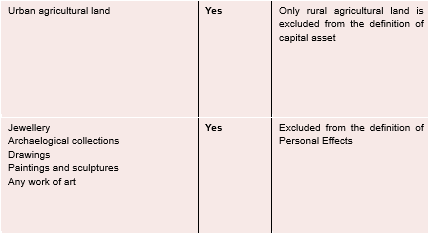

NO EXEMPTION U/S 10 ON URBAN AGRICULTURAL LAND – EXPLANATION 1 TO SECTION 2(1A)

While agricultural income is exempt from income-tax under Section 10(1) , Explanation 1 to Section 2(1A) , clarifies that capital gains arising from urban agricultural land would not be treated as agricultural income, and would this be chargeable to tax under Section 45.

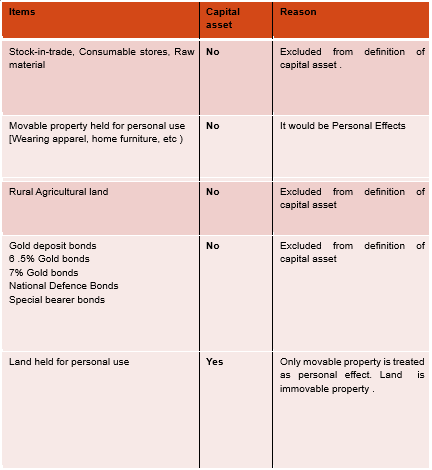

ASSETS NOT CONSIDERED AS CAPITAL ASSET – BONDS

The following bonds would not be considered as a Capital Asset : –

- Specified Gold Bonds : – 6½% Gold Bonds, 1977, or 7% Gold Bonds, 1980, or National Defence Bonds

- Special Bearer Bonds, 1991 issued by the Central Government;

- Gold Deposit Bonds issued under the Gold Deposit Scheme, 1999 or deposit certificates issued under the Gold Monetisation Scheme, 2015 notified by the Central Government .

CAPITAL ASSETS