PURPOSE OF THE AUTHORITY FOR ADVANCE RULINGS (‘AAR’) FOR INCOME TAX

The Authority for Advance Rulings (‘AAR’), gives a ruling to : –

- a Non-resident; or

- Specified resident

relating to a transaction which is

- undertaken; or

- a future transaction.

This brings upfront clarity with regard to the taxability of the income of the applicant.

This scheme seeks to reduce potential disputes between the Income-tax authorities and the taxpayers.

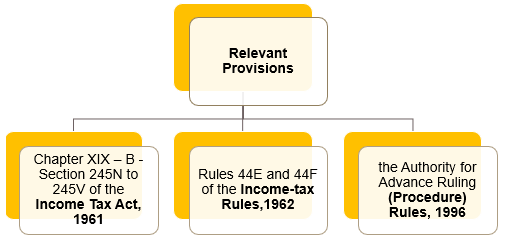

ENABLING PROVISIONS

The provisions of law pertaining to AAR are as follows : –

- Chapter XIX – B – Section 245N to 245V of the Income Tax Act, 1961;

- Rules 44E and 44F of the Income-tax Rules,1962; and

- the Authority for Advance Ruling (Procedure) Rules, 1996 [‘Rules’].

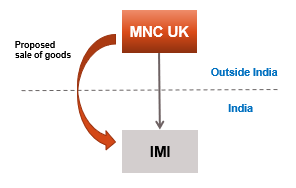

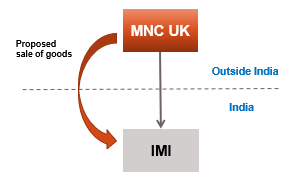

ILLUSTRATION – 1

MNC Ltd. UK, intends to sell goods to IMI Private Limited, an Indian company. They are not sure whether the income arising from such a sale would be taxable in India. Can MNC Ltd obtain an AAR Ruling?

SOLUTION

Authority for Advance Rulings gives a ruling to a non-resident relating to a transaction that is proposed to be undertaken. Hence, MNC Ltd. UK can obtain an AAR Ruling

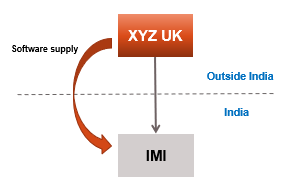

ILLUSTRATION – 2

XYZ Ltd UK, supplied software in FY 2016-17 to IMI Private Limited, an Indian company? There are no income tax proceedings pending against XYZ Ltd UK, in respect of any transaction. Can they obtain an Advance Ruling?

SOLUTION

The Authority for Advance Rulings (‘AAR’), gives a ruling to a non-resident relating to a transaction which has been undertaken provided certain conditions are satisfied. Hence, XYZ Ltd UK can obtain an AAR Ruling.

ILLUSTRATION – 3

In Example (2) above, can IMI Private Limited, an Indian company obtain an Advance Ruling?

SOLUTION

IMI Private Limited can obtain an AAR Ruling, provided it falls within the definition of “specified person”.

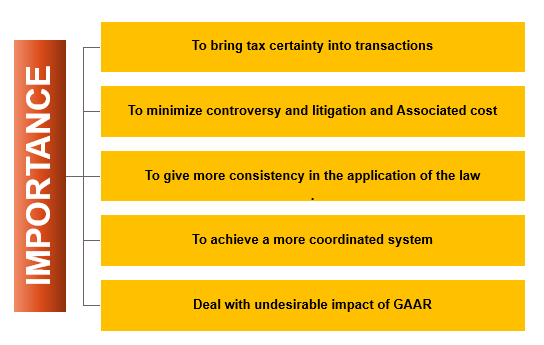

IMPORTANCE OF AAR (Authority for advance rulings)

DEAL WITH UNDESIRABLE IMPACT OF GAAR

Introduction of General Anti-Avoidance Regulations (‘GAAR’), would also lead to an increase in uncertainty for the taxpayers, and therefore, a greater demand for advance rulings. The reason is that GAAR, in the form it is generally incorporated to tax laws, has the potential to be applied by tax officers to genuine transactions, which are entered for legitimate business purpose

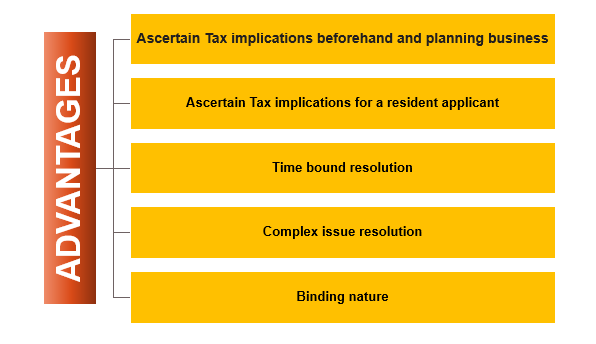

ADVANTAGES OF AAR (Authority for advance rulings)