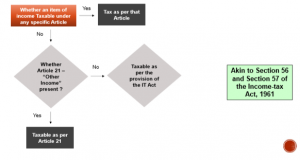

APPLICABILITY OF ARTICLE 21 – OTHER INCOME

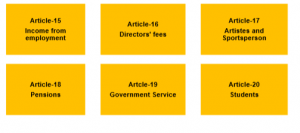

INCOME NOT COVERED UNDER FOLLOWING ARTICLE

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

INCOME NOT COVERED UNDER FOLLOWING ARTICLE

ARTICLE 23(1) OF THE INDIA – US TREATY

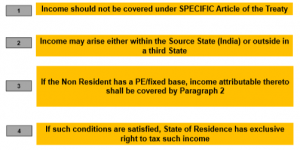

Subject to the provisions of paragraph 2,

items of income of a resident of a Contracting State,

wherever arising,

which are not expressly dealt with in the foregoing Articles of this Convention

shall be taxable only in that Contracting State

KEY CHARACTERISTICS – ARTICLE 23(1) OF THE INDIA – US TREATY

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

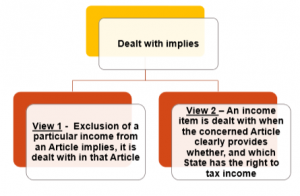

WHAT IS MEANT BY “DEALT WITH”

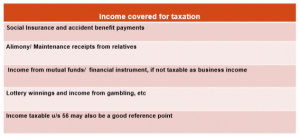

INCOME COVERED UNDER ARTICLE 21

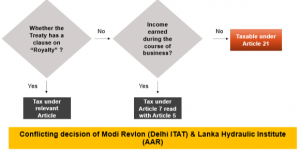

TAXABILITY OF INCOME AS “OTHER INCOME” WHEN RELEVANT CLAUSE ABSENT – ROYALTY

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

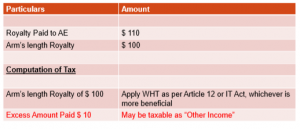

EXCESS PAYMENT TO RELATED PARTY

ARTICLE 23(2) OF THE INDIA – US TREATY

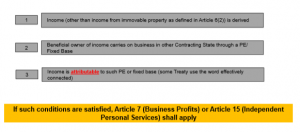

The provisions of paragraph 1 shall not apply to income, other than income from immovable property as defined in paragraph 2 of Article 6 [Income from Immovable Property (Real Property)],

if the beneficial owner of the income, being a resident of a Contracting State,

carries on business in the other Contracting State through a permanent establishment situated therein, or performs in that other State independent personal services from a fixed base situated therein, and

the income is attributable to such permanent establishment or fixed base.

In such case the provisions of Article 7 (Business Profits) or Article 15 (Independent Personal Services), as the case may be, shall apply

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

KEY CHARACTERISTICS – ARTICLE 23(2) OF THE INDIA – US TREATY

ARTICLE 21(3) OF THE INDIA US TREATY

Notwithstanding the provisions of paragraphs 1 and 2,

items of income of a resident of a Contracting State

not dealt with in the foregoing articles of this Convention and

arising in the other Contracting State

may also be taxed in that other State.