APPLICABILITY OF ARTICLE 23

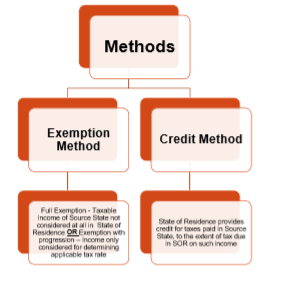

TYPES OF RELIEF FROM DOUBLE TAXATION

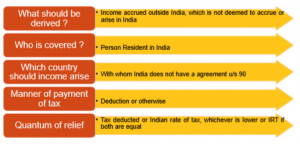

UNILATERAL RELIEF – SECTION 91

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

UNDERLYING CREDIT

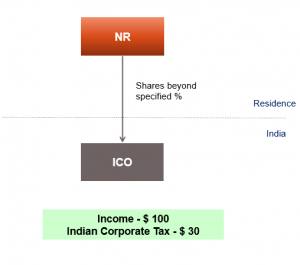

- In present case, taxes may be paid by :-

ICO; and

Shareholders on dividend distributed out of remaining

- For underlying credit clause, State of Residence grants credit of : –

Corporate taxes paid by ICO $ 30;

WHT on dividends $ 7.

India USA Treaty Clause : –

“in the case of a United States company owning at least 10 per cent of the voting stock of a company which is a resident of India and from which the United States company receives dividends, the income-tax paid to India by or on behalf of the distributing company with respect to the profits out of which the dividends are paid”

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

TAX SPARING

METHODS OF PROVIDING CREDIT

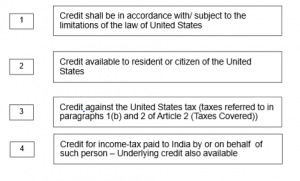

ARTICLE 25 (1) – INDIA USA TREATY – CREDIT BY USA

In accordance with the provisions and subject to the limitations of the law of the United States (as it may be amended from time to time without changing the general principle hereof),

the United States shall allow to a resident or citizen of the United States as a credit against the United States tax on income —

a. the income-tax paid to India by or on behalf of such citizen or resident ; and

b. in the case of a United States company owning at least 10 per cent of the voting stock of a company which is a resident of India and from which the United States company receives dividends, the income-tax paid to India by or on behalf of the distributing company with respect to the profits out of which the dividends are paid.

For the purposes of this paragraph, the taxes referred to in paragraphs 1(b) and 2 of Article 2 (Taxes Covered) shall be considered as income taxes.

KEY FEATURES

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

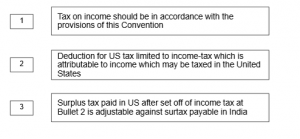

ARTICLE 25 (2) – INDIA USA TREATY

Where a resident of India derives income which, in accordance with the provisions of this Convention, may be taxed in the United States,

India shall allow as a deduction from the tax on the income of that resident an amount equal to the income-tax paid in the United States, whether directly or by deduction.

Such deduction shall not, however, exceed that part of the income-tax (as computed before the deduction is given) which is attributable to the income which may be taxed in the United States.

Further, where such resident is a company by which a surtax is payable in India, the deduction in respect of income-tax paid in the United States shall be allowed in the first instance from income-tax payable by the company in India and as to the balance, if any, from surtax payable by it in India.

KEY FEATURES

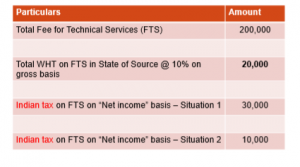

EXAMPLE ON CREDIT METHOD – QUANTUM

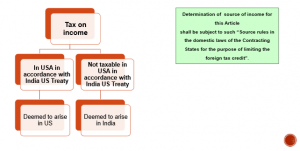

ARTICLE 25 (3) – INDIA USA TREATY – WHERE DOES INCOME ARISE

For the purposes of allowing relief from double taxation pursuant to this article, income shall be deemed to arise as follows :

a. income derived by a resident of a Contracting State which may be taxed in the other Contracting State in accordance with this Convention [other than solely by reason of citizenship in accordance with paragraph 3 of Article 1 (General Scope)] shall be deemed to arise in that other State ;

b. income derived by a resident of a Contracting State which may not be taxed in the other Contracting State in accordance with the Convention shall be deemed to arise in the first-mentioned State.

Notwithstanding the preceding sentence, the determination of the source of income for purposes of this Article shall be subject to such source rules in the domestic laws of the Contracting States as apply for the purpose of limiting the foreign tax credit.

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

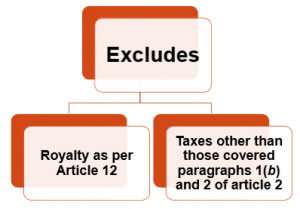

ARTICLE 25 (3) – INDIA USA TREATY – NON APPLICABILITY

The preceding sentence shall not apply with respect to income dealt with in article 12 (Royalties and Fees for Included Services).

The rules of this paragraph shall not apply in determining credits against United States tax for foreign taxes other than the taxes referred to in paragraphs 1(b) and 2 of article 2 (Taxes Covered).

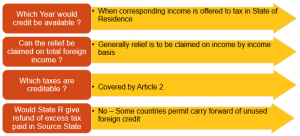

OTHER ASPECTS WORTH KNOWING

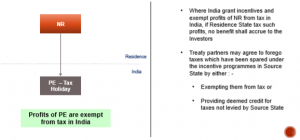

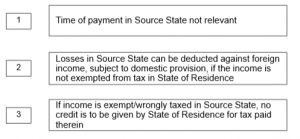

IMPACT OF VARIOUS EVENTS IN SOURCE STATE ON CREDIT/ EXEMPTION OF TAXES

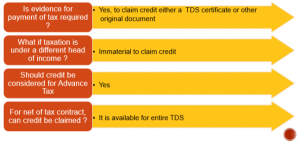

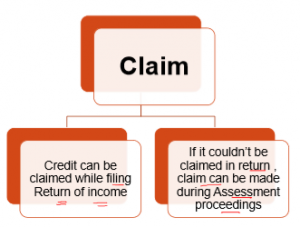

HOW CAN ONE CLAIM CREDIT ?

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

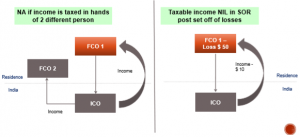

TRIANGULAR TREATY CASES