CAPITAL GAINS TO NON RESIDENT – TAX IN INDIA

WHAT COULD BE POTENTIAL SITUATIONS WHEN CAPITAL GAINS WOULD ARISE

Transfer of Shares by NR to resident

Transfer of Shares by NR to NR

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

What is the Meaning of “capital gains” ?

1. Term “Capital Gains “ defined under Article 13 ?

2. Article – 3 “General Definitions” requires application of domestic laws to ascertain meaning of terms not defined in Treaty

3. Income assessable under Section 45 of IT Act, 1961, may be considered as Capital gains

4.Subject matter of transfer should be a “Capital assets” and not “stock-in-trade”

5.What if a particular Capital Gains is not taxable under IT Act at all ?

6.Capital gains may be Long-term or Short-term capital gain, and may be chargeable to tax at special or normal rates

“CAPITAL ASSETS” COVERED UNDER ARTICLE 13 ?

1. Capital Assets

2. Immovable property referred to in Article 6 – Article 13(1)

3. Movable property forming part of Business property of a PE / Fixed Base – 13(2)

4.Ships, Aircrafts, Boats, etc. operated in international traffic/ movable property pertaining to such operations – 13(3)

5. Shares of Real Estate company – 13(4)

6. Any other property – 13(5)

RIGHT TO TAX OF SOURCE &/OR RESIDENT STATE

- Right to tax

2. Only India – (No Treaty like Cayman Island)

3. Only Treaty Partner (India-Singapore Treaty)

4. Both India & Treaty partner (India – USA Treaty)

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

RIGHT TO TAX WITH TREATY PARTNER – INDIA SINGAPORE TREATY

1.Gains derived by a resident of a Contracting State from the alienation of immovable property …..

2.Gains from the alienation of movable property forming part of the business property of a permanent establishment …….

3. Gains from the alienation of ships or aircraft …….

4. Gains derived by a resident of a Contracting State from the alienation of any property other than those mentioned in paragraphs 1, 2 and 3 of this Article shall be taxable only in that State.

RIGHT TO TAX WITH BOTH COUNTRIES – INDIA US TREATY

Except as provided in Article 8 (Shipping and Air Transport) of this Convention

each Contracting State may tax capital gains

in accordance with the provisions of its domestic law.

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

TAXATION OF CAPITAL GAINS

- Taxable under Act

- No

- Not taxable

- Yes

- Whether Article 13 present ?

- Yes

- Taxable as per Article 13

- No

- Whether Article 21 – “Other Income” present ?

- Yes

- May be taxable as per Article 21

- No

- Taxable as per Domestic laws

ALIENATION VS TRANSFER IN CAPITAL GAINS TAX

- Whether term “Alienation” is defined in Treaty?

- Yes

- Apply such definition

- India-Mauritius Treaty

- Whether Protocol permits application of definition of “transfer” as per Section 2(47)

- Yes

- Apply such definition

- India-Canada Treaty

- If above conditions are not satisfied, definition of Transfer cannot be applied to ascertain meaning of “Alienation”.

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

ALIENATION AS PER INDIA – MAURITIUS TREATY

Alienation means the

sale,

exchange,

transfer, or

relinquishment of the property, or

the extinguishment of any rights therein, or

the compulsory acquisition thereof under any law in force in the respective Contracting States.

ALIENATION OF PROPERTY

- Alienation

- Sale of a property

- Exchange of a property

- Extinguishment of rights in a property

- Transfer of a property

- Gift

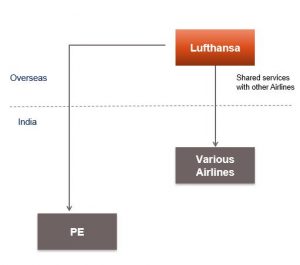

EXISTENCE OF PE AND CAPITAL GAINS – LUFTHANSA GERMAN AIRLINES CASE

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

Facts:

- Lufthansa airlines provided handling services to other airlines in India, as per the International Airline Technical Pool, as per IATP manual

- It also availed services from other Airlines

- Taxpayer claimed that income from various airline was not taxable in India in terms of Article 8 (4), which covered profits from the participation in a pool.

Issue:

- Whether profits earned by Lufthansa airlines was taxable under Article 8(4) or Article 7 & 5 ?

Held:

- Profits will be taxable under Article 8(4) which specifically covered profit from participation in pool.

ARTICLE 8 AS PER INDIA – GERMANY TREATY

1.Profits from the operation of ships or aircraft in international traffic shall be taxable only in the Contracting State in which the place of effective management of the enterprise is situated.

2.If the place of effective management of a shipping enterprise is aboard a ship, then it shall be deemed to be situated in the Contracting State in which the home harbour of the ship is situated, or, if there is no such home harbour, in the Contracting State of which the operator of the ship is a resident.

3.For the purposes of this Article, interest on funds connected with the operation of ships or aircraft in international traffic shall be regarded as profits derived from the operation of such ships or aircraft, and the provisions of Article 11 shall not apply in relation to such interest.

4.The provisions of paragraph 1 shall also apply to profits from the participation in a pool, a joint business or an international operating agency.

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

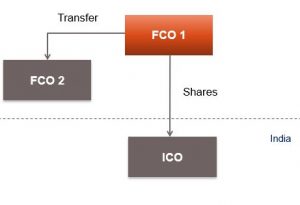

MAT ON SALE OF SHARES OF INDIAN COMPANY

Facts:

- FCO 1 is an Foreign Co. engaged in the manufacturing business

- ICO is a WOS of FCO 1;

- FCO 1 sold shares of ICO to FCO 2, a Mauritius Co.

Issue:

- Whether MAT is applicable on Capital Gain?

Position :

- Explanation 4 to Section 115JB(1) provides that MAT shall not apply to a foreign company if : –

- India has entered into a DTAA (Section 90(1))/relief from double taxation u/s 90A(1) with the country of whom the NR is a resident

- NR does not have a PE in India as per said agreement

Click here to Enroll in Interpretation of Tax Treaty (DTAA) – International Taxation Course

AMENDMENT BY FINANCE ACT 2016

- Applicability of MAT

2(a) DTAA (Section 90(1))/Relief from double taxation agreement u/s 90A(1)

2(b) No DTAA/ Relief agreement

2(a) 3 No PE – MAT not applicable

2(a) 4 Has a PE – MAT applicable

2(b) 5 NA if NR not required to obtain registration in India under any law in force for the time being

ARTICLE 13(1) – INDIA – AUSTRIA IMMOVABLE PROPERTY

Gains

derived by a resident of Contracting State

from the alienation of a immovable property referred to in Article 6

and

situated in the Other Contracting State

may be taxed in that Other State.