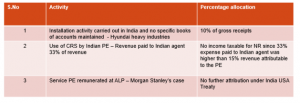

JUDICIAL PRECEDENTS ON ATTRIBUTION OF PROFITS

JUDICIAL PRECEDENTS ON ATTRIBUTION OF PROFITS

ARTICLE 7(3) – INDIA USA TREATY

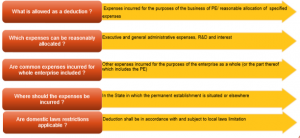

In the determination of the profits of a permanent establishment,

there shall be allowed as deductions

expenses which are incurred for the purposes of the business of the permanent establishment,

including a reasonable allocation of executive and general administrative expenses, research and development expenses, interest, and other expenses incurred for the purposes of the enterprise as a whole (or the part thereof which includes the permanent establishment),

whether incurred in the State in which the permanent establishment is situated or elsewhere,

in accordance with the provisions of and subject to the limitations of the taxation laws of that State.

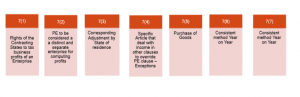

ARTICLE 7(3) – KEY CHARACTERSTICS

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

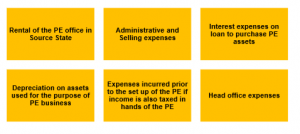

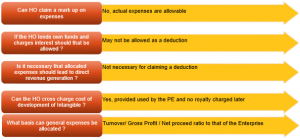

CAN THE FOLLOWING BE CLAIMED AS A DEDUCTION ?

ARTICLE 7(3) – HEAD OFFICE EXPENSES

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

ARTICLE 7(3) – INDIA USA TREATY

However, no such deduction shall be allowed in respect of amounts, if any, paid (otherwise than towards reimbursement of actual expenses) by the permanent establishment to the head office of the enterprise or any of its other offices, by way of royalties, fees or other similar payments in return for the use of patents, know-how or other rights, or by way of commission or other charges for specific services performed or for management, or, except in the case of a banking enterprises, by way of interest on moneys lent to the permanent establishment.

Likewise, no account shall be taken, in the determination of the profits of a permanent establishment, for amounts charged (otherwise than toward reimbursement of actual expenses), by the permanent establishment to the head office of the enterprise or any of its other offices, by way of royalties, fees or other similar payments in return for the use of patents, know-how or other rights, or by way of commission or other charges for specific services performed or for management, or, except in the case of a banking enterprise, by way of interest on moneys lent to the head office of the enterprise or any of its other offices.

ARTICLE 7(4) – INDIA USA TREATY

No profits shall be attributed to a permanent establishment

by reason of the

mere purchase by that permanent establishment

of goods or merchandise for the enterprise.

ARTICLE 7(5) – INDIA USA TREATY

For the purposes of this Convention,

the profits to be attributed to the permanent establishment as provided in paragraph 1(a) of this Article

shall include

only the profits derived from the assets and activities of the permanent establishment

and shall be determined by the same method year by year unless there is good and sufficient reason to the contrary.

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

ARTICLE 7(6) – INDIA USA TREATY

Where profits include

items of income which are dealt with separately in other Articles of the Convention,

then the provisions of those Articles shall not be affected by the provisions of this Article.

ARTICLE 7(7) – INDIA USA TREATY

For the purposes of the Convention,

the term “business profits”

means

income derived from any trade or business

including income from the furnishing of services other than included services as defined in Article 12 (Royalties and Fees for Included Services) and

including income from the rental of tangible personal property other than property described in paragraph 3(b) of Article 12 (Royalties and Fees for Included Services)

RULE 10 OF INCOME TAX RULES

If AO is of opinion,

that actual income accruing or arising to any non-resident person whether directly or indirectly cannot be definitely ascertained,

the amount of such income for the purposes of assessment to income-tax may be calculated :

• At such % of turnover, as is considered reasonable by AO;

• Apportioning total profits of business of NR in the Ratio of Indian receipts to total receipts of the business

• such other manner as the AO deems suitable.

SPECIFIC RULINGS