MEANING OF POEM (PLACE OF EFFECTIVE MANAGEMENT)

POEM (Place of Effective Management), is an internationally acceptable test to determine, whether a company incorporated in a foreign jurisdiction, is a tax resident of another country.

“Place of effective management” means a place where : –

- Key management, and commercial decisions

- that are necessary for the conduct of the business of an entity as a whole are,

- in substance made.

Points to remember : –

- The criteria for determination of POEM are the place where management and commercial decisions are taken;

- Such management and commercial decisions should be key to the entire business operations of the entity. If the decision relate to routine operations, these would not be relevant for the determination of POEM.

- The relevant place is of where the decisions have been in substance

NON APPLICABILITY OF POEM (PLACE OF EFFECTIVE MANAGEMENT)

The criteria to determine POEM shall be applicable only if the turnover or gross receipts of a company , in a financial year, is greater than Rs. 50 crores. The provision would not be applicable, where the turnover or gross receipts of a company , in a financial year is either less than or equal to 50 crores. In such a case, the company would be treated as a non- resident for Indian tax purposes.

GUIDING PRINCIPLE FOR DETERMINATION OF POEM (PLACE OF EFFECTIVE MANAGEMENT)

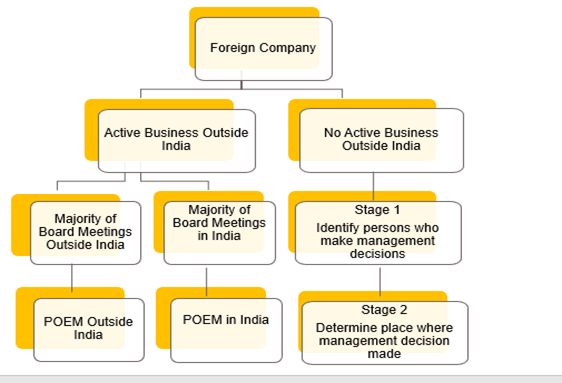

In order to determine, whether the POEM of a company is in India, or outside India, the first thing one needs find out is, whether the company is Engaged in Active business at a place in India or outside India (“Active Business Test”)?

There are different set of conditions, which needs to be applied to ascertain, the applicability of POEM depending on whether the company is : –

- Engaged in “Active Business Outside India”; and

- Not engaged in “Active Business Outside India”.

WHAT IS ACTIVE BUSINESS OUTSIDE INDIA ?

The applicability of POEM requires an understanding of the term Active Business Outside India . For detailed, discussion, refer Paragraph

PLACE OF EFFECTIVE MANAGEMENT FOR COMPANIES ENGAGED IN “ACTIVE BUSINESS OUTSIDE INDIA”

POEM of companies, which are engaged in “Active Business Outside India” (ABOI) shall be presumed to be outside India, if the majority of the Board meeting are held outside India. Thus, in such a case, the emphasis is on the place where majority of board meetings are held. If, majority of board meetings are held in India, the place of effective management would be in India. However, if the majority of board meetings are held outside India, the POEM would be outside India.

However, there is an exception to these rules. In case of a foreign company, even if the majority of board meetings are held outside India, but the power of management are exercised by the following, then the POEM shall be considered to be in India : –

- Indian holding company ;

- Any other person, resident in India,

EXAMPLE : –

Alpha, Inc is engaged in Active Business Outside India. During the current financial year, total of 5 meetings of its Board of Directors were held, of which 2 were held in India and 3 were held outside India. However, the Board of Directors are not exercising powers of management and such powers are being exercised by ‘Indian holding Company’ (IHC) of Alpha Inc. Determine POEM of Alpha Inc ?

SOLUTION : –

Company having “Active Business Outside India” shall not be treated as having there PEOM in India, when majority of their Board meetings are held outside India, provided the power of management are not exercised by the Indian Holding Company. In the present case, even though the majority of Board meetings were held outside India, since the Board of Directors are not exercising powers of management, and such powers are being exercised by Indian holding company, the POEM of Alpha Inc shall be in India .Accordingly, Alpha Inc would be treated as resident in India.

IMPACT OF FOLLOWING GLOBAL POLICY OF GROUP ON “POEM”

If the Board of Directors of a company, follow the general and objective principles of global policy of the entire group,laid down by parent entity,it shall not be deemed that Board of Directors are not exercising their powers of management.

In order to avail to the benefit of this clause, the following conditions should be satisfied: –

- The matter should relate to general and objective principles of global policy of the entire group;

- They should be laid down by parent entity of the group;

- They should not be specific to any entity or groupof entities within the group;

- The Global policy may be in the field of-

- Payroll functions,

- Accounting,

- Human resource (HR) functions,

- IT infrastructure and network platforms,

- Supply chain functions,

- Routine banking operational procedures,

EXAMPLE : –

FCO is wholly owned subsidiary of ICO. Parent company (i.e., ICO) laid down principles of supply chain functions. Such principles are laid down for the entire group of companies and are not specific to an entity or group of entities within the group.Board of Directors of FCO follows such principle of supply chain functions.Whether Board of Directors of FCO are not exercising their powers of management?

SOLUTION : –

The Place of Effective Management of FCO shall be outside India. The fact that the Board of Directors are following general and objective principles of global policy laid down by Indian Parent company, would not imply that they are not their powers of management.

POEM FOR COMPANIES NOT ENGAGED IN “ACTIVE BUSINESS OUTSIDE INDIA”

If the company does not satisfy the test of ABOI, and is not engaged in “Active Business Outside India”, the POEM of the company would be determined by following the two steps as under :-

- Step 1 : – Identify the person(s) who actually make the key management and commercial decisions , which are necessary for the conduct of the business of the company as a whole.

- Step 2 : – Determine the place where these decisions are, in fact, being made.

In such a case, instead of relying solely on where the Board of Directors conduct their meetings, emphasis is on the person who actually make the decisions, and the place where the decisions are made. One important thing, that needs to be noted is that the place where management/commercial decisions are taken is more important than the place where such decisions are implemented. So if all of the decisions are taken in Singapore, but they are implemented in India, the place of decision, i.e Singapore would be more relevant.POEM of Foreign Company would be outside India where key management and commercial decisions are taken outside India. However, POEM of Foreign Company would be in India where key management and commercial decisions are taken in India.

EXAMPLE : –

- Beta Inc., held the Board meeting in USA wherein Board of Directors of the Beta Inc. agreed to sign the contract of sale. However, the contract of sale was signed in India.

- Beta Inc. is not engaged in Active Business Outside India.

- Whether Place of Effective Management of Beta Inc. would be outside India?

SOLUTION : –

- The Board of Directors decided to sign the sale contract outside India. Thus, key management decision is taken outside India.

- The Board of Directors signed the sale contract in India. Thus, the key management decision is implemented in India.

- POEM of FCO would be outside India as the place where these management decisions are taken would be more important than the place where such decisions are implemented .

EXAMPLE : –

- Gamma Pte Ltd., is wholly owned subsidiary of Shoonya India Private Limited (SIPL). SIPL laid down principles of supply chain functions. Such principles are laid down for the entire group of companies.

- Board of Directors of Gamma follows such principle of supply chain functions.

- Whether Board of Directors of Gamma are not exercising their powers of management?

SOLUTION : –

The POEM of Gamma Pte Ltd., shall be outside India. The fact that the Board of Directors are following general and objective principles of global policy laid down by Indian Parent company, would not imply that they are not their powers of management.

DETERMINATION OF PLACE OF EFFECTIVE MANAGEMENT – SUMMARY

The following chart summarizes, the concept of place of effective management : –

WHEN IS A COMPANY ENGAGED IN ACTIVE BUSINESS OUTSIDE INDIA ?

- A company shall be said to be engaged in ‘Active Business Outside India’ if it satisfies all the following conditions:

- Its passive income is 50% (or less) of its total income;

- Its total asset situated in India are less than 50% of its asset ;

- Total number of employees are situated in Indiaor employees who are resident in India, is less than50% of total employees;

- the payroll expenses incurred on such employees is less than 50% of its total payrollexpenditure.

- To understand the concept of Active business outside India, it becomes necessary to understand what is the meaning of the following : –

- What is passive income ?

- What is the meaning of total asset situated in India;

- How do I ascertain the total number of employees ?

- What forms part of the payroll expenses ?

Let us discuss each of them in the subsequent paragraph : –

MEANING OF PASSIVE INCOME

A company shall be said to be engaged in ‘Active Business Outside India’ if amongst other conditions, its passive income is 50% (or less) of its total income.

Generally speaking, passive income refers to income received on a regular basis, which requires minimal or no effort by the recipient, to maintain it.

For the purpose of, this clause, Passive income of a company shall be calculated as the sum of : –

Income from the transactions, where both the purchase, and the sale of goods is from/ to its Associated Enterprises. In this case, the transaction would be with an Associated Enterprise.

NOTE : –

Income from sale of goods to Associated Enterprise will be considered as passive income only when goods are also purchased from Associated Enterprise.

- Income by way of royalty, dividend, capital gains, interest or rental income. However, interest income of banking companies and public financial institutions would not be regarded as passive income.

NOTE : –

Such income will be considered as passive income even if there is no involvement of associated enterprises.

CALCULATION OF INCOME

The question which arises is, how should one calculate income ? There are various questions that needs to be considered, like : –

- Whether one should consider the accounting or tax income ?

- If one has to consider the tax income, which laws should be applied, i.e whether the tax laws of India or the country of incorporation should be applied ?

For this purpose the jurisdiction has to be divided into two categories : –

- Where the laws of the country of incorporation require separate computation for tax purposes – It means the income which is computed for tax purpose in accordance with the laws of the country of incorporation. FOR EXAMPLE:- In case of company, incorporated in USA, passive income will be computed as per the taxation laws of USA.

- Where the laws of the country of incorporation do not require separate computation for tax purposes – Income will be taken as per the books of accounts.

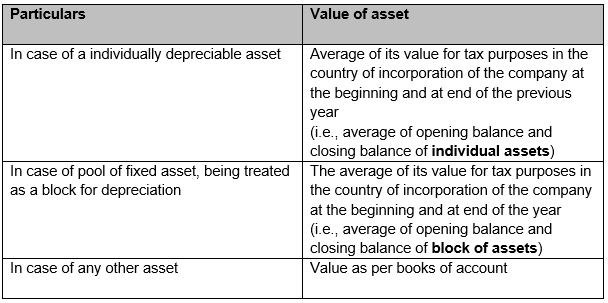

DETERMINATION OF THE VALUE OF ASSETS ?

A company shall be said to be engaged in ‘Active Business Outside India’ if amongst other conditions, less than 50% of its total asset are situated in India.

In order to compute the value of the assets, the assets have to be divided into the following two categories :-

- Depreciable assets, which are further sub-divided into assets on which

- Depreciation is claimed on an individual asset ;

- Depreciation is claimed on a block of assets;

- Non depreciable assets

The methodology for calculating the value of the assets in each of these cases is discussed as under : –

ASCERTAINING THE NUMBER OF EMPLOYEES ?

A company shall be said to be engaged in ‘Active Business Outside India’ if amongst other conditions, less than50% of total number of employees are situated in Indiaor are resident in India.

In order to ascertain the number of employees, the following two aspects needs to be considered : –

Who shall included within the definition of employee : – It shall include employees of the company. However, additionally, it shall also include persons, who are not directly employed by the company, but perform tasks similar to those performed by the employees. This would include say employees who are on payroll of other company/independent service providers but work with the company as an employee.

Computation of number of employee : – The average of the number of employees (including those discussed above) as at the beginning and at the end of theYear.

MEANING OF PAYROLL

A company shall be said to be engaged in ‘Active Business Outside India’ if amongst other conditions, the payroll expenses incurred on total number of employees situated in Indiaor employees who are resident in India isless than 50% of its total payroll expenditure. As discussed above, persons, who are not directly employed by the company, but perform tasks similar to those performed by the employees, would also be considered as employees of the company.

For the computation, of Payroll, the following expenses paid by the company are included –

- Cost of salaries,

- Wages,

- Bonus ; and

- All other employee compensation (including related pension and social costs borne by the employer).

EXAMPLE 1 : –

- Company A is a sourcing entity, for an Indian multinational group, incorporated in country X and is 100% subsidiary of Indian company (B Co.).

- The warehouses and stock therein are the only assets of the Company A in Country X. All the employees of the company are also in Country X.

- The average income wise breakup of the company’s total income for 3 years is, –

- 30% of income is from transaction where purchases are made from non-Associated Enterprises and sold to Associated Enterprises;

- 30% of income is from transaction where purchases and sales are made from/to Associated Enterprises;

- 30% of income is from transaction where purchases are made from Associated Enterprises and sold to non-Associated Enterprises; and

- 10% of the income is by way of interest.

Analyse the test of “Active Business Outside India”

SOLUTION : –

In this case, passive income is 40% of the total income of the company. The passive income consists of –

a) 30% income from the transaction where both purchase and sale is from/to Associated Enterprises; and

b) 10% income from interest.

The Company A satisfies the first requirement of the test of active business outside India. Since no assets or employees of Company A are in India the other requirements of the test is also satisfied. Therefore, company A is engaged in active business outside India.

EXAMPLE 2 : –

c) Assuming the other facts remain same as in previous Example 1 with certain employee related variations which are as under:

- A Co. has a total of 50 employees of which 47 employees, managing the warehouse, storekeeping and accounts of the company, are located in country X.

- The Managing Director (MD), Chief Executive Officer (CEO) and sales head are resident in India.

- The total annual payroll expenditure on these 50 employees is of 5 crore of which annual payroll expenditure in respect of MD, CEO and sales head is of 3 crore.

d) Analyse the test of “Active Business Outside India”?

SOLUTION : –

e) FCO satisfies the following test of ABOI : –

- 40% of its total income is passive in nature.

- More than 50% of the employees are situated outside India.

- All the assets are also situated outside India.

However, the payroll expenditure in respect of the MD, CEO and the sales head, being employees resident in India exceeds 50% of the total payroll expenditure. A Co. would be treated as not engaged in active business outside India.

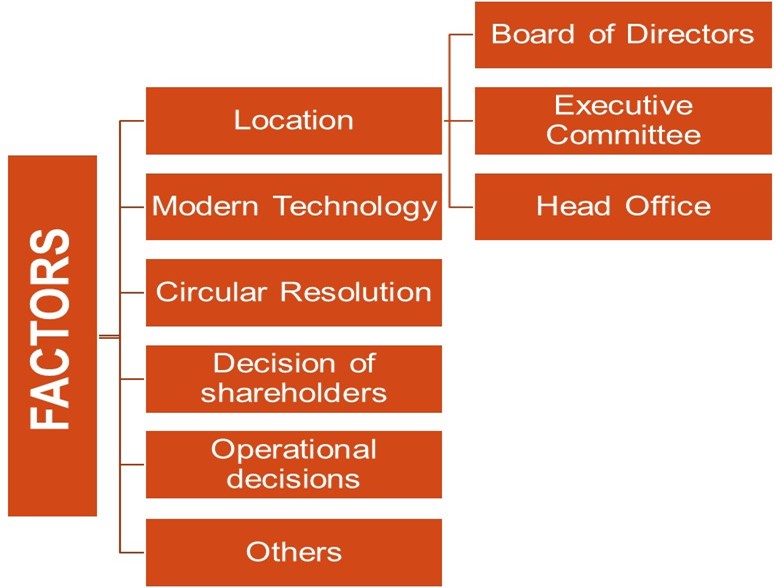

VARIOUS FACTORS TO BE CONSIDERED TO DETERMINE PLACE OF EFFECTIVE MANAGEMENT

The various factors which are to be considered , to determine the POEM of a company are as under : –

LOCATION OF BOARD OF DIRECTORS

Generally speaking, in case of a company, the Board of Directors/ shareholders, are responsible for making the key decisions in the company. Since the criteria of POEM of a company, is dependent on who takes the key managers and commercial decisions, and the place where such decisions are taken, the location where a company’s Board regularly meets and makes decisions is important to determine whether the company has a POEM in India.

This location, may be the company’s POEM, provided the following conditions are satisfied : –

- Boardretains and exercises its authority to govern the company. If the Board has the authority but it does not exercises such authority, this condition would not be fulfilled ; and

- The Board should, in substance,make the key management and commercial decisions necessary for the conduct of the company’s business as a whole.

However, in the following cases it cannot be said, that the Board has exercised its Power to make key management and commercial decisions : –

- There is only formal holding of Board Meetings at a place . Such place, and the fact that the meeting has been held there , would not be conclusive for determination of POEM being located at that place.

- The key decisions by the Directors are in fact being taken in a place other than the place where the formal meetings are held . In such a case, the other place where the key decisions have been made would be relevant for determination of POEM.

- In certain cases, it’s may happen that the Board has de factodelegated the authority to make the key management and commercial decisions to the senior management or any other person (including a shareholder, promoter, strategic or legal or financial advisor etc). The Board in such a case, generally ratify the decisions that have been made by such person. In these cases, the POEM of the company will ordinarily be the place where these senior managers or the other person make those decisions are based.

EXAMPLE : –

- Ralmart Inc. (‘USA’) held Board meeting at its office in India. Board of Directors of Ralmart Inc. makes all key management and commercial decisions at USA.

- Determine POEM of RalMart ?

SOLUTION : –

- Ralmart Inc. takes key management and commercial decisions at USA. Thus, POEM of Ralmart Inc. would be outside India.

MEANING OF SENIOR MANAGEMENT

For this purpose, the “Senior Management” of a company would mean the person/(s) who are generally responsible for developing and formulating key strategies and policies for the company and for ensuring or overseeing the execution and implementation of those strategies on a regular and on-going basis.

These persons may include : –

- Managing Director or Chief Executive Officer;

- Financial Director or Chief Financial Officer;

- Chief Operating Officer; and

- The heads of various divisions or departments (for example, Chief Information or Technology Officer, Director for Sales or Marketing).

LOCATION OF EXECUTIVE COMMITTEE

In case of several companies, particularly the ones which are large, and have operations in multiple countries, company’s Board may delegate some or all of its authority to one or more Executive Committee . The delegation of authority may be either be by means of a formal resolution or Shareholder Agreement (de jure) or based upon the actual conduct of the Board and the executive committee – de facto.

Such executive Committee consist of certain key members of senior management. The decision taken by such Executive Committee are routinely ratified by the board without a detailed analysis of such decisions.

In these situations, the location where the members of the executive committee are based and where that committee develops and formulates the key strategies and policies for mere formal approval by the full Board, will often be considered to be the company’s POEM.

LOCATION OF HEAD OFFICE

The location of a company’s head office will be a very important factor in the determination of the company’s POEM because it often represents the place where key company decisions are made.

MEANING OF HEAD OFFICE

In case of the company, the decisions are generally taken by company’s senior management. Such management may even be located at the main office of the company, or may be located at different places. Additionally, every company under the corporate laws, is required to provide the registered office to the regulatory authorities for the purpose of communication. Generally speaking, the senior management may be based at the head office of the company.

“Head Office” of a company, generally would refer to –

- The place where the company’s senior management and their direct support staff are located ; or

- If they are located at more than one location, the place where they are primarily or predominantly located.

A company may have head office, at one place even though the majority of its employees may work at a different place. Further, just because the Board of Directors of the company typically meet, at a particular place that place by itself would not become the head office of the company.

The following points would need to be considered for determining the location of the head office of the company : –

a) Senior management and their support staff are based at a single location –

If the company’s senior management and their support staff are based in a single location and that location is held out to the public as the company’s principal place of business or headquarters then that location is the place where head office is located.

b) Members of senior management operate from offices located in the various countries from time to time

In such a case, the company’s head office would be the location where these senior managers –

- are primarily or predominantly based; or

- normally return to following travel to other locations; or

- meet when formulating or deciding key strategies and policies for the company as a whole.

c) Participate in various meetings via telephone or video conferencing

In case where the members of the senior management operate from different locations, and participate in various meetings via telephone or video conferencing, the head office would normally be located at the place, where the highest level of management (for example, the Managing Director and Financial Director) and their direct support staff are located.

d) In situations where the senior management is so decentralised that it is not possible to determine the company’s head office with a reasonable degree of certainty, the location of a company’s head office would not be of much relevance in determining that company’s place of effective management.

USE OF MODERN TECHNOLOGY FOR BOARD MEETINGS

With the advent of modern technology, and the fact that the companies have grown across different geographical locations, sometimes, the traditional board meeting wherein, the directors of the company meet at a particular location may not be possible. In such a case, the physical location of Board Meeting may not be relevant, where the key decisions are in substance being made through use of Modern Technology. For example, meetings made via video conferencing. In such cases, the place where the Directors, or the persons taking the decisions, or majority of them usually reside, may also be a relevant factor.

CIRCULAR RESOLUTION OR ROUND ROBIN VOTING

A circular resolution is a resolution signed by the Directors of the company , with wording that signify that they are in favor of the resolution. These meetings would generally have a proposer. The proposed resolution is then generally circulated to the members, who convey their views on the resolution.

In order to determine the place of effective management in cases where the commercial and managerial decisions are passed through circular resolution or round robin voting, the following factors should be considered :-

- The frequency with which circular resolution or round robin voting is used,

- The nature of decisions made in that manner, i.e, whether these decisions are key manager decisions or routine decisions ; and

- Location of the parties, who are involved in those decisions.

Generally, it cannot be said that proposer of decision would be relevant to determine POEM. A detailed evaluation of the facts would be required to determine the person who has the authority and who exercises the authority to take decisions. The place of location of such person would be more important.

DECISIONS MADE BY SHAREHOLDERS

In every company, the shareholders, take various decisions. In order to ascertain the impact of such decisions on place of effective management, one needs to consider whether these decisions are important from the perspective of Business and management of the company, or they are taken by the shareholders to protect their own interest and investment in their capacity as shareholders.

The decisions made by shareholder on matters, which are reserved for shareholder decision under the company laws are not relevant for determination of a company’s POEM. These decisions generally, impact the existence of the company itself or the rights of the shareholders as such, rather than the conduct of the company’s business from a management or commercial perspective.

Some of these decisions may include –

- Sale of all or substantially all of the company’s assets,

- The dissolution, liquidation or deregistration of the company,

- The modification of the rights attaching to various classes of shares or the issue of a new class of shares etc.

However, there may be certain cases where the shareholders may participating into effective management of the company. In such a case, based on the facts of the case, a stand is to be taken whether it would be relevant for POEM.

EXAMPLE : –

If the shareholders limit the authority of Board and senior managers of a company and thereby remove the company’s real authority to make decision, then the undue influence may result in effective management being exercised by the shareholder.

EXAMPLES OF KEY COMMERCIAL DECISIONS :-

- Open a major new manufacturing facility

- Discontinue a major product line.

ROUTINE OPERATIONAL DECISIONS

Day to day routine operational decisions, relating to the oversight of the day-to-day business operations and activities of a company, undertaken by junior and middle management shall not be relevant for the purpose of determination of POEM.

EXAMPLES OF ROUTINE OPERATIONAL DECISIONS :-

- Appointment of plant manager.

- Normal repair and maintenance.

- Implementation of company-wide quality controls and human resources policies.

HOW TO DETERMINE POEM IF SAME PERSON MAKES ROUTINE AND COMMERCIAL DECISION?

In certain situations it may happen that person responsible for operational decisions, is the same person who is responsible for the key management and commercial decision. In such cases it will be necessary to distinguish the two type of decisions and thereafter assess the location where the key management and commercial decisions are taken.

SECONDARY FACTORS

In case the application of the above factors, do not result in clear identification of POEM, then the following secondary factors may be considered:

- Place where main and substantial activity of the company is carried out; or

- Place where the accounting records of the company are kept.

OTHER FACTORS

The determination of POEM has to be considered based on all relevant facts related to the management and control of the company. It cannot be determined on the basis of isolated facts , which by themselves, do not establish effective management.

In the following cases, the facts may not necessarily indicate where the pace of effective management is situated : –

- Foreign company is completely owned by an Indian company – POEM may not necessarily be in India.

- PE of a foreign entity in India – – POEM may not necessarily be in India.

- One or some of the Directors of a foreign company reside in India – – POEM may not necessarily be in India.

- Local management situated in India in respect of activities carried out by a foreign company in India – POEM may not necessarily be in India.

- Support functions that are preparatory and auxiliary in character in India – POEM may not necessarily be in India.

POEM PRINCIPLES ARE ONLY FOR GUIDANCE

- POEM principles are for guidance only and no single principle will be decisive.

- Principles are to be seen with reference to activities performed over a period of time, during the previous year.

- If it is determined that during the previous year the POEM is both in India and outside India, it shall be presumed to be in India, if it has been mainly /predominantly in India.

AO TO SEEK TWO STAGE APPROVAL FOR TREATING POEM OF FOREIGN COMPANY IN INDIA

In order to ensure that the POEM provisions are not misused by the tax office, and are not applied in each and every case, the AO is required to take two-stage approval , before treating any Foreign Company as resident in India on basis of its POEM

STAGE 1: – BEFORE GIVING ANY FINDING

In case the Assessing Officer proposes to hold a foreign company as resident in India, on the basis of its POEM, then any such finding shall be given by the Assessing Officer after seeking prior approval of the collegium of three members (consisting of the Principal Commissioners or the Commissioners, as the case may be)

STAGE 2: BEFORE INITIATING PROCEEDINGS

The Assessing Officer (AO) shall, seek prior approval of Principal Commissioner or Commissioner before initiating any proceedings for holding a foreign company as resident in India on the basis of its POEM.

USAGE OF AVERAGE DATA TO DETERMINE PLACE OF EFFECTIVE MANAGEMENT

For the purpose of determining Active Business Outside India, the average of the data of the previous year and two years prior to that shall be taken into account. In case the company has been in existence for a shorter period, then data of such period shall be considered.

RULES FOR DETERMINATION OF ABOI

PERIOD FOR WHICH DATA TO DETERMINE POEM IS TO BE CONSIDERED

In order to ensure that the POEM provision are applied based on activities of a longer period, the law provides that the data , which should be considered to arrive at POEM should be for a period of more than the previous year.

- In case of a company which has been in existence for the period of more than two years prior to the previous year

The average of the data of the previous year and two years prior to that shall be taken into account . - In case the company has been in existence for a shorter period

The data of the period for which the company has been in existence shall be considered.

ACCOUNTING YEAR PERIOD OF FOREIGN COMPANY IS DIFFERENT FROM PREVIOUS YEAR

In India, the previous year, for tax purposes is considered to start from April 1 and ends on March 31 of the next year. However, different countries may have different time period, for the purpose of computing taxable income. Where the accounting year for tax purposes, in accordance with laws of country of incorporation of the company, is different from the previous year for Indian tax purpose, then, data of the accounting year of the Foreign Company that ends during the relevant previous year and two accounting years preceding it shall be considered.

EXAMPLE : –

Cheetah Mauritius, follows accounting year for tax purposes as 1 July – 30 June, of every year. Which year’s data should be used in order to apply ‘Active Business Outside India’ test for FY 2016-17 ?

SOLUTION : –

In this case, accounting year of Mauritius (i.e., July 1, 2016 to June 30, 2017) is different from the previous year of Indian Income Tax Act , 1961 (i.e., April 1, 2016 to March 31, 2017).

Data of following accounting years (as per Mauritius Tax laws) shall be considered to apply ‘Active Business Outside India’ test : –

i) 2015-16 – July 1, 2015 to June 30, 2016 (Since this previous year ends during , previous year of Indian Income Tax Act , 1961 (i.e., April 1, 2016 to March 31, 2017).

ii) 2014-15 – July 1, 2014 to June 30, 2015 ;and

iii) 2013-14 – July 1, 2013 to June 30, 2014.