Permanent Establishment, refers to a fixed place of business or some other form of presence of the Non resident in the Source country, through which the business of the enterprise is wholly or partly carried on.

Under the Indian Income Tax Act, 1961, the concept of Permanent Establishment is substituted by what is referred to as Business Connection.

BUSINESS CONNECTION – SECTION 9(1)(i) OF THE IT ACT

Under this Section, the following incomes shall be deemed to accrue or arise in India :—

i. all income accruing or arising, whether directly or indirectly, through or from any business connection in India, or through or from …..

Explanation 1 — For the purposes of this clause —

a) in the case of a business of which all the operations are not carried out in India, the income of the business deemed under this clause to accrue or arise in India shall be only such part of the income as is reasonably attributable to the operations carried out in India ;

Inclusive definition of PE also exist under Section 92F (iii a) of the IT Act

Other aspects covered in section 9(1)(i)

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

Inclusive definition of PE under Section 92F (iii a) of the IT Act

“Permanent Establishment”, referred to in clause (iii),

includes

a fixed place of

business through which the business of the enterprise

is wholly or partly

carried on.

Article 5 Permanent Establishment – Vishakhapatnam Case

The words ‘permanent establishment’ postulate the existence of a substantial element of an enduring or permanent nature of a foreign enterprise in another country which can be attributed to a fixed place of business in that country.

It should be of such a nature that it would amount to a virtual projection of the foreign enterprises of one country into the soil of another country.

Characteristics of a PE

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

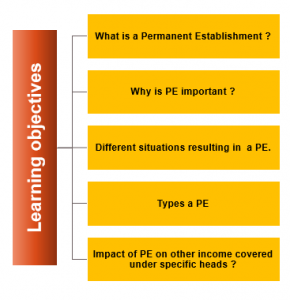

What we should learn from this presentation ?

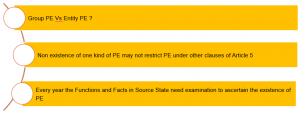

KEY ISSUES IN PE ANALYSIS

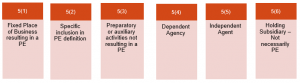

Scheme – Article 5 Permanent Establishment of the India USA treaty

Article 5(1) – India USA treaty – Fixed Place PE

For the purposes of this Convention,

the term “permanent establishment” means

a fixed place of business

through which

the business of an enterprise

is wholly or partly

carried on.

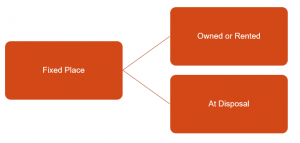

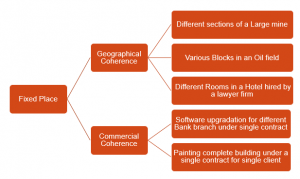

FIXED PLACE OF BUSINESS

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

WHETHER RIGHT OF DISPOSAL EXIST IN FOLLOWING CASES ?

FIXED PLACE OF BUSINESS

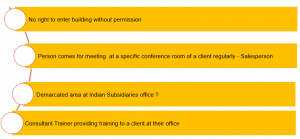

Whether following are included in fixed place ?

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

Whether following are included in fixed place ?

Carried on business ?

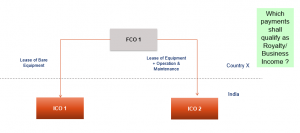

Fixed Place PE – Lease

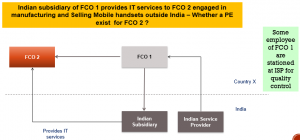

Provision of it services to affiliate of head office

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

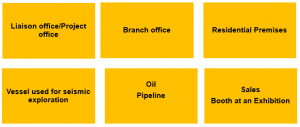

Article 5(2) – India USA Treaty – Inclusions in PE

The term “permanent establishment” includes especially :

a)a place of management ;

b)a branch ;

c)an office ;

d)a factory ;

e)a workshop ;

f)a mine, an oil or gas well, a quarry, or any other place of extraction of natural resources ;

g)a warehouse, in relation to a person providing storage facilities for others ;

h)a farm, plantation or other place where agriculture, forestry, plantation or related activities are carried on ;

i)a store or premises used as a sales outlet ;

Article 5(2)(J) – india USA treaty – STRUCTURE FOR EXPLOITATION OF NATURAL RESOURCES

an installation or structure

used for the exploration or exploitation of natural resources,

but only if so used

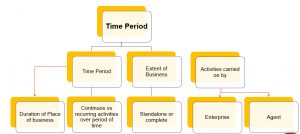

for a period of more than 120 days in any twelve-month period

STRUCTURE FOR EXPLOITATION OF NATURAL RESOURCES

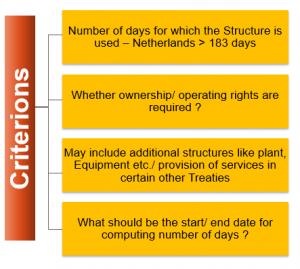

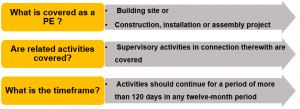

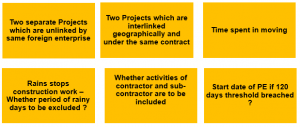

Article 5(2)(k) – INDIA USA TREATY – CONSTRUCTION PE

a building site or

construction, installation or assembly project or,

Supervisory activities in connection therewith,

where such site, project or activities (together with other such sites, projects or activities, if any)

continue for a period of more than 120 days in any twelve-month period ;

INCLUSIONS

COMPUTING THE PERIOD OF ACTIVITIES – FACTORS

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

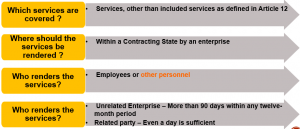

Article 5(2)(L) – INDIA USA TREATY – SERVICE PE

the furnishing of services, other than included services as defined in Article 12 (Royalties and Fees for Included Services),

within a Contracting State by an enterprise

through employees or other personnel,

but only if:

i. activities of that nature continue within that State for a period of periods aggregating more than 90 days within any twelve-month period ; or

ii. the services are performed within that State for a related enterprise [within the meaning of paragraph 1 of Article 9 (Associated Enterprises)].

SERVICE PE

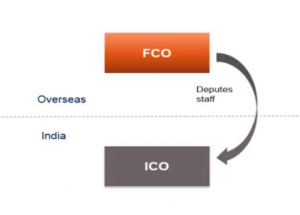

SERVICE PE – CASE STUDY

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

Facts:

- ICO provided certain BPO services to FCO on Cost plus basis

- Certain staff of FCO, which was on its payroll was working in India

- Under the terms of the contract, the staff was to work under the control and supervision of ICO , although there salaries were paid by FCO, which were later reimbursed by ICO

- The appraisal of staff was done by ICO in consultation with FCO and the staff were to return back to FCO post deputation

Issue:

- Whether FCO had a PE in India

Held:

- Yes, it was held that FCO was rendering services to ICO through its employees

Article 5(3) – India USA Treaty – Preparatory or Auxiliary Activities

Notwithstanding the preceding provisions of this Article, the term “permanent establishment” shall be deemed not to include any one or more of the following :

a)the use of facilities solely for the purpose of storage, display, or occasional delivery of goods or merchandise belonging to the enterprise ;

b) the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of storage, display, or occasional delivery ;

c) the maintenance of a stock of goods or merchandise belonging to the enterprise solely for the purpose of processing by another enterprise ;

d) the maintenance of a fixed place of business solely for the purpose of purchasing goods or merchandise, or of collecting information, for the enterprise ;

e) the maintenance of a fixed place of business solely for the purpose of advertising, for the supply of information, for scientific research or for other activities which have a preparatory or auxiliary character, for the enterprise.

WHETHER ACTIVITIES ARE PREPARATORY OR AUXILLIARY

LIAISON OFFICE

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

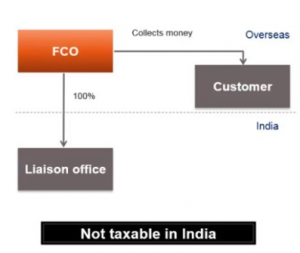

UAE EXCHANGE CENTRE LLC – DELHI HC

Facts:

- FCO collected funds from customers overseas who were interested in remitting funds to India;

- It had a LO in India, which downloaded information by connecting to FCo’s servers, made cheques and handed these over to the recipient

Issue:

- Whether LO constituted a PE in India

Held:

- Delhi High Court has Ruled that no PE arise in such a case

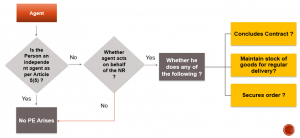

MATRIX FOR AGENCY PE

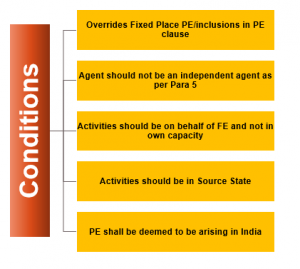

Article 5(4) – India USA Treaty – Dependent Agent

Notwithstanding the provisions of paragraphs 1 and 2

where a person—other than an agent of an independent status to whom paragraph 5 applies – is acting in a Contracting State

on behalf of an enterprise of the other Contracting State.

that enterprise shall be deemed to have a permanent establishment in the first-mentioned State, if : –

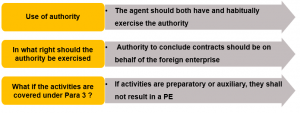

a)he has and habitually exercises in the first-mentioned State

an authority to conclude on behalf of the enterprise,

unless his activities are limited to those mentioned in paragraph 3 which, if exercised through a fixed place of business, would not make that fixed place of business a permanent establishment under the provisions of that paragraph ;

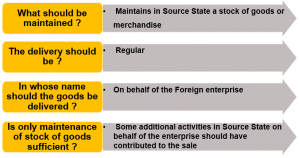

b) he has no such authority but

habitually maintains in the first-mentioned State a stock of goods or merchandise from which he regularly delivers goods or merchandise on behalf of the enterprise, and some additional activities conducted in the State on behalf of the enterprise have contributed to the sale of the goods or merchandise ; or

c) he habitually secures orders in the first-mentioned State, wholly or almost wholly for the enterprise.

CHARACTERSTICS

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

AUTHORITY TO CONCLUDE CONTRACT

MAINTAINING STOCK OF GOODS FOR DELIVERY

HABITUALLY SECURES ORDERS IN SOURCE STATE

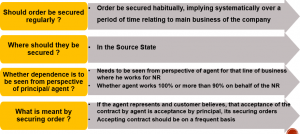

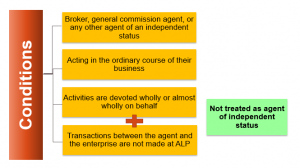

Article 5(5) – India USA Treaty – Independent Agent

An enterprise of a Contracting State shall not be deemed to have a permanent establishment in the other Contracting State

merely because it carries on business in that other State through a broker, general commission agent, or any other agent of an independent status.

provided that such persons are acting in the ordinary course of their business.

However, when the activities of such an agent are devoted wholly or almost wholly on behalf of that enterprise and

the transactions between the agent and the enterprise are not made under arm’s length conditions,

he shall not be considered an agent of independent status within the meaning of this paragraph

Article 5 Permanent Establishment – Independent Agent

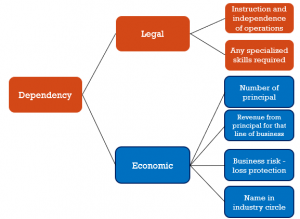

FACTORS TO BE CONSIDERED FOR DEPENDENCY

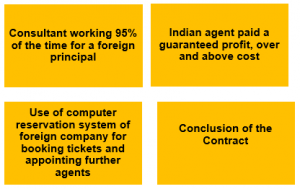

WHETHER DEPENDENT AGENT IN FOLLOWING CASES :-

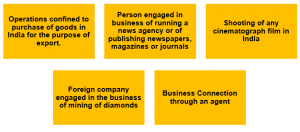

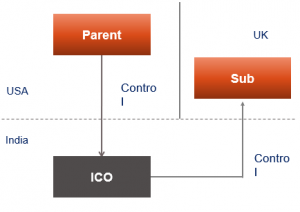

ARTICLE 5(6) – INDIA USA TREATY – HOLDING SUBSIDIARY RELATIONSHIP

The fact that a company which is a resident of a Contracting State

controls or

is controlled

by a company which is a resident of the other Contracting State,

or which carries on business in that other State (whether through a permanent establishment or otherwise),

shall not of itself constitute either company a permanent establishment of the other